This article was submitted by Michael Stark, market analyst at Exness.

Today’s key news so far affecting derivative markets has been the partial refloating of the Ever Given, the large container ship that has blocked the Suez Canal since last Tuesday. Expectations among some participants that crude oil might move strongly upward if the blockage dragged on have failed to materialise so far, so regular stock data and Chinese PMI might be key for oil this week. Meanwhile on Friday non-farm payrolls is likely to drive high volatility for most instruments. This preview of weekly forex data looks at UKOIL, USDCHF and XAUUSD.

Last week was mostly inactive in monetary policy, with Mexico, South Africa and other countries’ central banks leaving rates on hold as expected. There’s also no significant meeting of any central bank due this week.

The most important release in view this week is of course Friday’s NFP, but NBS manufacturing PMI and Caixin manufacturing PMI from China on Tuesday and Thursday respectively are likely to be key for crude oil in particular. Australia’s balance of trade early on Thursday morning rounds off the major data.

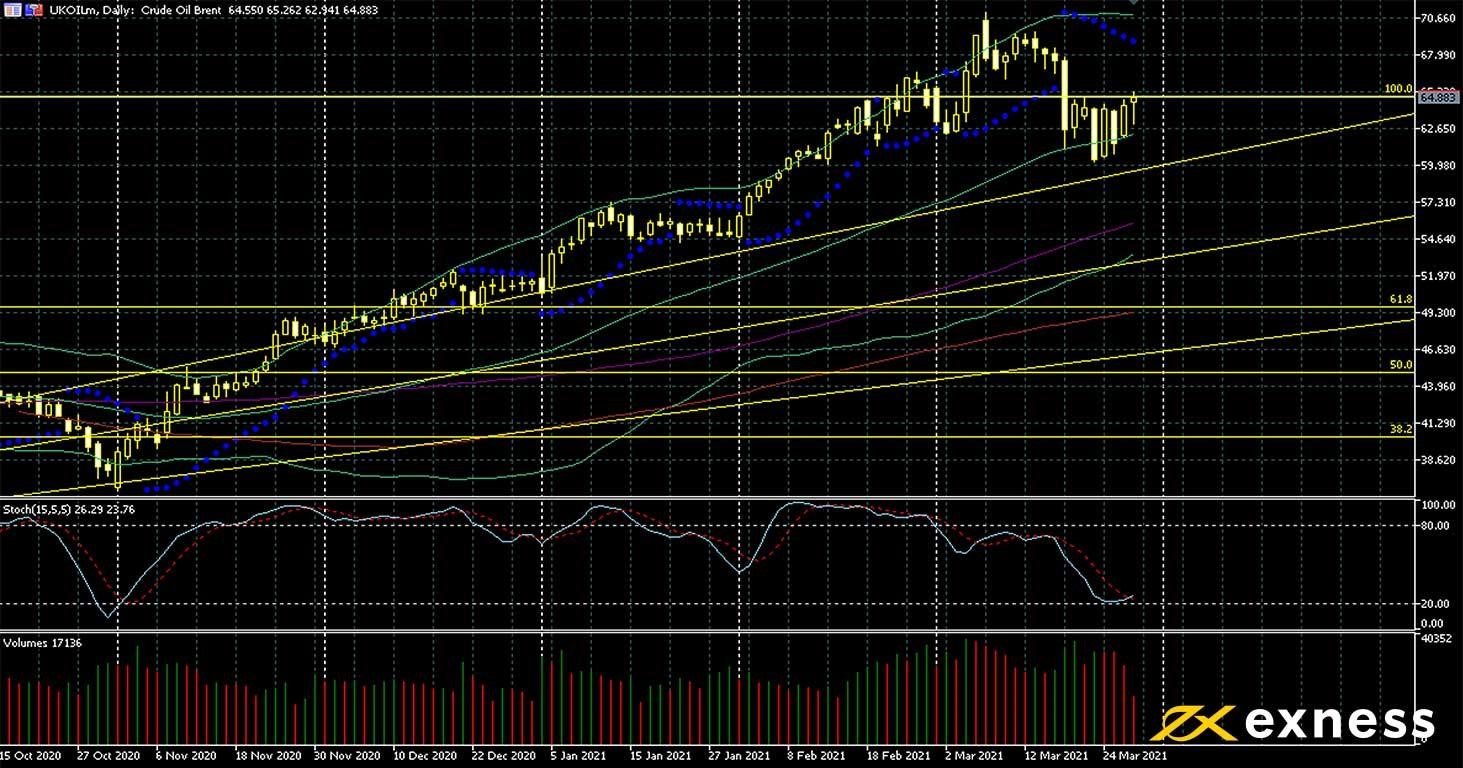

Brent, daily

Oil has generally held its strength so far this week despite the partial refloating of the Ever Given in the Suez Canal. In the second half of last week, various participants in commodity markets had expected strong gains by oil if the blockage had dragged on given that much of Europe’s requirements for crude are imported from the Gulf. However, ongoing low demand and relatively high stocks of oil across the continent remain negative factors, while there is strong evidence of American stocks and production both having risen overall in the first quarter of 2021.

From a technical perspective, oil’s uptrend since last summer is clearly still active for now. Brent has failed to break below the 50 SMA from Bands, and there is currently no indication of overbought from either Bollinger Bands (50, 0, 2) or the slow stochastic (15, 5, 5). The key area on this chart for the next few days is likely to be the 100% weekly Fibonacci retracement area, i.e. full retracement of all losses since late January 2020. Apart from Chinese PMI and of course the NFP, traders will continue to look at regular stock data and Baker Hughes’ rig count this week for clues on whether the uptrend might continue.

