This article was submitted by Michael Stark, market analyst at Exness.

Negativity in some markets so far today as European countries, notably Germany, have tightened their lockdowns has been tempered by ongoing rollout of vaccines against covid-19. The American FDA’s authorisation of Pfizer’s vaccines has also been a positive. This preview of weekly forex data looks at XAUUSD, USDMXN and EURNOK.

Central banks were mostly inactive last week with the ECB basically continuing with ‘wait and see’ despite the unusually high rate of euro-dollar. This week’s main event in monetary policy is the meeting of the Federal Open Market Committee on Wednesday night GMT. As before no change in rates is likely but comments on the dollar’s weakness and the possibility of continuing unlimited QE will be in view for traders. Other central banks meeting this week include the Bank of Thailand, Banco de México, Magyar Nemzeti Bank, the Swiss National Bank and Norges Bank.

The key regular data this week are tomorrow’s employment releases from the UK, foremost among them claimant count change. Coming in the context of the extension of Brexit talks until New Year’s Eve, the outlook for the pound from data remains important. Traders are also looking ahead to balance of trade from various countries, notably Japan and Canada, plus inflation from Japan and the UK.

For pairs with the pound, the pressure seems to be off somewhat this week since few now expect a significant breakthrough in trade talks with the EU before Christmas. Nevertheless, cable, EURGBP and GBPJPY are likely to be extremely volatile tomorrow morning from 7.00 GMT at the crucial releases.

