This article was submitted by Michael Stark, market analyst at Exness.

Sentiment in markets has recovered so far this week as the phaseout of the lockdown in Shanghai approaches. The primary focus of markets this week is on Friday’s job data from the USA, particularly non-farm payrolls and the rate of unemployment. Today’s preview of weekly data looks at USDCAD and UKOIL.

The Reserve Bank of New Zealand announced a two-step hike of its cash rate last week to 2% as was widely expected. However, it also noted that the continuing rise of inflation might mean that rates will have to go up faster than expected this year. The Kiwi dollar made some gains in the aftermath, but participants are somewhat concerned about the possibility of a hard landing if the RBNZ doesn’t strike the right balance. Meanwhile the Central Bank of the Russian Federation cut its key rate by a full 3% to 11%.

The main central bank meeting this week is the Bank of Canada on Wednesday afternoon GMT. Analysts expect another half percent hike to 1.5%, especially given that inflation in Canada accelerated faster than expected last month and reached a fresh 30-year high. Traders will monitor the subsequent comments closely for possible clues on further hikes in the second half of the year.

Apart from American jobs, this week’s important regular releases include Canadian GDP, inflation and unemployment rate in various major countries of the eurozone, Australian GDP and balance of trade plus German balance of trade. This is quite an active week of data even beyond the NFP, so one might expect movements to be larger than normal for many of the symbols affected.

US dollar-Canadian dollar, daily

The greenback has continued to decline against its northern counterpart this week as oil’s gains also continued and as the former seems to have overextended in the last few weeks. Canadian unemployment in April was 5.2%, the lowest figure ever recorded since comparable data began in 1976. The Bank of Canada seems to be very hawkish, prepared like most other major central banks to hike rates significantly against inflation. The Fed is also hawkish, but its policy over the next few months at least seems to be priced in.

With price now within the value area between the 100 and 200 SMAs and strongly oversold based on the slow stochastic, a pause seems likely in the runup to tomorrow’s meeting of the BoC. The target for sellers in the medium term seems to be last month’s lows around C$1.25, while to the upside the 100% weekly Fibonacci retracement area could be an important resistance if the 50 SMA is broken.

This is a particularly active week of data for dollar-loonie, so volatility is likely to pick up strongly from this afternoon’s GDP and following. In this situation, it would traditionally make sense to keep trades small at least until the direction following the BoC’s meeting becomes clear.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 31 May

12:30 GMT: Canadian quarterly GDP growth (Q1) – consensus 1.4%, previous 1.6%

12:30 GMT: Canadian annualised GDP growth (Q1) – consensus 5.4%, previous 6.7%

Wednesday 1 June

from 14:00 GMT: statement and press conference of the Bank of Canada

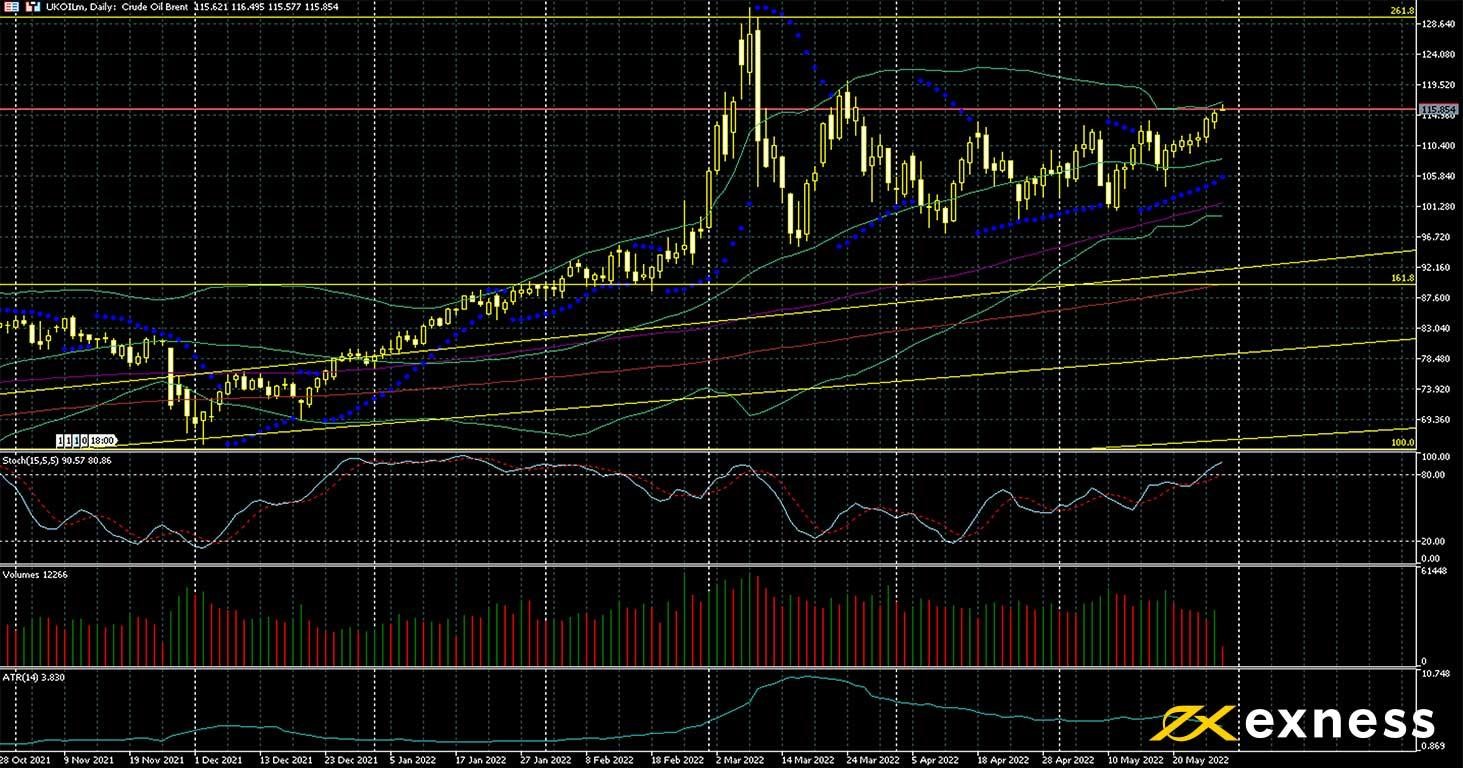

Crude oil has had a strong boost so far this week from the combination of apparently imminent European sanctions on Russian oil and Shanghai’s plans to phase out its lockdown which has been in place since late March. On 16 May, the local government of Shanghai announced that from the beginning of June it would start removing restrictions.

This is positive for demand for oil because Chinese industrial output had shrunk clearly during the period of the lockdown. However, uncertainty remains high: the zero-Covid policy of the government means that more similar lockdowns might return later in the year. At the time of writing, the EU is expected imminently to announce a partial ban on imports of Russian oil, affecting crude brought by sea but not pipelines.

Brent broke above the upper limit of the recent range yesterday to trade around $117, the highest in two months. So far, this movement isn’t clearly supported by volume, while ATR is also dropping and the slow stochastic at about 91 gives an overbought signal. Typically, oil is a good candidate for momentum trades, so it’s possible that there might be more highs this week, but more cautious traders would typically favour a lower entry.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.