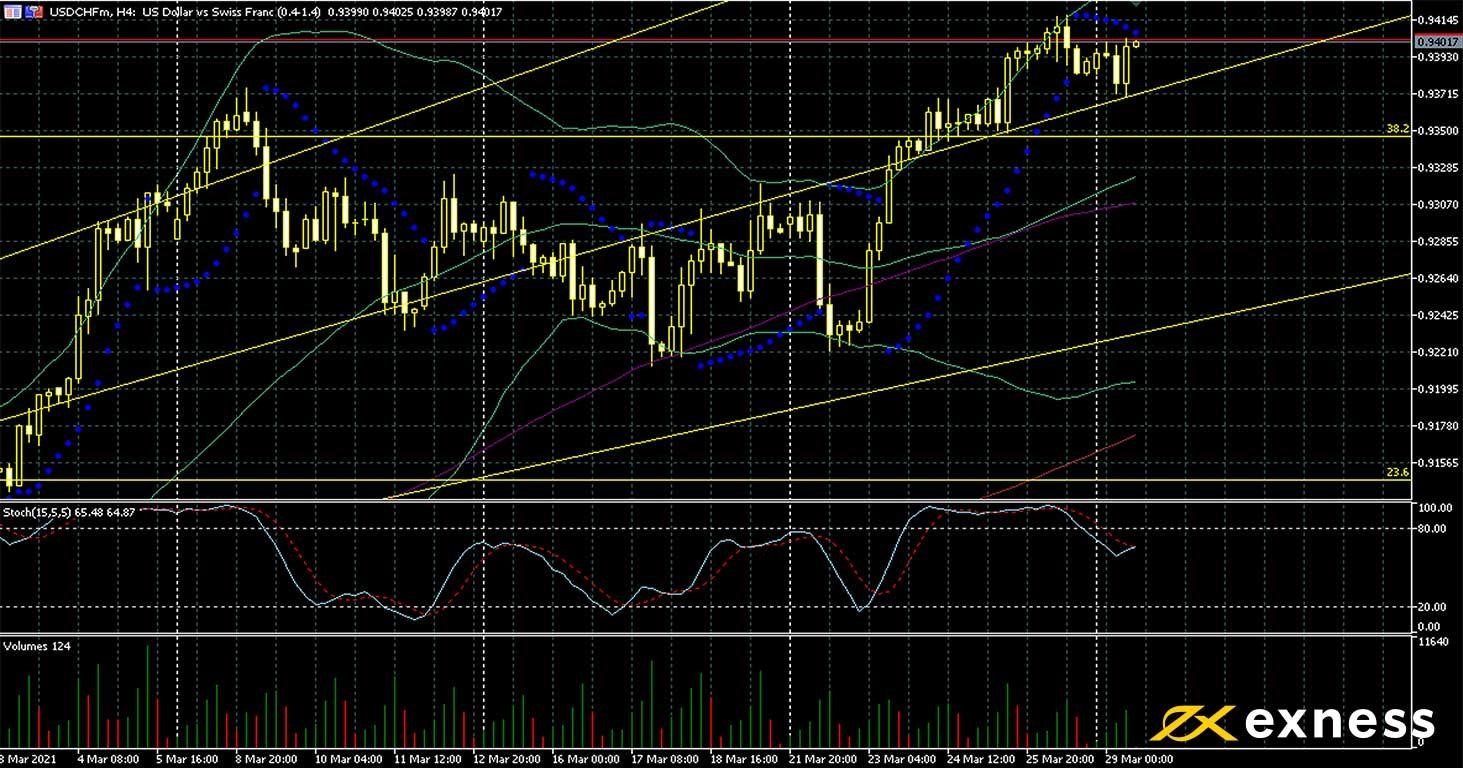

As against many other currencies, the dollar has been making gains against the franc overall in 2021 so far as ‘risk on’ remains in vogue and traditional havens have declined. Yields from benchmark decade Treasury bonds have increased significantly and remained above 1.6%. The outlook for economic recovery in the USA has also generally improved over the last few weeks.

Although volume for dollar-franc has not been especially high over the last few weeks, it has been dominated clearly by buying. On the four-hour chart, there is currently no overbought signal: the slow stochastic is closer to neutral than the zone of buying saturation at about 63. The obvious target for buyers is the upper area of the daily Fibonacci fan around 95 centimes, but data this week make an extended consolidation possible, especially in the case of a negative surprise from the NFP.

Key data this week

Bold indicates the most important releases for this symbol.

30 GMT: American annual average hourly earnings (March) – consensus 4.5%, previous 5.3%

Gold-dollar, daily

Gold has made small losses so far this week in the context of its inverse correlation with the US dollar: ongoing high yields from American bonds and a better outlook for the economy have dented sentiment somewhat. Recent declines by gold have also matched losses by haven currencies, primarily the yen and the franc.

Momentum downward for XAUUSD has been somewhat lower since last week when price moved back inside the lower area of the weekly Fibonacci fan. Volume though does not currently confirm the trend, with indications of high demand for buying during bouts of strong losses. A disappointing NFP this week would probably make the value area between the 50 and 100 SMAs the first clear resistance, but to some extent we might also expect Chinese PMI data (see above) to have an effect on the price.

Key data this week

Bold indicates the most important release for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.