This article was submitted by Michael Stark, market analyst at Exness.

This week started slowly with holidays in the USA and the UK. Recent data on food inflation in the USA has brought the narrative of commodities’ bull run back into focus, though, and a more active end of the week is likely as traders await Friday’s non-farm payrolls. This preview of weekly forex data looks at XAUUSD, UKOIL and GBPZAR.

There was no significant activity among central banks last week; the last notable change to policy in a major economy was the Central Bank of the Russian Federation’s hike of its key rate by half a percent to 5% the week before. The main event in the calendar for monetary policy this week is the meeting of the Reserve Bank of Australia early tomorrow morning GMT. A hold of the cash rate at its record low 0.1% seems all but certain. However, traders are likely to monitor any comments from members of the Federal Open Market Committee this week given the return of inflation to many participants’ concern.

The consensus for Friday’s NFP currently stands at about 650,000. Apart from this key release, other important events this week include tomorrow morning’s Caixin manufacturing PMI from China and Australian balance of trade on Thursday morning. Regionally important releases are dominated by South African unemployment data tomorrow and Turkish annual inflation on Thursday.

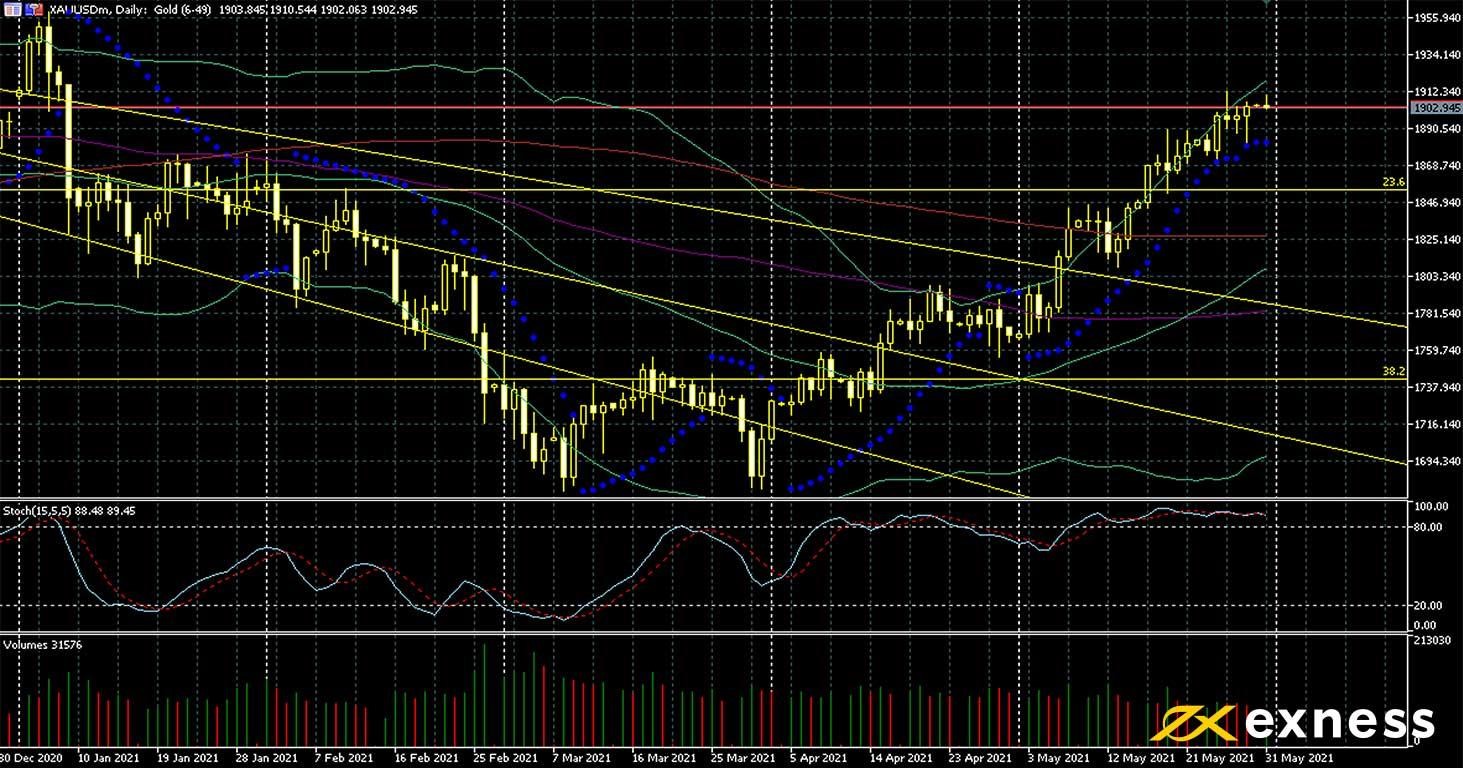

Gold-dollar, daily

Gold continued to shine last week as large participants generally moved forward with rotating out of crypto and into the yellow metal. That was the fourth consecutive week of gains, with $1,900 being a four-month high. Stimulus and inflation remain active as factors while American bonds have eased slightly over the last few sessions.

The golden cross of the 50 SMA over the 100 a fortnight ago came ahead of more gains, although price has now moved clearly into overbought based on the slow stochastic (15, 5, 5). The weekly Fibonacci fan has probably lost relevance now that the medium-term trend is clearly upward, but 61.8% might still limit a fairly deep retracement.

