This article was submitted by Michael Stark, market analyst at Exness.

Oil was an early strong mover this week, up around 8% on Monday after OPEC+’s surprise decision to cut more than a million barrels of production daily from May to the end of the year. Most other major CFD instruments started off slowly as traders look ahead to the job report from the USA on Friday. This preview of weekly data looks at USDCAD and USOIL.

Regional central banks were active last week, with the Banco de Mexico, South African Reserve Bank and Bank of Thailand all hiking their rates. This week the focus is on Australia and New Zealand, but the NFP might have an impact on expectations for the Fed’s next meeting if it’s significantly different from the consensus. At the time of writing, CME FedWatch Tool suggests a 60% chance of a single hike to the funds rate on 3 May with a 40% chance of a hold.

Apart from Friday’s employment data from the USA, this week’s key releases include Canadian, American and Australian balance of trade and the Canadian job report. With no major earnings expected this week and little important data apart from jobs and trade, the focus is also likely to be on regular stocks of crude oil given the unexpected nature of OPEC+’s latest decision.

US dollar-Canadian dollar, daily

Given the loonie’s traditional correlation with crude oil, the price of USDCAD declined sharply on Monday. Banks’ issues in the USA haven’t spilled over to Canada significantly so far while the outlook for monetary policy seems more-or-less balanced; both the Fed and the Bank of Canada are expected to start cutting rates sometime in the second half of the year.

Now that the price has broken below the 200-day moving average for the first time in three months, the door might open for further losses. Conversely, the slow stochastic prints an extreme oversold reading around 4, so selling in here for the medium term would not usually be favourable. Instead, waiting for a small or moderate bounce to the area of the 200 SMA before finding an entry to sell could derisk a trade somewhat.

Dollar-loonie is likely to be highly active later this week because of the respective countries’ job reports on Thursday and Friday. Since the NFP has consistently been higher than expected in 2023 so far, it wouldn’t be very surprising to see a stronger result on Friday with a kneejerk higher for USDCAD. That could provide an opportunity for sellers to enter at a more favourable price, but depending on sentiment on the US dollar and oil’s movements it’d be possible to see the price continue to bounce. Gauging the strength of the reaction to Friday’s data for at least a few minutes might be wise before committing.

12:30 GMT: American annual average hourly earnings (March) – consensus 4.3%, previous 4.6%

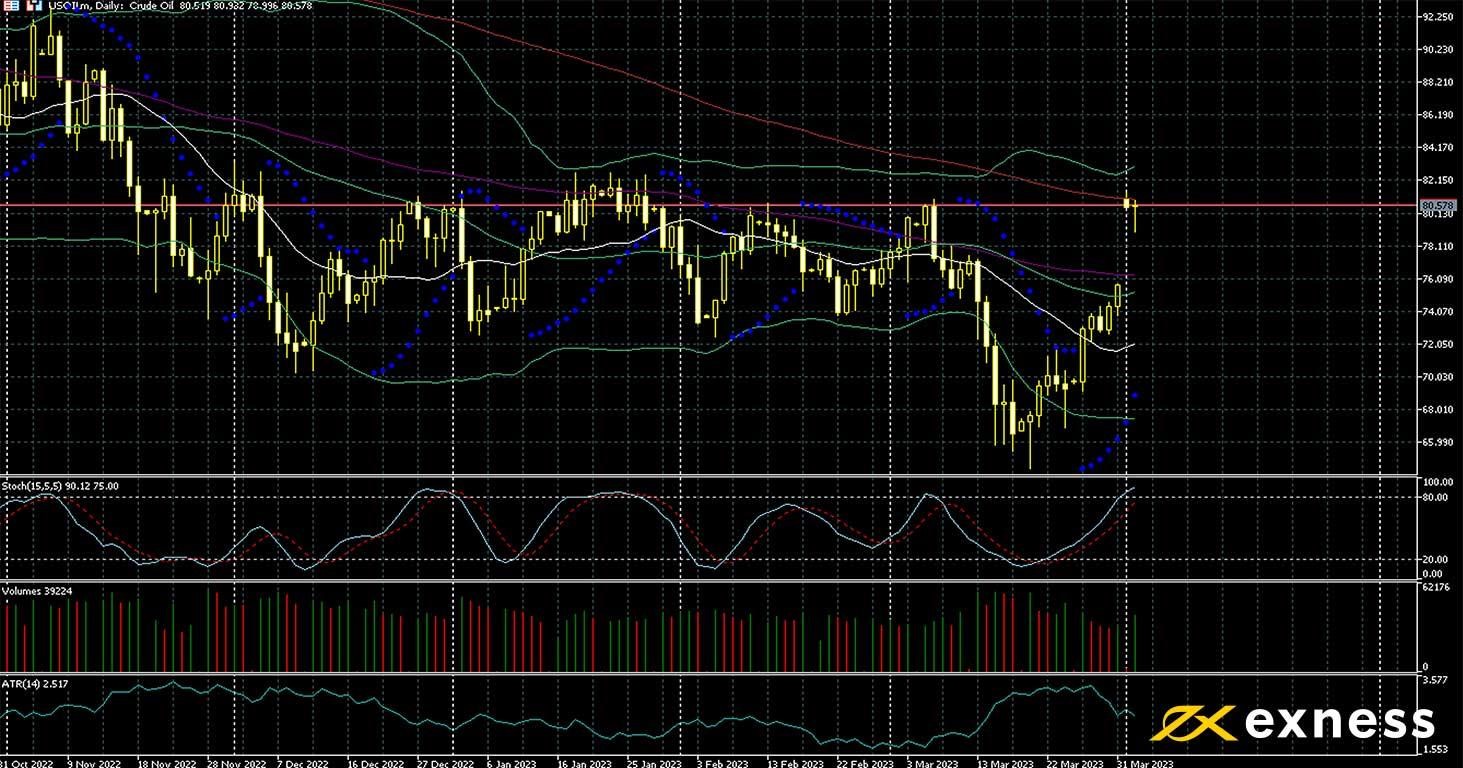

American light oil, daily

USOIL gapped up more than $5 over the weekend after OPEC+ announced a surprise cut to production of more than a million barrels daily from May to the end of 2023. In practice, it’s likely that the total cuts will be significantly higher than this, with Russia in particular eager to cut more. While markets seemed to have been pricing in some sort of further action from the group and its allies, few had expected a sudden move like this. Meanwhile the outlook for demand from China still seems to be positive. On the other hand, the dispute over exports of oil from Iraqi Kurdistan through Turkish ports seems more likely to be resolved within weeks rather than many months.

It’s challenging to apply TA after a gap this large. There seems to be some reluctance to push above the 200 SMA, but this is partially because a gap of more than 5% for crude oil would usually close within a few days before a possible resumption of the movement. That might seem especially relevant now that the price is overbought based on the stochastic and there hasn’t been clear support from buying volume.

This week’s stocks from the USA might give traders more useful information and possibly drive further movement. Equally, traders of oil should monitor the job report from the USA because most markets price oil in dollars: commentary about the rise of the ‘petroyuan’ seems to be overblown for now.

Key data this week

Bold indicates the most important release for this symbol.

Tuesday 4 April

20:30 GMT: API crude oil stock change (31 March) – previous negative 6.08 million

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.