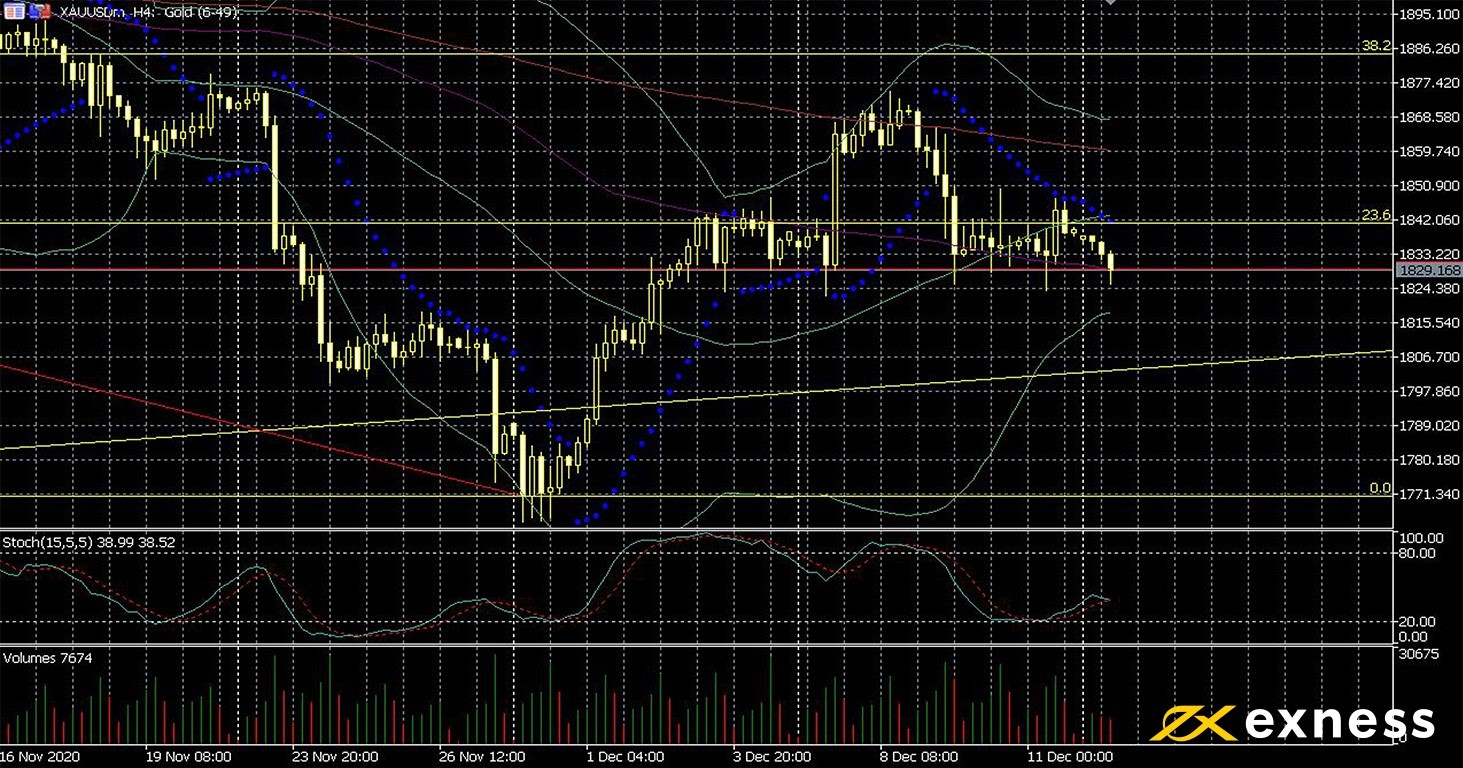

Gold-dollar, four-hour

Gold has continued to test weekly lows so far today as the environment of positive sentiment in stock markets generates headwinds. Rollout of vaccines against covid continues to spur oil and many indices upward, with participants in gold markets discounting for now record low rates and extensive QE. So far, December has certainly been quieter for the yellow metal than many traders had expected.

Despite the ongoing formation of a classic head and shoulders pattern which might complete over the next few periods, bulls focussing on the chart will have cheered last week’s golden cross over the 50 and 100 SMAs. A combination of both fundamentals, i.e. mainly sentiment, and TA is likely to be important over the next few days as price tests the value area between these two moving averages to the downside.

This week’s meeting of the Fed is obviously the critical event for gold and might see loose monetary policy coming back into main view, boosting the metal. The other important event is American retail sales on Wednesday afternoon GMT.

Key data this week

Bold indicates the most important releases for this symbol.

