From a traditional perspective, Bitcoin has always been a mystery, refusing to fit nicely within standard definitions of what constitutes an investment worthy security. Often referred to as “Digital Gold”, Bitcoin does not always act like its “safe haven” cousin, but on occasion, it does. Bitcoin began as a payment device, but it soon morphed into a handy investment tool for hedging the dilution of fiat currencies by central banks across the globe. The COVID-19 pandemic has only heightened the debate, since under these times of stress, BTC correlated highly with the S&P 500 index, a surprise to many.

Whatever the driving reasons might be, however, a bevy of analytical reports from the likes of the research arm of the Kansas City Federal Reserve Bank and two researchers with the Oxford University Law Faculty blog were published in the past few days. As much as these reports would have liked, each failed to force Bitcoin into a neat little box where its pricing behavior and risk aspects could be easily understood versus a conventional backdrop of situational data in the marketplace.

Analysts from the Federal Reserve Bank of Kansas City recently tackled the issue of “safe haven” status that has been bandied about in various debates of late. The study was performed, however, within the context of their strict definition of a “safe haven” asset: “An asset is considered a safe haven if it is uncorrelated or negatively correlated with riskier assets during times of stress.”

Within these tight confines, the result of the Fed’s analysis was a foregone conclusion: “Overall, our results suggest that the 10-year Treasury has generally exhibited safe-haven behavior, gold has occasionally exhibited safe-haven behavior, and Bitcoin has never exhibited safe-haven behavior since its introduction.”

Crypto enthusiasts generally object to these findings, preferring to discuss Bitcoin’s “store of value” concept as an evolving characteristic. Cryptoglobe noted that Charles Hayter, Co-Founder and CEO of CryptoCompare, a leading crypto market data provider, had said: “Its risk-off across the markets — Bitcoin is still novel, and is great as a means of transferring value quickly, person to person, but bad at holding value. The theory is that, with time, this will change but quite clearly it has nascent fragmented markets at present and isn’t fulfilling the digital gold story.”

The key point here is “with time”. Bitcoin today has not achieved “Digital Gold” status, but the chorus from industry observers is “not YET”. The other factor in question is the use of the phrase “during times of stress”. The Fed focused on risk assets and how they react to stress, but the group did not pose the situation where fiat currencies were “under stress”. If major currencies are diluted, as they surely will be by an assortment of stimulus programs designed to combat the effects of COVID-19, then Bitcoin will easily become a safe haven and store of value during those troubled times.

This line of reasoning is borne out by the study conducted by researchers with Oxford University. The result of this study is that Bitcoin could pose a threat to traditional financial markets. Per the report: “In a nutshell, if, as our findings suggest, investors initially view the crypto market is a substitute for the traditional financial markets in times of crisis, then regulating it can help in preventing systemic risk to the “real” financial markets.” The researchers also noted that halting crypto markets during such a time of stress could prove to be “mission impossible”.

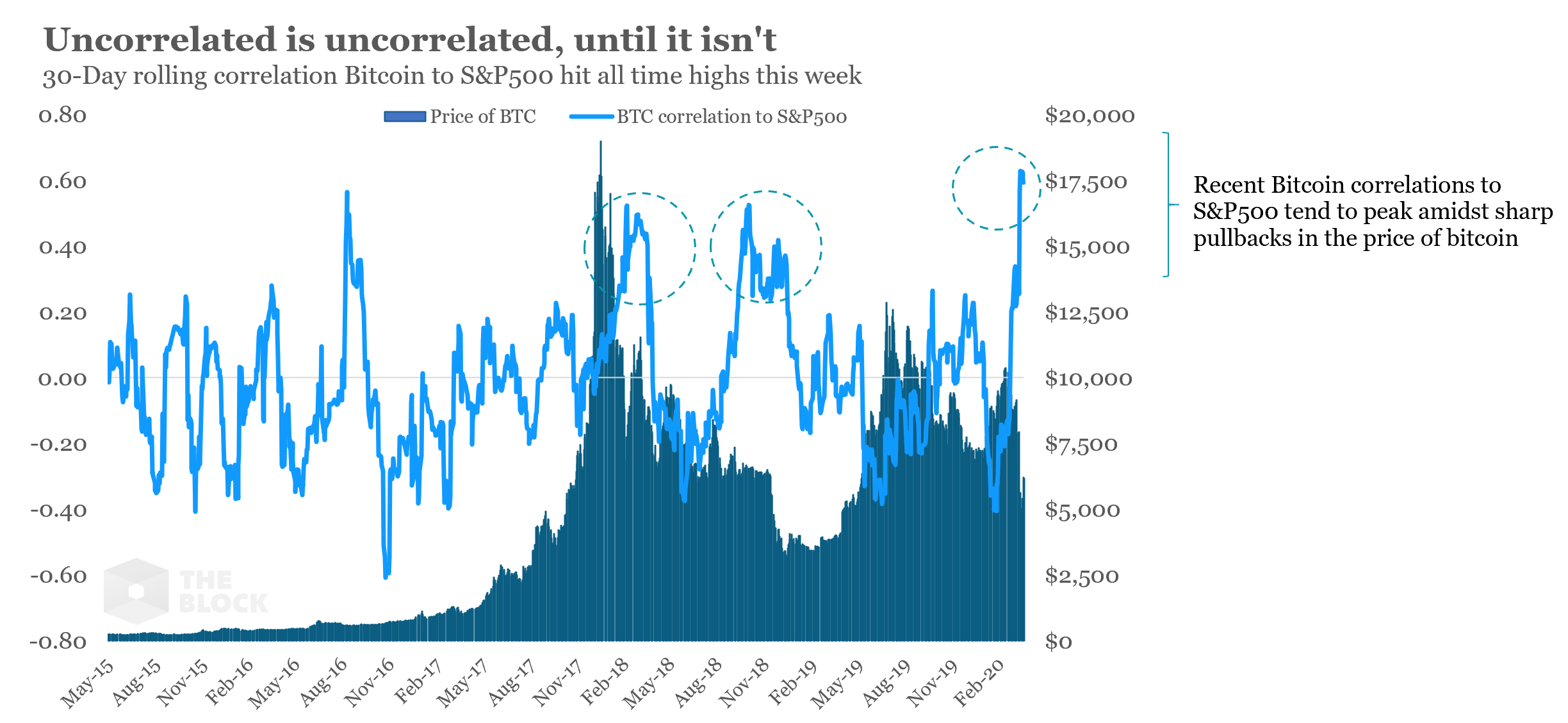

Bitcoin will remain a mystery for traditional analysts, since it does not always correlate one way or the other. The Block recently prepared the following graphic, which demonstrates that Bitcoin has correlated with the S&P 500 index both negatively and positively over time. The recent peak, as depicted below, is but a recent phenomenon.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.