This article was submitted by Michael Stark, market analyst at Exness.

The fresh collapse of the lira this morning has dominated news from markets so far this week. Turkey’s President Recep Erdogan sacked the head of the Central Bank of the Republic of Turkey Naci Agbal on Saturday morning, sparking panic among investors in Turkish bonds and shares from today’s open. This preview of weekly forex data looks at two tradable emerging currencies, the baht and the peso, plus gold.

Last week’s most important news from central banks for emerging markets was the CBRT’s 2% hike of its one-week repo rate, taking the rate to 19%. The sum of hikes over Dr Agbal’s tenure was 8.75%, one of the main factors driving the sudden decision to remove him. Elsewhere, the Central Bank of the Russian Federation also raised its key rate to 4.5% last week, a hike of 0.25%. The central banks of Thailand, Hungary, the Czech Republic, Switzerland, South Africa and Mexico all meet this week.

Yields from major benchmark bonds have generally declined negligibly so far this week. The USA’s decade T-bond has held around 1.7%. However, German bonds moved up very slightly while remaining below negative 0.3%. The main regular data this week are tomorrow morning’s claimant count change followed by British inflation, American durable goods, and German consumer confidence.

For emerging markets specifically, there is a particularly large number of important figures due this week. These include Mexican and Thai job data and balances of trade plus South African inflation.

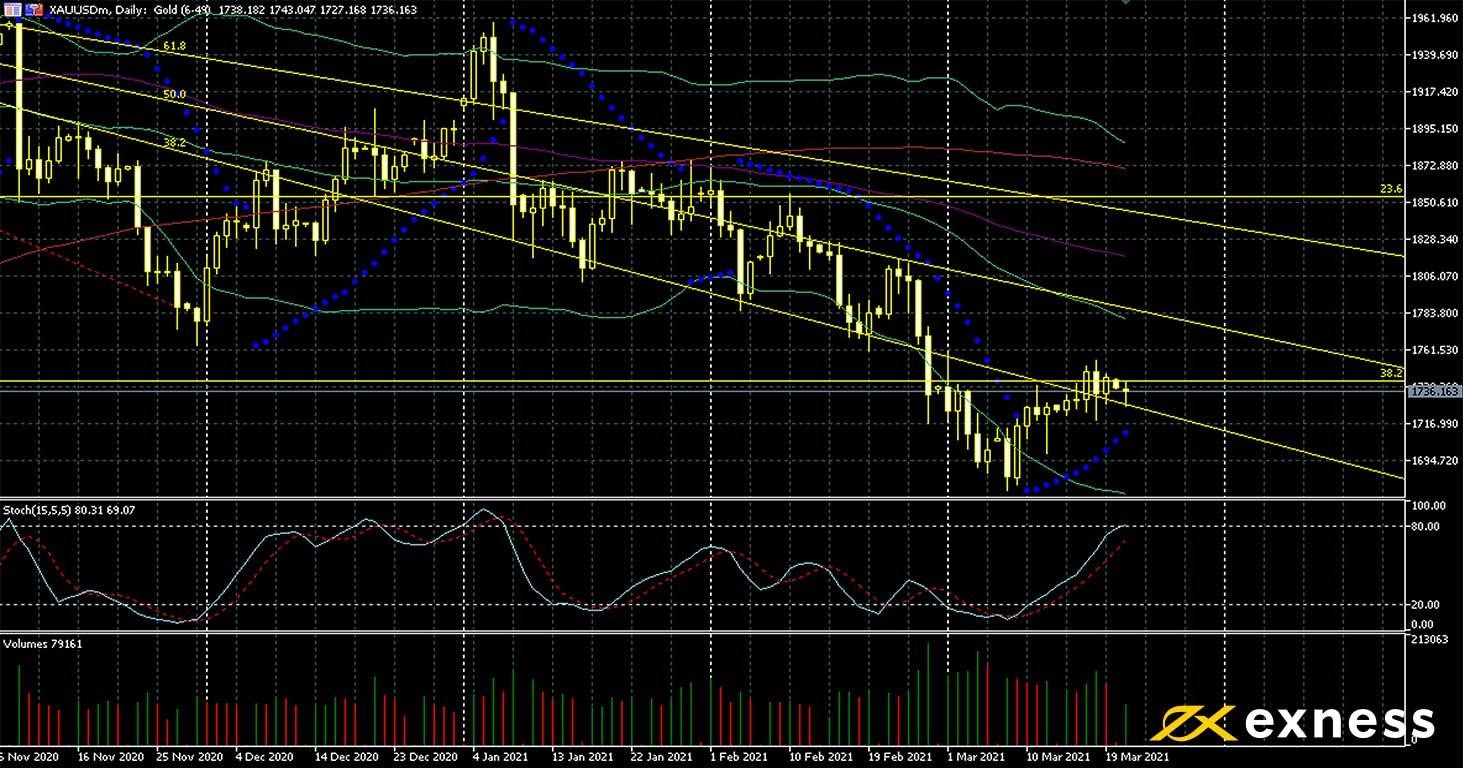

Gold-dollar, daily

Last week’s meeting of the Fed didn’t have a very strong effect on the price of gold, but the yellow metal does seem to have found support for now around the psychological area of $1,700. The Fed’s chairman Jerome Powell stressed the need for strong, ongoing monetary support and noted that changes to policy would need to be justified by actual data as opposed to projections. More generally, ‘risk on’ seems to be holding as American shares generally moved up yesterday afternoon.

From a technical point of view, gold’s downtrend is still active, with the 100 SMA having moved further below the 200 and a new low having been reached on 8 March. Now that there is no longer an oversold signal from either Bollinger Bands (50, 0, 2) or the slow stochastic (15, 5, 5) – the latter being slightly inside the trigger zone for overbought this afternoon – another leg down can probably be expected over the next few weeks in the absence of significant changes in sentiment or surprises from data.

