This article was submitted by Michael Stark, market analyst at Exness.

Positivity has generally remained high in most markets today as traders continue to wait for news of the American government’s stimulus package being confirmed. However, signs of inflation have dented sentiment somewhat on shares as some participants consider monetary tightening this year less unlikely. This preview of weekly forex data looks at EURNZD, BTCUSD and USDTHB.

Major central banks were inactive last week, and this week seems likely to be similar except for the Reserve Bank of New Zealand. The RBNZ meets on Wednesday morning local time, so pairs with the Kiwi dollar are likely to be active from midnight GMT on Wednesday. Some minor central banks – Israel and Hungary – are also due to meet over the next few days.

The only critical economic data due this week is tomorrow morning’s claimant count change from the UK. Important releases elsewhere include German GfK consumer confidence and American durable goods, income and spending. This isn’t a particularly big week of data except in New Zealand, so traders can probably expect sentiment, political news and technical developments to dominate over the economic calendar for many symbols.

Euro-Kiwi dollar, daily

Nothing much has changed for EURNZD’s fundamentals in February so far: economic data affecting both currencies continue to recover and monetary policy shows no signs of tightening anytime soon. However, the Kiwi dollar does generally do better during ‘risk on’ moods and its sensitivity to trade has been a boon over the last few weeks as the outlook for Chinese demand has improved significantly.

The obvious pivot point on this chart is the 100% weekly Fibonacci retracement area, i.e. complete retracement of all the euro’s gains in March 2020. A clear breakout below $1.655 might trigger another leg down over the next few weeks. On the other hand, with price having been generally oversold or close to it for a number of months, this might be a logical place for a bounce.

None of this week’s data are guaranteed to be catalysts given that the focus now is on inflation and sentiment, but the sheer volume of key releases from New Zealand means that the Kiwi dollar is likely to be highly active over the next few days. While the RBNZ’s meeting will probably bring some short-term volatility, a significant change to monetary policy or economic projections is not favourable. Retail sales, balance of trade and various other figures from New Zealand could provide short-term opportunities in both directions.

Key data this week

Bold indicates the most important releases for this symbol.

