This article was submitted by Michael Stark, market analyst at Exness.

What would usually be among the most inactive weeks of the year has started with a bang as participants in many markets have been spooked by news of a more virulent strain of covid emerging in south-east England. Most European indices are down today as is oil. This last preview of weekly forex data in 2020 looks at cable (GBPUSD), UKOIL and EURJPY.

Central banks were mostly inactive last week, with each meeting announcing no change to rates. The People’s Bank of China also kept its loan prime rate on hold early this morning GMT. The main event this week in monetary policy is the meeting of the Central Bank of the Republic of Turkey on Thursday at 11.00 GMT. The CBRT is expected to hike its one-week repo rate from 15% to 16.5%.

There isn’t a huge amount of regular data scheduled for this week, but traders are likely to focus on some key releases from the USA. The most important of these are personal income and spending on Wednesday and durable goods on Thursday. German GfK consumer confidence tomorrow morning is also in view.

Despite higher nervousness in most markets so far this week, traders can reasonably expect volume to remain low in the runup to Christmas on Friday. This means that volatility is likely to be high as ‘choppy’ markets take in new information, so caution is advised particularly for traders of the pound sterling and crude oil.

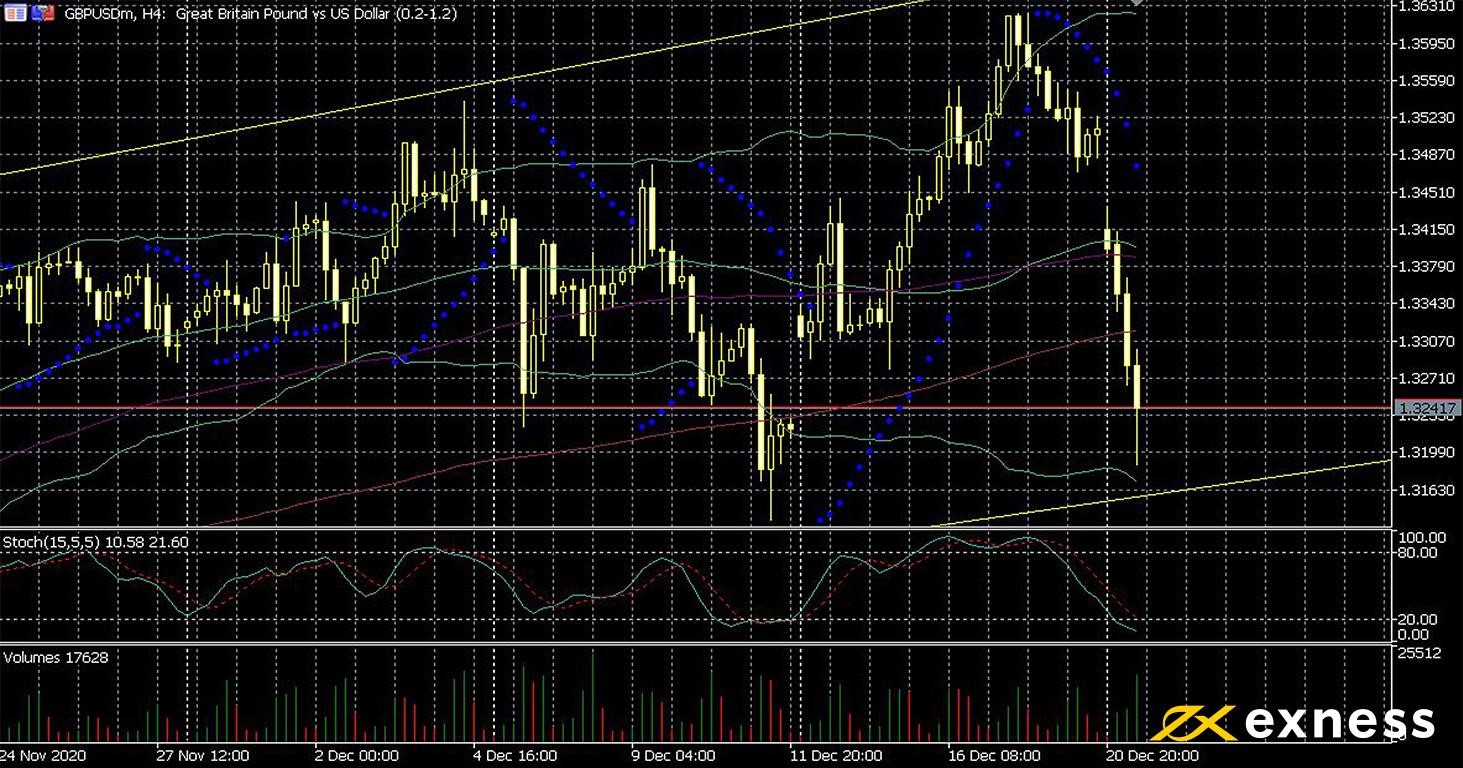

Cable, four-hour

Cable tanked against the dollar and various other major currencies this morning after most of south-east England went into tier 4 lockdown and as France, Germany and other large European countries banned flights from the UK. The UK’s Brexit-related contingencies are currently being tested after France forbade entry to accompanied traffic, with motorways in Kent being used as waiting areas for heavy vehicles. Meanwhile another supposedly hard deadline for trade talks between the UK and EU passed last night with no sign of progress.

The pound’s fall today has been quite dramatic on the chart, with none of the 50, 100 or 200 SMAs providing any clear support. However, buying volume has been unusually high for the time of year so far today, so there is clearly some demand to push sterling back up toward the value area at least.

We can expect cable to be particularly unstable over the festive period as the end of the transition period approaches on new year’s eve. Data is likely to have some impact in the short-term, but ongoing direction depends completely on the outcome (or breakdown) of the trade talks between the UK and the EU.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 22 December

