This article was submitted by Michael Stark, market analyst at Exness.

Most stock markets have started the week positively after Asian shares generally moved up yesterday and Chinese annual exports surged more than 30% last month. The main focus of data for traders this week is on inflation from the USA and the UK, so this preview of weekly data looks at USDCNH and GBPJPY.

There were no significant events in monetary policy last week, with the last notable change still the BdeM’s hike on 24 June. The central banks of New Zealand, Canada and Turkey are all due to meet tomorrow, followed by Japan on Friday morning. Any change to policy is unlikely.

The key release for many markets this week is this afternoon’s annual inflation from the USA. Non-core is expected to decrease slightly from 5% to 4.9%, but the consensus is for the core figure to rise negligibly to around 4%. An upside surprise from these figures might have a significant effect on gold and possibly cryptocurrencies given the FOMC’s confidence that high inflation is temporary.

Earnings season is also underway this week, with major American banks including JPMorgan Chase, Bank of America and various others due to report figures for the second quarter. Altogether this is quite an active week of news and figures in markets, so volatility might be higher than usual for this time of year.

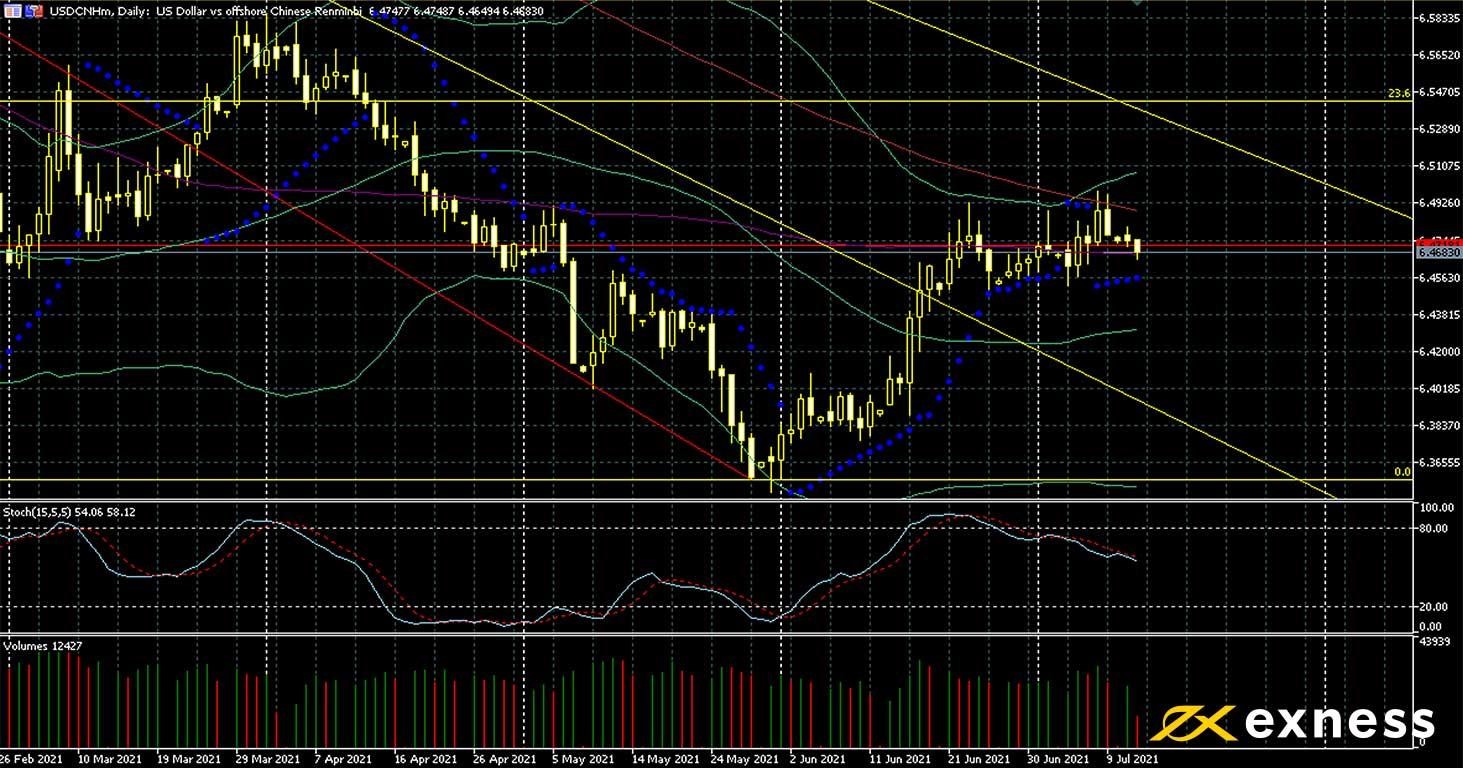

Dollar-offshore yuan, daily

USDCNH’s fundamentals are somewhat less weak than at the beginning of the year but the pressure from sentiment remains to the downside. Very strong growth in Chinese exports as announced this morning have combined with the rate differential and the Fed’s reluctance to set a timeline for tightening to reduce enthusiasm for buying so far this week. With the offshore yuan at a low of about three months against the dollar, this looks from a fundamental perspective like a good entry for new sellers.

