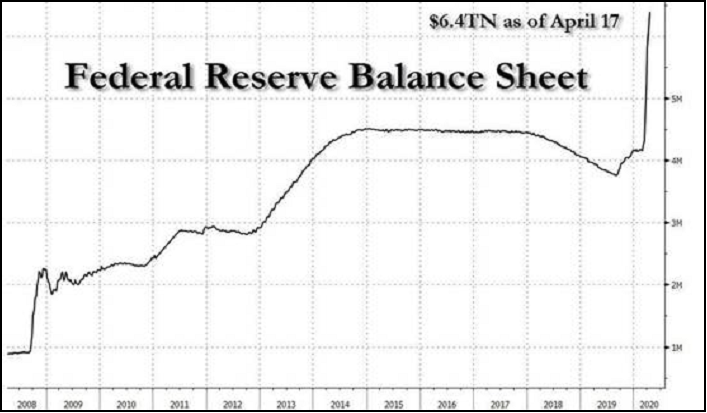

Strange times may call for stranger measures, but the Fed has caused alarm among economic observers by slashing interest rates to zero and re-inventing the definition of qualifying assets for QE repurchases. The Fed has recently expanded its balance sheet by over 50%, adding liquidity to repo markets and to junk bonds, as well. Such a dramatic departure from traditional policy measures has re-ignited debates in several quarters, including whether Bitcoin will truly be a “safe haven” asset in times ahead.

Chart provided courtesy of Wealth Research Group

When the full impact of the COVID-19 pandemic hit financial markets, it was sink-or-swim time across all global venues. In crisis mode, Bitcoin joined other equity classes and plummeted on cue, leaving any semblance of “safe haven” status in its torrid wake. BTC skeptics and especially “Gold Bugs” were quick to gloat that Bitcoin was an imposter, when it came to protecting portfolios. Forbes, however, touted a Delphi Digital report that revealed that Bitcoin had outperformed every asset class over the past year.

Kevin Kelly, Delphi’s lead analyst, noted that Bitcoin’s performance year-over-year had yielded a 40% return, despite its recent fall from grace. He added: “There are a handful of asset classes boasting positive returns this year and crypto is one of them. Bitcoin’s latest rebound pushed its year-to-date return back into the black as investors continue to digest countless headlines surrounding monetary and fiscal policy responses to COVID-19. We often remind ourselves to take a step back as arbitrary time horizons can muddy or even mislead investors.”

What about Gold and precious metals? Were they not stellar performers over the previous twelve-month period? Per Kelly: “There are a few subsets of asset classes that have outperformed BTC, like palladium for example, even though precious metals as a group have not.” In times of crisis, however, when investors are looking for cash from any sector to cover margin calls and necessary expenses, Bitcoin demonstrated that it would suddenly react in correlation with equities. Kelly explains: “If stocks sell-off, it wouldn’t be the first (or the last) time bitcoin follows suit.”

Crypto industry observers have pondered for the past year how Bitcoin might react when a recession materialized. The COVID-19 pandemic has delivered the answer: the volatility and risk aspects of the crypto asset required that it correlate heavily with the S&P 500 index. The question, however, is whether Bitcoin will resurrect its “safe haven” asset status when central banks suddenly react to the crisis by opening the printing presses full bore for expanding money supplies globally?

Since the supplies of Bitcoin are limited and therefore scarce, the overriding principle has been that BTC valuations should rise if global fiat currencies are diluted, the basic premise of Bitcoin in the first place. Analysts at CoinDesk have asserted that Bitcoin’s “safe haven” status remains intact. Per one analyst, Osho Jha: “People think bitcoin lost its safe-asset use case but this liquidity crunch and ensuing government intervention is laying the foundation for bitcoin’s adoption as a safe-haven asset.”

In summary, Bitcoin’s recent correlation with equities has been driven purely by a liquidity crisis in which all asset classes react abnormally. The IMF, in its recent “World Economic Outlook” report, has predicted a 3% year-over-year recession in 170 countries, “the worst economic downturn in 90 years and predicting a total of nine trillion dollars of losses by 2022”. The group forecasts a mild recovery in 2021, but will Bitcoin and Gold, for that matter, break from their recent tight correlation with the S&P 500?

In a recent report, Coinmetrics predicts that the correlations will break down, as central banks in lockstep expand their respective national money supplies: “Although correlations recently reached all-time highs, it is unlikely that Bitcoin and S&P 500 correlations will remain elevated in the long-term without major changes in the fundamentals of one or both markets.”

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.