This article was submitted by Michael Stark, market analyst at Exness.

Various markets started this week positively as participants await the passing of new fiscal stimulus in the USA and Tesla disclosed its purchase of $1.5 billion worth of bitcoin. This preview of weekly forex data looks at EURUSD, US500 and UKOIL, the latter two having reached significant new highs this morning GMT.

Overall strong employment data considering the circumstances from the USA on Friday has strengthened the current ‘risk on’ mood, with American index futures reaching new highs and traders now looking ahead to key inflation data on Wednesday afternoon GMT. Other important regular data this week include balance of trade from Germany and the UK plus sentiment in Australia.

The central banks of Sweden, Mexico and Russia all meet this week, with all expected to keep their base rates on hold at nil in Sweden and 4.25% in Mexico and Russia. Generally, monetary policy continued to take a back seat to sentiment and rumours of fiscal stimulus last week.

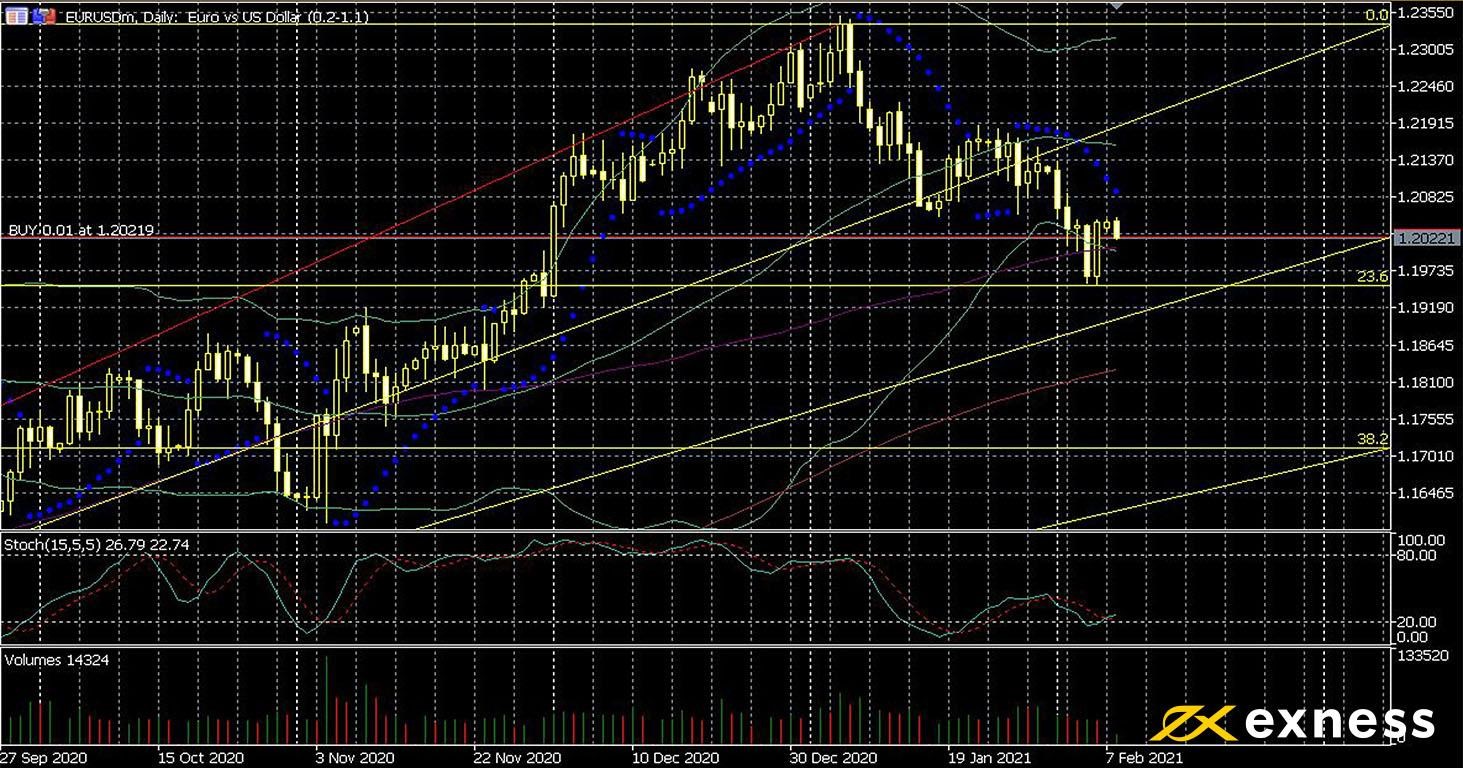

Euro-dollar, daily

The euro remains close to two-month lows against the dollar so far today amid a degree of general positivity on the dollar, relatively high yields from American bonds and expectations for a quicker economic recovery due to upcoming fiscal stimulus. Major European economies continue to struggle, with German industrial production stagnant and Spain contracting slightly in December.

From a technical perspective, the uptrend still seems to be active on this timeframe: there has been no clear breach of the 100 SMA. However, price has now moved out of oversold based on both Bollinger Bands (50, 0, 2) and the slow stochastic (15, 5, 5), so more losses this week might be expected unless German balance of trade is unexpectedly strong tomorrow. As always, though, sentiment can be fickle: if the Democrats’ stimulus is passed, one might see ‘buy the rumour, sell the fact’.