30 GMT: American personal income (February) – consensus negative 7.3%, previous 10%

30 GMT: American personal spending (February) – consensus negative 0.7%, previous 2.4%

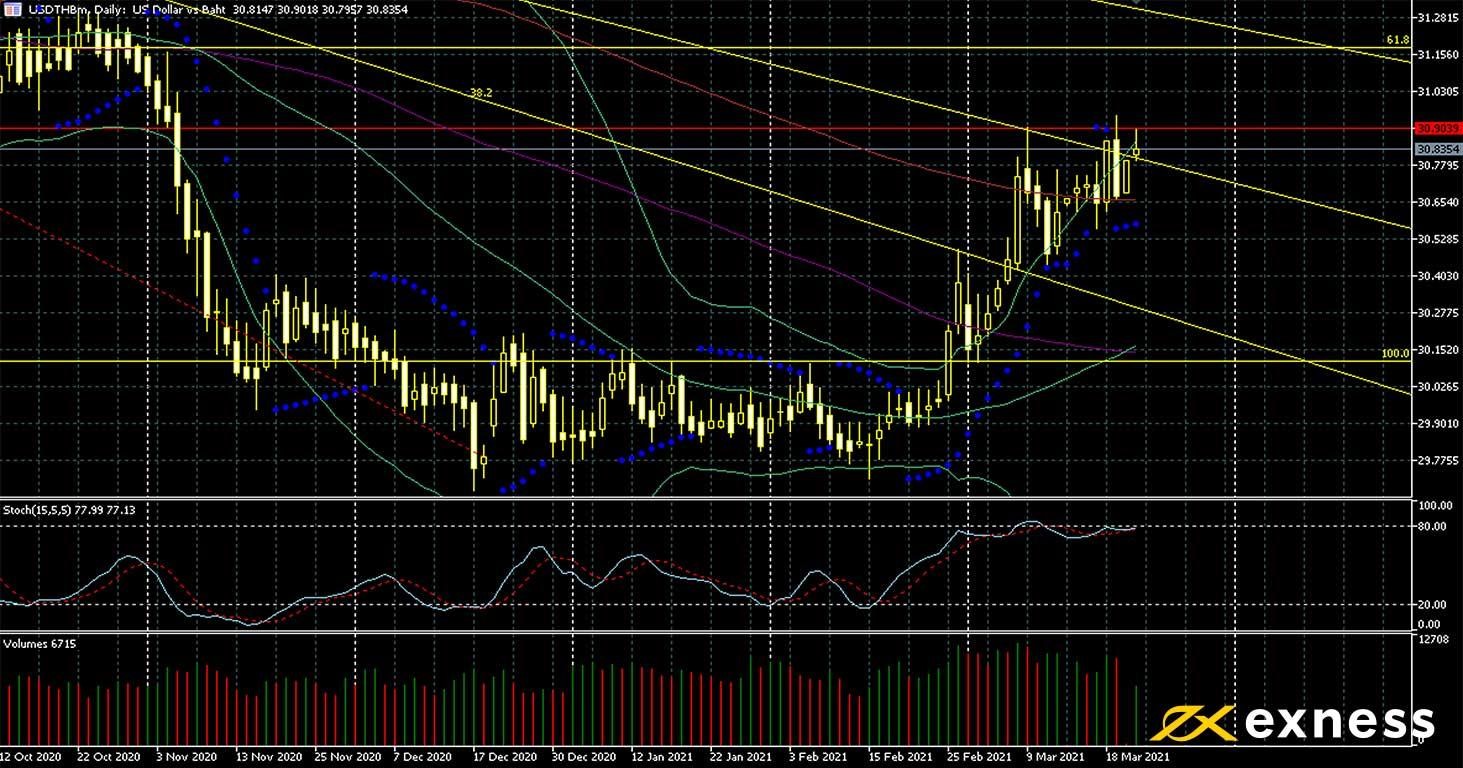

Dollar-baht, daily

Much like other emerging currencies, the baht has retraced downward recently against the dollar as the outlook for the latter has improved. Data from Thailand over the last few weeks has also been generally disappointing, with annual deflation reaching more than 1% last month and core inflation very close to zero.

Price is currently testing the 50% area of the weekly Fibonacci fan, with the potential for a move higher depending on the reaction to the Bank of Thailand’s meeting on Wednesday morning GMT. No change to the current repo rate of 0.5% is expected but commentary on the outlook for the Thai economy over the next few months is likely to be in focus for this symbol.

Key data this week

Bold indicates the most important releases for this symbol.

30 GMT: American personal income (February) – consensus negative 7.3%, previous 10%

30 GMT: American personal spending (February) – consensus negative 0.7%, previous 2.4%

Euro-peso, daily

EURMXN’s sideways trend has continued so far this year as both currencies remain relatively strong against the US dollar compared to the average for most of 2020. While American light oil has made several new highs in 2021 so far and remains above $60 at the time of writing, Mexican employment data and balance of trade for January were very weak and participants here appear to be unwilling to commit significantly.

Despite the euro’s gains late last month amid disappointing economic figures from Mexico, the sideways trend seems to have been confirmed by the retreat from areas just above the 23.6 weekly Fibonacci retracement area over the last few weeks. Price is now within the value area between the 100 and 200 SMAs and shows no clear sign of moving lower, though, especially with the oversold signal from the slow stochastic.

The Banco de Mexico is unlikely to change its benchmark rate on Thursday night GMT but as usual for central banks there could be volatility around the meeting, especially as a result of comments on the outlook for inflation and GDP over the next few months. Volatility for most pairs with the peso is also likely to be high around Wednesday’s job data and Friday’s balance of trade.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.