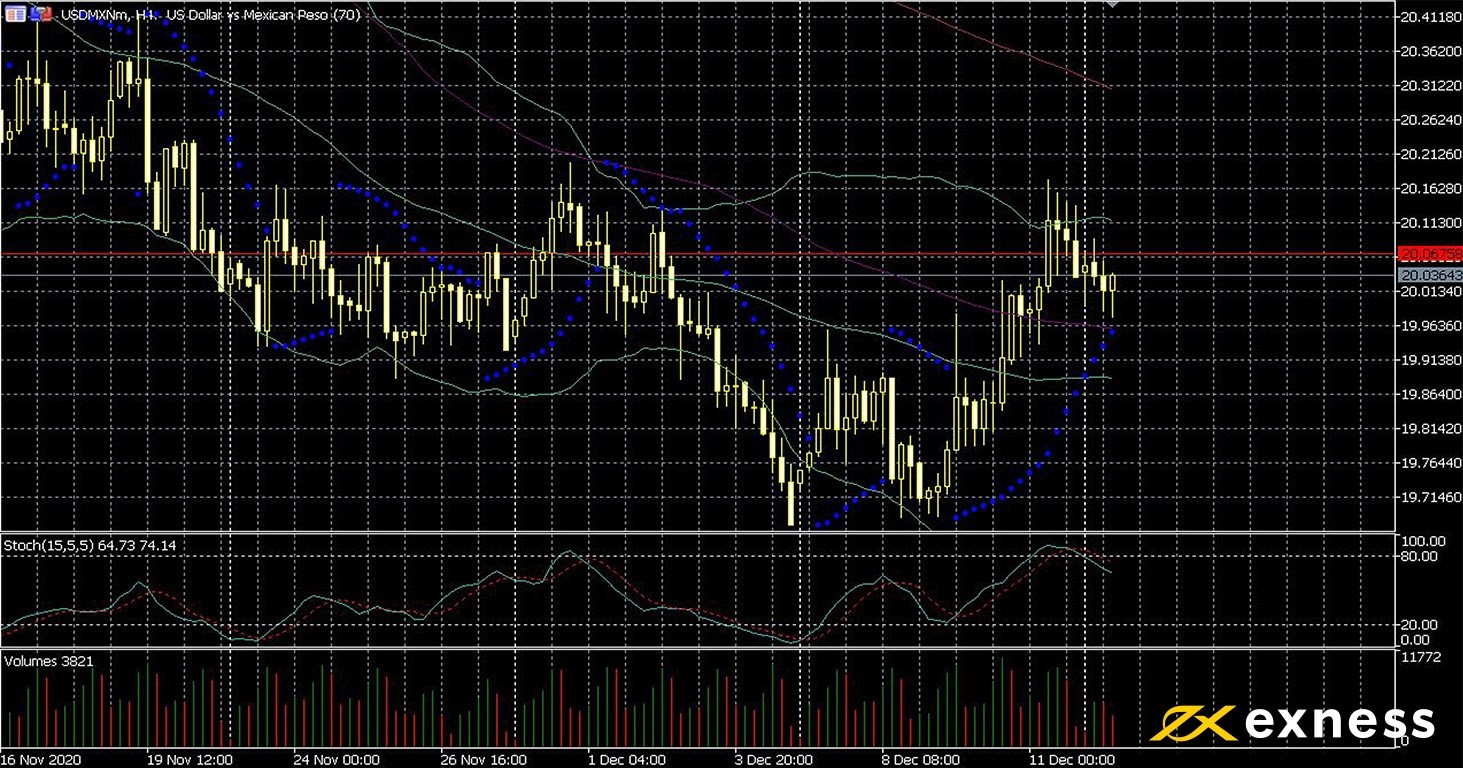

From a fundamental point of view, things look fairly good for the peso. Industrial data on Friday beat expectations; with inflation at 3.3% and close to Banxico’s target of 3%, the government is continuing to consider a 15% hike in the minimum wage. Oil’s strong gains over the last few weeks have also supported MXN due to Mexico’s importance as an exporter of crude.

The recent bounce by the dollar then appears to be more of a technical development and a liquidity-driven movement on the daily chart. Failure to break through the latest lower high on Friday night GMT around Mex$20.17 combined with a downward crossover of the slow stochastic in overbought signal a resumption of the trend sooner or later.

Uncertainty over fiscal policy in the USA and its knock-on effects in Mexico is an important factor here, but this question is very unlikely to be resolved until the incoming Democrat administration starts to legislate in January. This week’s meeting of the FOMC is key here as for gold, but Banxico’s decision on rates is the most important. Due on Thursday night GMT, the consensus is for a cut of 0.25% in the benchmark rate, which would take it to 4%.

Key data this week

Bold indicates the most important releases for this symbol.

