This article was submitted by Michael Stark, market analyst at Exness.

Stock markets have generally started the week negatively as participants brace for the critical meetings of central banks this week, with most expected to hold course on their aggressive cycles of tightening. This preview of weekly data looks at EURUSD and GBPJPY ahead of major news on monetary policy, especially the Fed on Wednesday night.

This is an exceptionally active week in monetary policy, with no less than eight relevant central banks due to meet over the next few days. The first is the Sveriges Riksbank on Tuesday from 7.30 GMT with a triple hike to the repo rate expected.

The Swiss National Bank and the Norges Bank meet on Thursday, with the former likely to take its rate above zero for the first time in a decade and the latter expected to call for a double hike. Also on Thursday, the Bank of Japan is seen keeping its rate on hold at negative 0.1% and the Central Bank of the Republic of Turkey also no change at 13%, while the consensus for the South African Reserve Bank is a triple hike to 6.25%.

However, these meetings are all overshadowed by the Federal Open Market Committee’s statement and press conference from 18.00 GMT on Wednesday and, to a lesser extent, the Bank of England from 11.00 on Thursday. As of the evening of 19 September, the chance of a triple hike by the Fed was around 85% according to CME FedWatch Tool, so this has been mostly priced in. Traders will concentrate on comments from Jerome Powell to determine how high the Fed might end up by the end of the year and what the outlook for the American economy might be in the coming months.

Similarly the Bank of England seems nearly certain to call for a double hike to 2.25%. Comments from Andrew Bailey and the MPC in general are also key here, especially given that British annual non-core inflation unexpectedly declined in August to 9.9%.

Monetary policy is certainly the main event this week, but traders are also looking at some important items of regular data. These include Canadian inflation early on Tuesday afternoon and British consumer confidence on Thursday night. Overall, it’s likely to be a very active few days for most markets from the Fed’s meeting.

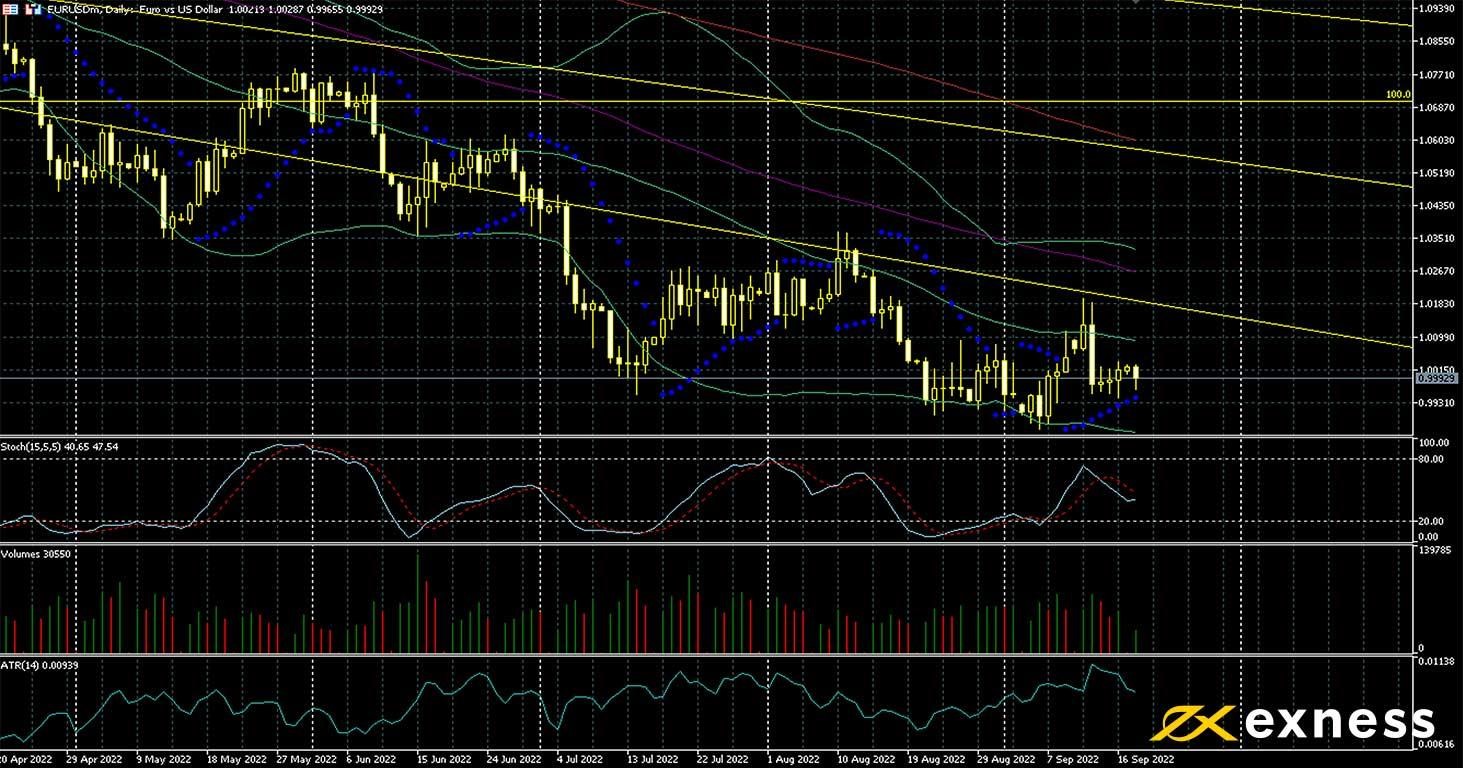

Euro-dollar, daily

Euro-dollar corrected quite sharply lower after last week’s surprisingly high American inflation. This symbol’s fundamentals haven’t changed significantly in the last few weeks: both central banks remain seemingly very hawkish although the Fed was quicker on the ball to hike rates, while the energy crisis will probably continue to have a much bigger effect on the eurozone than the USA. It seems very likely that the eurozone will also enter recession within the next few quarters, but the ECB has been careful not to sound too negative on the current economic slowdown.

Parity, i.e. exactly $1, remains the key technical reference with no immediate sign of momentum below. That’s normal in the context of an upcoming meeting of the Fed, but the range between the latest low and the 50 SMA is now less than two cents, so logically the price has to break out one way or another at least to some degree this week. Above the 50 SMA around $1.01, any round number in the value area below the 100 SMA might be an important resistance, while a breakout definitively below 99c looks unlikely this week unless the Fed surprises everybody and calls for a four-step hike or sounds suddenly even more hawkish.