00 GMT: French total jobseekers (January) – consensus 3.61 million, previous 3.59 million

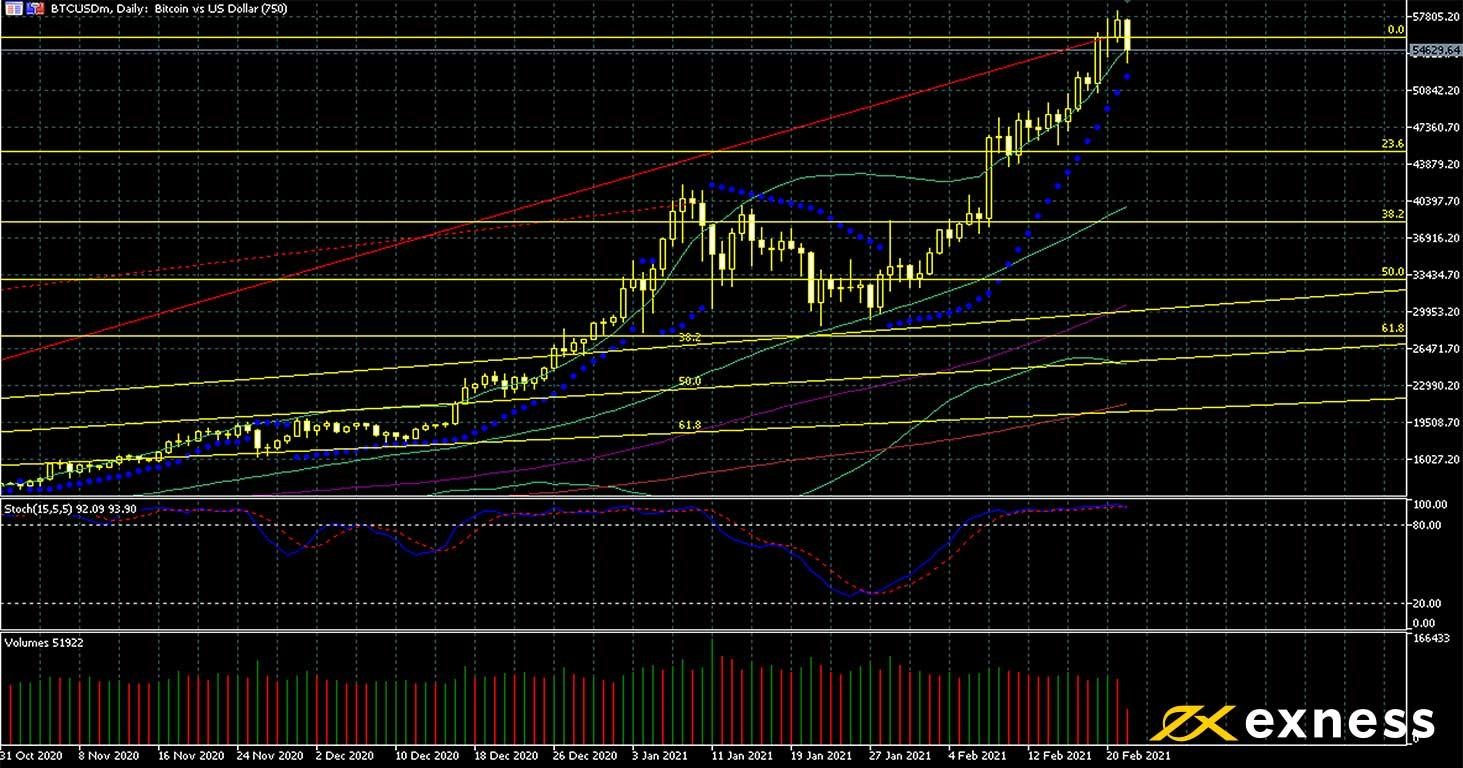

Bitcoin-dollar, daily

Bitcoin has moved down somewhat so far this week as some participants appear to be concerned about overvaluation. However, as with any cryptocurrency, fundamental analysis is never much more than guesswork.

From a technical point of view, a consolidation had been coming for some time. Price has extended strongly beyond the weekly Fibonacci fan and remained overbought or close to it since basically the beginning of Q4 2020. The initial support might come from the 23.6% weekly Fibonacci retracement area just above $45,000. However, it is of course possible that many new buyers might want to enter after even a small retracement.

Any further news this week about the American government’s new fiscal stimulus will certainly be important. Equally, data on inflation in the eurozone (see above) might affect bitcoin given its increasing role as a hedge. Ultimately, though, trying to analyse bitcoin through the lens of political news and economic data is extremely difficult.

Dollar-baht, daily

The dollar appears to have stabilised against the baht since the fourth quarter of 2020, The decrease in political uncertainty in Thailand over the last few months has also reduced negative sentiment on THB, while some positivity for the dollar from rising yields of American bonds has played a role in preventing further losses here.

Summer 2020’s important support around 31 has clearly been broken, with the emphasis now on the 100% weekly Fibonacci retracement area as above with EURNZD. If this is clearly breached, one might expect the price of dollar-baht to track the 61.8% area of the weekly Fibonacci fan more closely. Despite price having now moved above the 50 SMA from Bands, the signal from moving averages remains clearly ‘sell’.

Numerous figures are due this week from Thailand and a few significant ones from the USA. Thai balance of trade on Tuesday morning probably has the biggest potential to drive a breakout from the recent range, but Thursday and Friday’s releases might also be key clues as to the baht’s direction in the next few weeks.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 23 February

30 GMT: Thai balance of trade (January) – consensus $70 million, previous $960 million

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.