This article was submitted by Michael Stark, market analyst at Exness.

At the start of a highly active week of economic data, markets were somewhat surprised by weaker than expected Chinese PMI. Caixin manufacturing PMI at 51.5 early this morning was a seven-month low, but so far shares and commodities have been fairly static except for silver. With the NFP approaching on Friday, this preview of weekly forex data takes a closer look at USDCAD, GBPAUD and XAGUSD and data affecting these symbols.

Central banks were fairly inactive last week, with the Fed releasing a statement more-or-less identical to the previous one. This week could be more eventful, with two major central banks meeting, the Reserve Bank of Australia tomorrow morning GMT and the Bank of England at noon GMT on Thursday. Elsewhere decisions are expected from the Bank of Thailand, the National Bank of Poland and the Czech National Bank. No significant changes to policy are expected but economic projections are in focus.

The most important regular data this week is Friday’s non-farm payrolls. American balance of trade and various Canadian releases are scheduled for the same time, so USDCAD is likely to be very active on Friday afternoon. Australian balance of trade shortly after midnight GMT on Thursday rounds off the week’s most important figures.

Earnings season is also in focus this week. Tomorrow is a particularly big day, with Alphabet, Amazon, Pfizer and ExxonMobil all releasing their earnings reports.

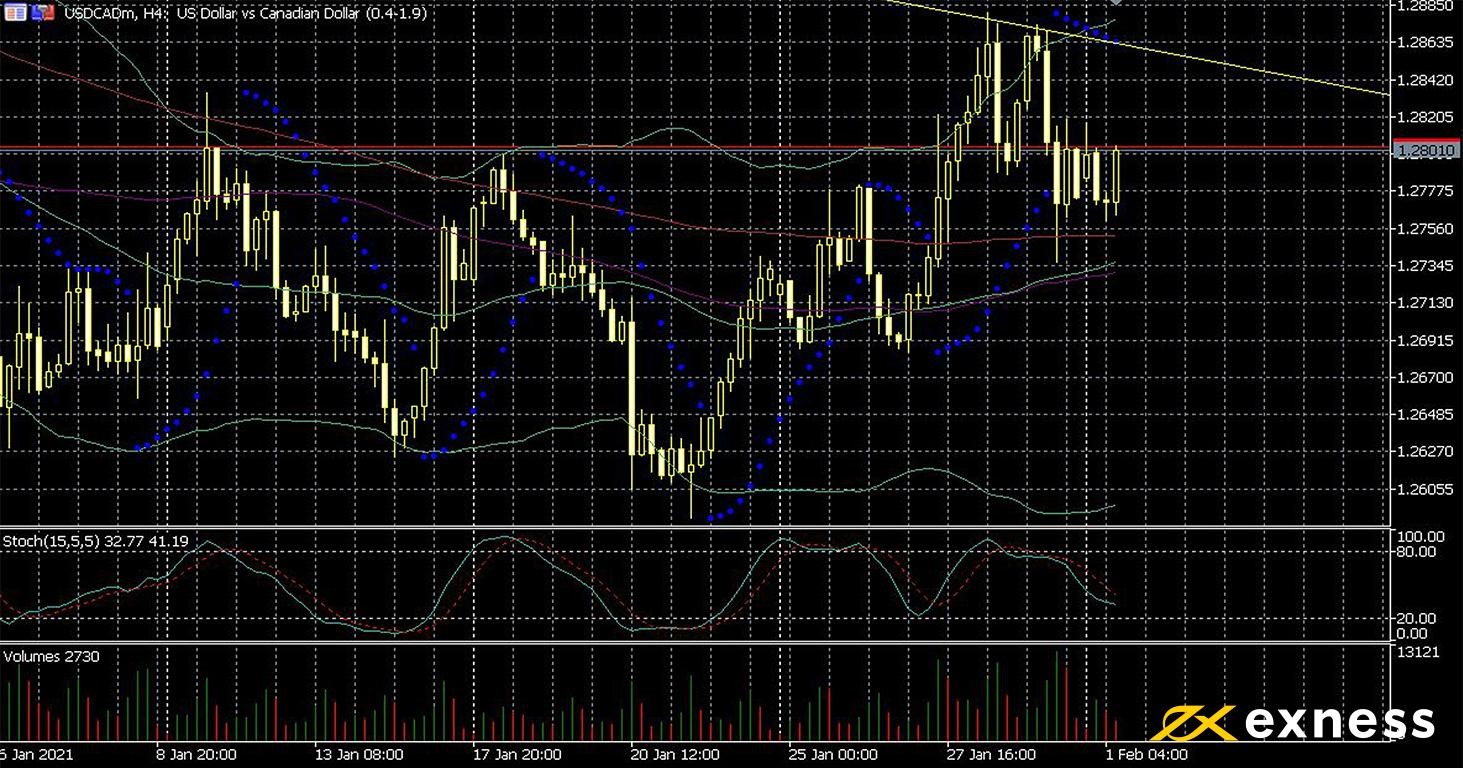

US dollar-Canadian dollar, four-hour

The greenback has made some gains against its northern counterpart as against other majors since last week amid rising yields from American bonds and ongoing high demand for US dollars to buy shares. On the other hand, oil has also remained strong since last week, giving some fundamental support to the loonie.

There seems to be more room for gains here by the US dollar from a technical point of view. Moving averages are below the price, with none except the 200 SMA having offered significant resistance in the second half of January, and the 50 SMA from Bands is about to complete its golden cross of the 100. There is no sign of overbought from either Bollinger Bands (50, 0, 2) or the slow stochastic (15, 5, 5).

There’s no critical data due for USDCAD until Friday at 13.30 GMT. This is when the storm of releases begins, with the NFP plus balance of trade from both the USA and Canada all coming out at the same time. On the face of analysts’ predictions combined with TA, we might expect the greenback to continue upward to retest the latest high, but entering a large trade here before the data is still a big risk.

Key data this week

Bold indicates the most important releases for this symbol; bold red indicates a release of critical importance for most markets.