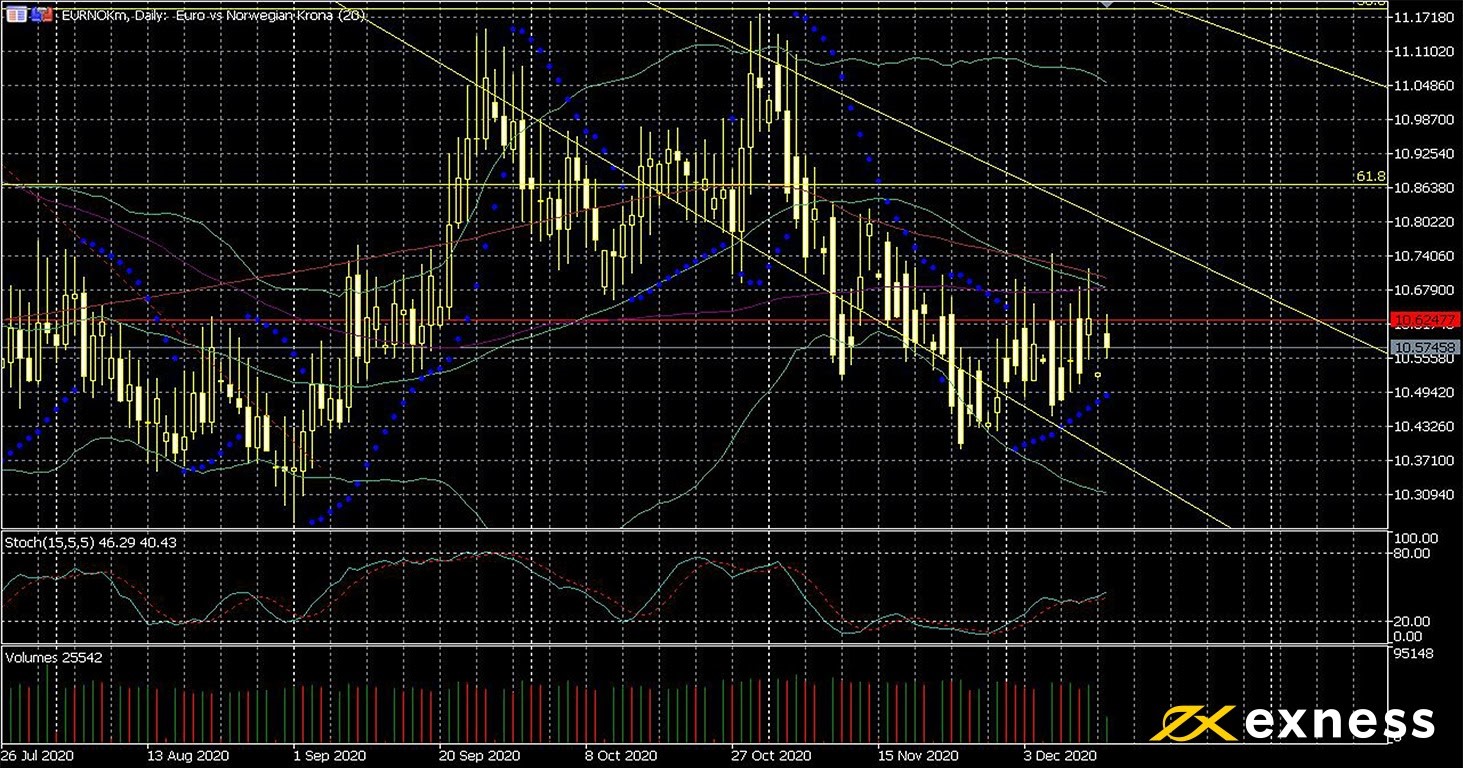

Economic recovery in Norway has been relatively stronger than that in the EU over the last few weeks. Data since early November have shown inflation in Norway at an eight-month low, modest falls in producers’ prices, unexpectedly better retail sales and for Q3 a higher current account surplus. Norway’s relatively sparse population has made it among the less affected economies in Europe from covid.

While the most recent test of the lower area of the Fibonacci fan last week was unsuccessful, the impression from TA for EURNOK remains fairly negative. Moving averages have nearly finished reconfiguring back into a sell signal and there is currently no oversold signal. The 61.8% weekly Fibonacci retracement area could cap another bounce; such a lower low might confirm the downside into the end of the year.

This week’s standout event for the Norgie krone is the meeting of the Norges Bank on Thursday morning GMT. No change in rates or other aspects of policy is expected but comments on the outlook for trade and general economic recovery over the next quarter are likely to be key. Other important releases affecting the krone this week are balance of trade tomorrow and unemployment on Friday. Finally as usual there’s a range of data from the eurozone that could drive short-term volatility.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.