00 GMT: British current account (Q3) – consensus -£11.6 billion, previous -£2.8 billion

00 GMT: British annual GDP growth (final, Q3) – consensus -9.6%, previous -21.5%

00 GMT: British quarterly GDP growth (final, Q3) – consensus 15.5%, previous -19.8%

Wednesday 23 December

30 GMT: American personal income (November) – consensus -0.3%, previous -0.7%

30 GMT: American personal spending (November) – consensus -0.2%, previous 0.5%

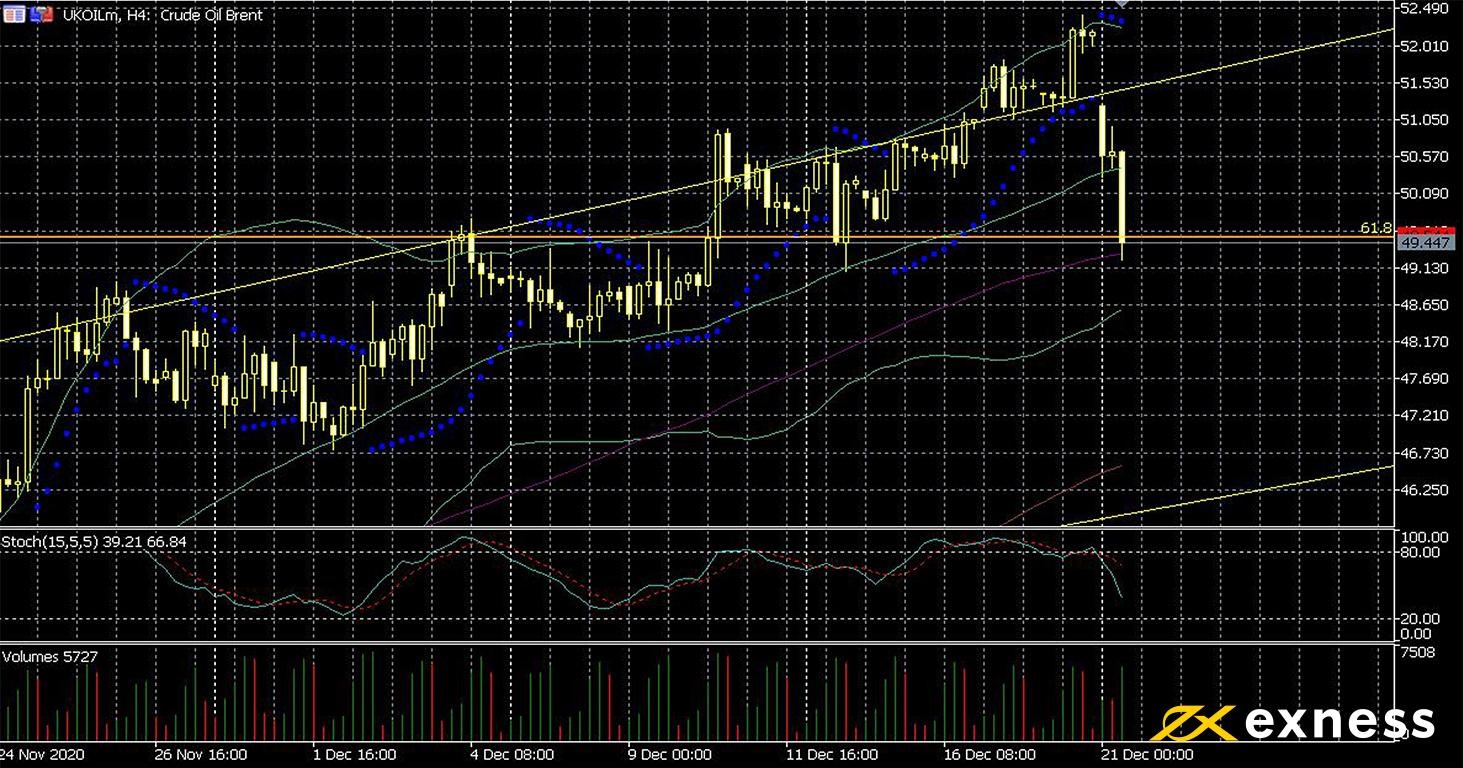

Similarly to the pound, crude oil moved sharply downward this morning GMT as the outlook for demand, particularly aviation fuel, worsened significantly. Participants are pricing in the potential effects of the new strain of covid, known so far as ‘N501Y’. Traders of oil have ignored the likely passing of new fiscal stimulus in the USA worth nearly a billion dollars; so far this week they have also discounted increasing rollout of vaccines around the world.

The key support in the short term for oil is the 100 SMA which price is currently testing. In the absence of more bad news, a small bounce might be expected from this zone. Another key support exists around the 200 SMA. With volume likely to drop off in the second half of the week, ranging around $50 is favourable since this crucial psychological area has yet to be broken convincingly.

Key data this week

Bold indicates the most important release for this symbol.

Tuesday 22 December

30 GMT: API crude oil stock change (18 December) – previous 1.97 million

The euro has been somewhat volatile against the yen so far today. While many similar Brexit-related drivers are affecting the common currency, there has yet to be any notable indication of ‘flight to safety’ boosting the yen. While the VIX has reached a month’s high this morning at 29.52, it still hasn’t passed the ‘trigger point’ of 30, indicating that fear in markets has yet to become very great this week.

Turning to the technical view, it’s clear from the chart of euro-yen that the value area between the 50 and 100 SMAs is still an important support. The beginning of expansion by Bollinger Bands (50, 0, 2) suggests some volatility to come as 2021 approaches. Last week’s oversold signal has also disappeared, with the slow stochastic (15, 5, 5) at 21 now very close to oversold instead.

This week’s data for EURJPY are likely to drive some volatility and instability, but no clear directional movement is likely unless significant new information on N501Y or other important factors reaches markets. Japan is one of few countries to release important data on Christmas day: annual retail sales and November’s rate of unemployment are expected late on Thursday night GMT. Holding yen positions over Christmas should probably be avoided.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.