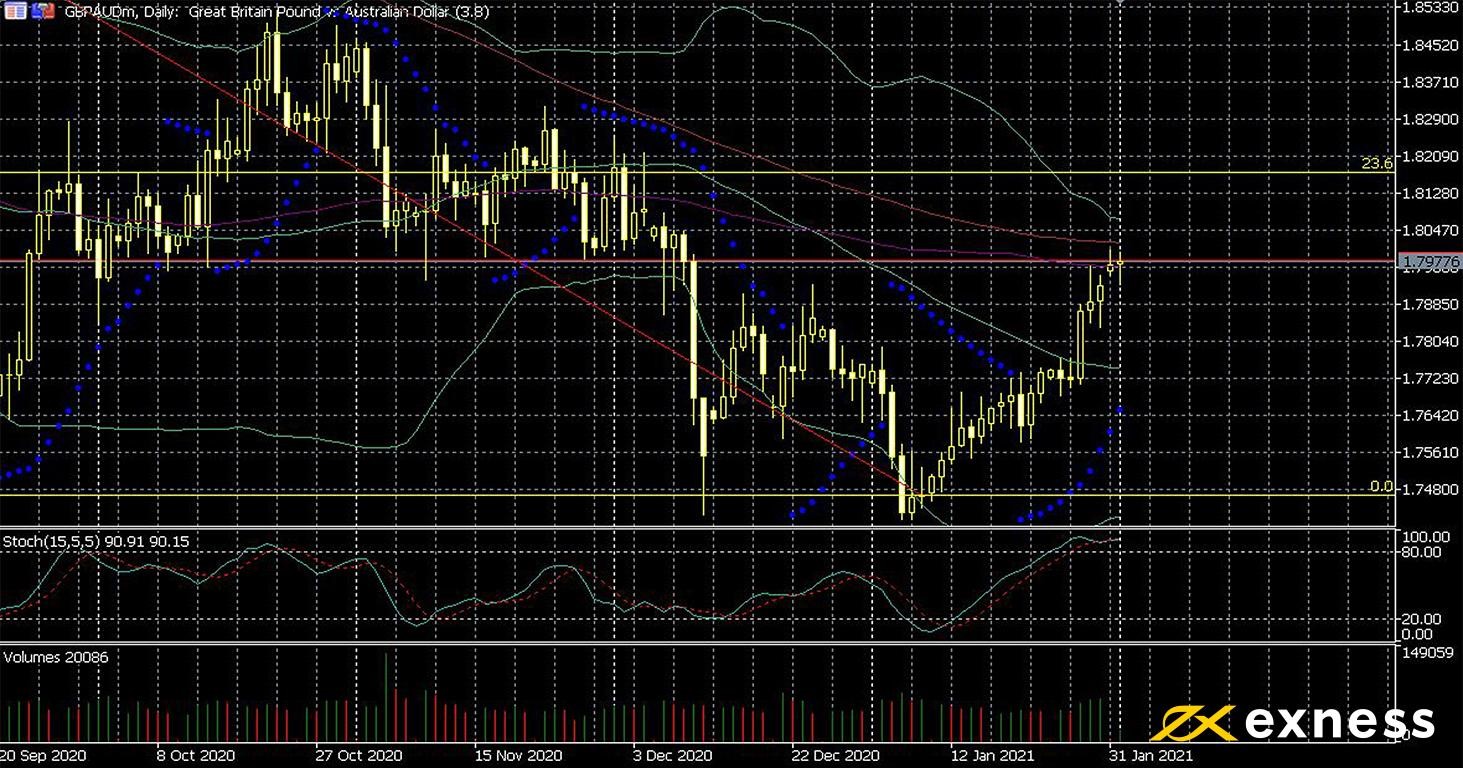

The pound sterling remains close to at least annual highs against both the euro and dollar but has only recently bounced against the Aussie dollar. Last week appears to have been partially a technical movement given that fundamentals on AUD are significantly better than for the pound, with rising prices of industrial commodities and relative calm in Aussie-Chinese relations. Markit manufacturing PMI from Australia this morning at 57.2 also beat estimates. However, very high recent rates of vaccination in the UK have led to some positive sentiment on the pound.

The 0% Fibonacci retracement area here is the same as the 100% weekly retracement based on the pound’s gains to the end of March last year, a strong support from which there’s been an energetic bounce since last week. The main areas of resistance in view this week are the 100 and 200 SMAs plus the 23.6% weekly Fibonacci retracement area. As of now, though, the slow stochastic (15, 5, 5) gives a clear overbought signal at about 91.

The main focus for this symbol over the next few days is monetary policy, with both the RBA and BoE meeting this week. Neither is at all likely to make any substantive change to QE and definitely not rates, but how the committees project economic recovery this quarter could be important.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 2 February