An obvious target for the bulls here would be January 6th’s high just below $1,960. However, gold probably has more room to fall than gain in the immediate future. Another negative NFP is of course possible, but buying in with the stochastic around 90 and momentum seeming to drop is a significant risk.

Key data this week

Bold indicates the most important release for this symbol.

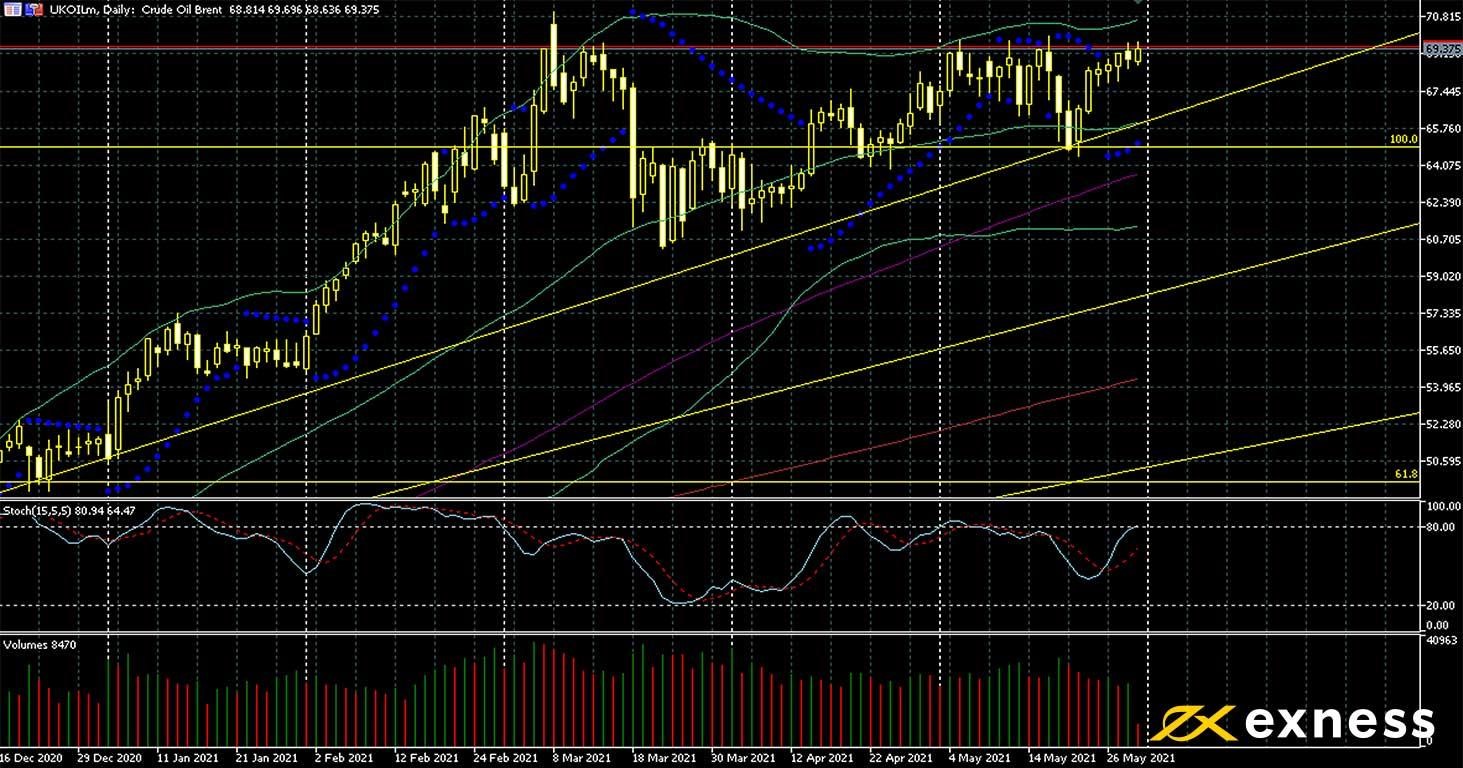

Sentiment generally remains positive on crude ahead of OPEC+’s meeting tomorrow. The outlook for demand is still relatively positive considering the circumstances but the cartel and its allies are likely to maintain the current cuts to production. The wildcard in terms of events for crude is a possible breakthrough in American-Iranian negotiations: loosening of sanctions could see Iran add an extra two million barrels per day to total supply.

$70 remains a very strong psychological resistance, but it’s possible that tomorrow’s meeting could boost sentiment and lead to a breakout upward. Intraday losses in the event of a negative reaction might be capped by the 50 SMA around $66.10.

Apart from OPEC+ and the NFP, this week’s regular stock data from the API and EIA might drive volatility for oil. Equally, another gain in Baker Hughes’ rig count might dent sentiment on Friday night.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 1 June

all day: 17th OPEC and non-OPEC Ministerial Meeting

South Africa’s intensification of restrictive measures against transmission of covid-19 starting today haven’t had a clear impact on the rand yet. Despite the generally better picture for the British economy and voices from the Bank of England predicting earlier rate hikes than expected next year, South Africa’s role as an exporter of in-demand commodities seems to be taking traders’ attention for this symbol: South African balance of trade earlier today at over R51 billion beat the consensus by more than R20 billion.

The 61.8% weekly Fibonacci retracement area is an important support which is still being tested. Most of the time, second and third tests are less likely to succeed, so it’s possible that a bounce might be observed over the next few days barring major good news from South African data. R20 would be a key psychological zone if this happened, while to the downside R19 might be an important support based on 20 December 2020’s low.

Key data this week

Bold indicates the most important release for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.