While a retest of the multi-year low around ¥6.36 doesn’t seem likely in the immediate future, a movement above the 200 SMA is also unfavourable. With no sign of saturation and the significant low quite close, consolidation with the value area between the 50 and 100 SMAs seems to be possible in the absence of a new, strong driver from the news or economic data. This afternoon’s inflation release from the USA is a key figure but traders will also monitor the large number of statistics from China on Thursday morning GMT.

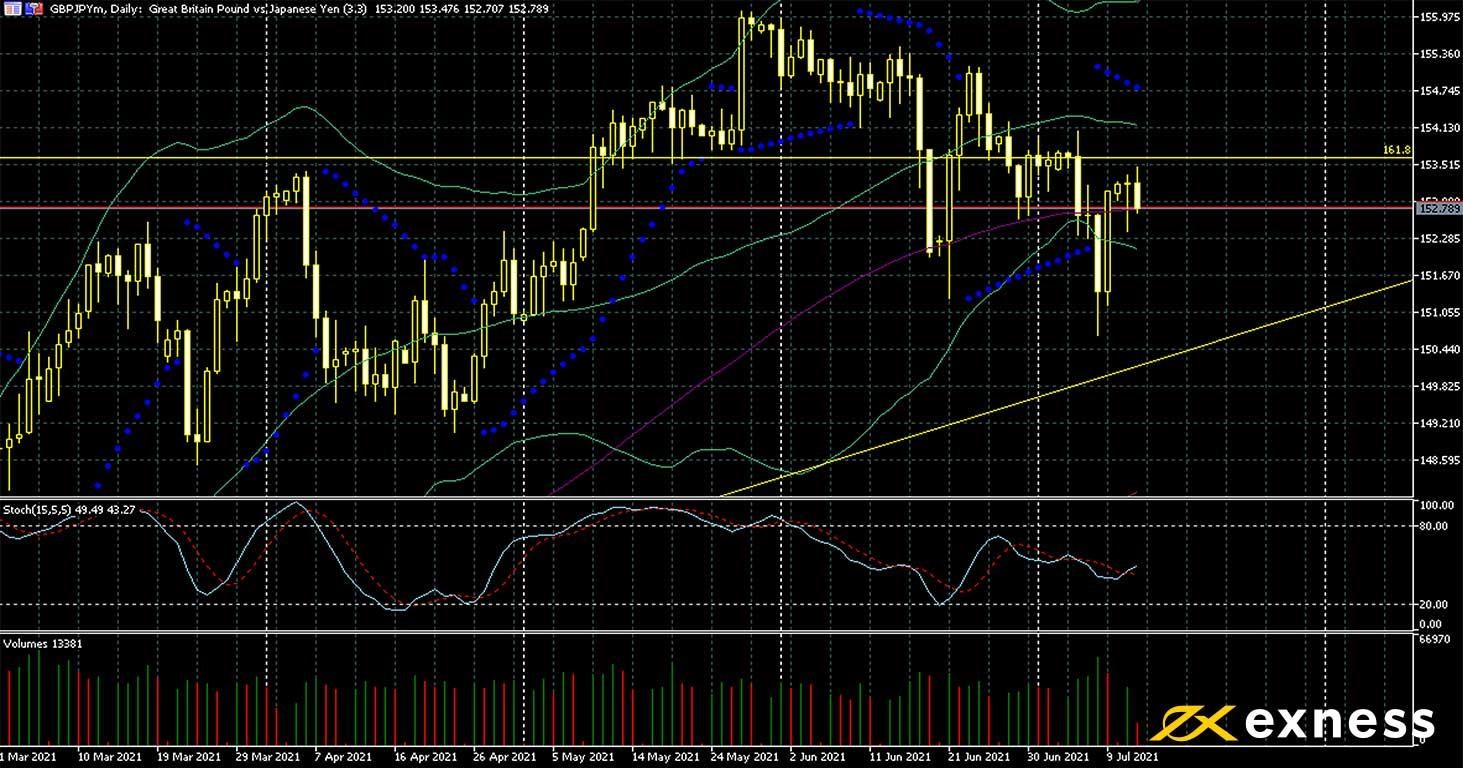

The pound has retreated from its highs against the yen amid moderately high volatility over the last few weeks as the Japanese currency has generally strengthened somewhat against ESMA/ASIC-defined majors. This week, though, sentiment might turn more negative on the yen given that Tokyo has now entered its fourth state of emergency since the advent of covid-19. Equally, though, buyers of the pound might be somewhat concerned by the British government’s determination to push ahead with ‘freedom day’ on 19 July against all medical advice.

¥150 is an obvious psychological area from which one would typically expect a bounce, while the 50 SMA from Bands around ¥154.10 could cap upward movement over the next few days. The signal from moving averages is still buy; notably this symbol hasn’t managed to complete a daily close clearly below the 100 SMA despite sharp intraday movements on 18 June and 8 July. Claimant count change is the crucial figure for GBPJPY this week, but markets’ reaction to inflation data tomorrow should also be monitored.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.