from 3.30 GMT: meeting of the Reserve Bank of Australia

Thursday 4 February

30 GMT: Australian balance of trade (December) – consensus – A$4.4 billion, previous – A$5.02 billion

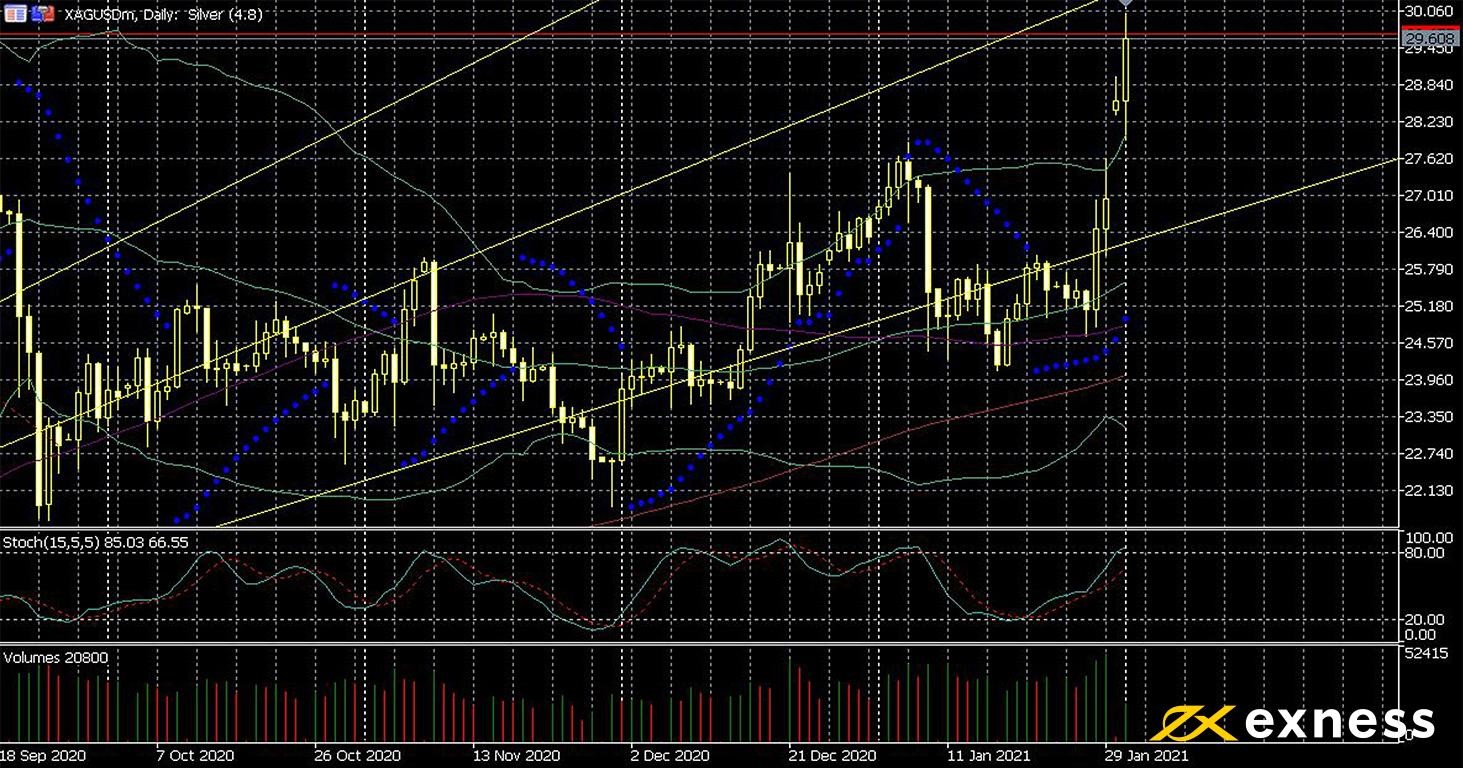

Silver has been the next target of ‘Gamestoppers’ so far this week, with very high enthusiasm from retail traders and investors pushing the price beyond $29 for the first time since August. Silver’s appeal as a haven remains fairly strong as many countries are making slow progress with vaccinations and more infectious strains of covid-19 continue to spread, but rising production inflation is one of the most important general factors driving silver up since the end of last year.

Overbought is the name of the game here, with both the slow stochastic at 85 and Bollinger Bands giving strong signals of buying saturation. Moving averages give a strong buy signal and the 50 SMA golden crossed the 100 at the beginning of last week. The traditional plan of attack in this situation would be to buy in when price retraces to cover the gap up, but waiting to see how this symbol reacts to important data this week would be less risky in the context of small traders’ frenzy.

Key data this week

Bold indicates the most important releases for this symbol;

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.