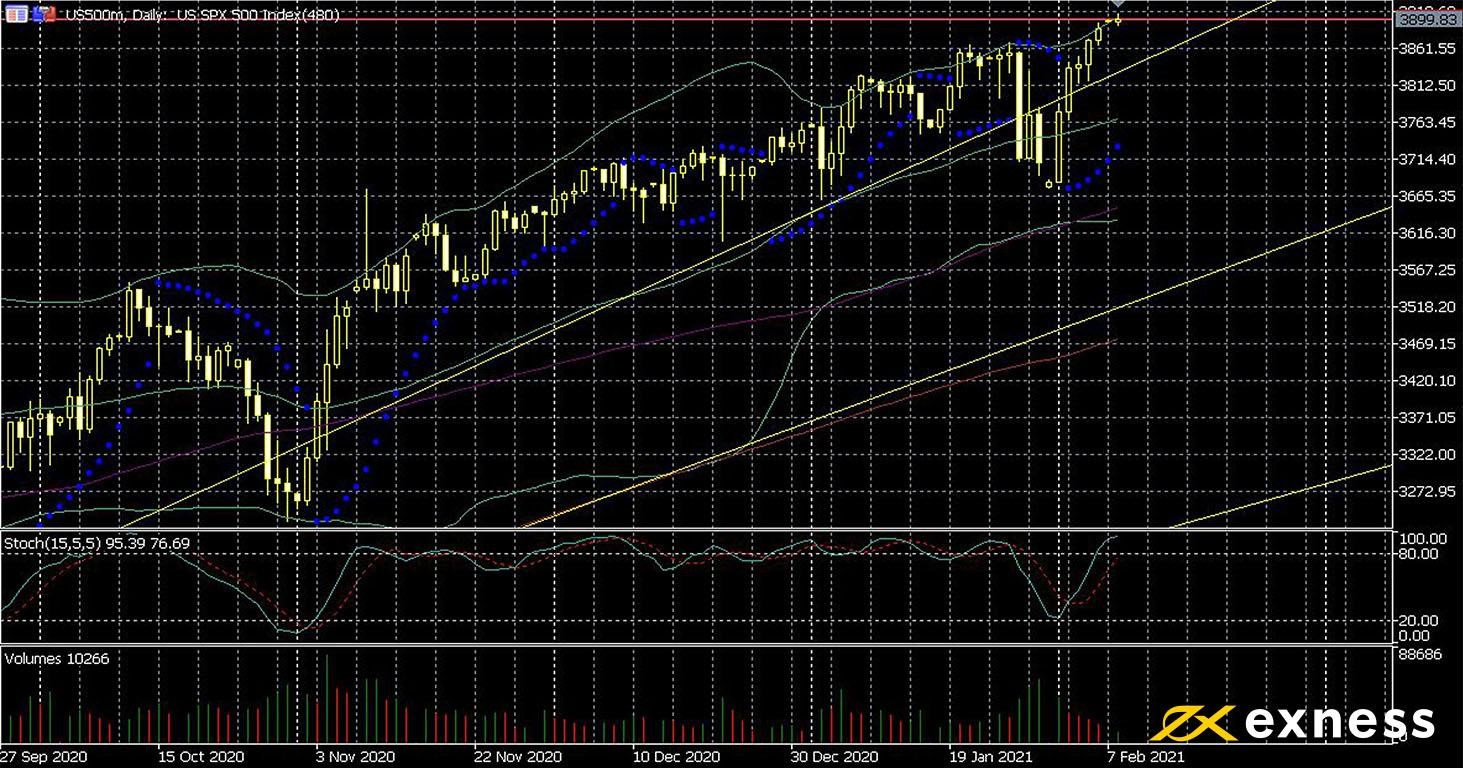

US500, the representative CFD based on the S&P 500, has continued to make strong gains since the start of last week and reached a new all-time high today of around 3,900. As elsewhere, record loose monetary policy and high hopes for new fiscal stimulus have boosted sentiment, but now nearly every constituent of the index has posted gains recently as traditional defensive shares return to favour.

The next clear resistance is the psychological area of 4,000. While there is no sign of lower momentum just yet, US500 has been strongly overbought since early November. Traditionally, a consolidation would be expected in the near future, since prices don’t typically continue in one direction for such a long time. The 50, 100 and 200 SMAs are some of the main areas in focus to the downside, but the 50% zone of the weekly Fibonacci fan is also in view if there’s a fairly deep retracement.

While some of the general releases affecting the dollar this week (see above) could also drive movement for US500, the earnings reports of large-cap constituents are more likely to inform sentiment on the index. 78 companies report earnings this week, but here’s a summary of the most relevant:

Tuesday 9 February

Pre-market: DuPont de Nemours, Inc – consensus EPS 92c, same quarter last year’s EPS 95c

After hours: Cisco Systems, Inc – consensus EPS 68c, same quarter last year’s EPS 71c

After hours: Twitter, Inc – consensus EPS 18c, same quarter last year’s EPS 15c

Wednesday 10 February

Pre-market: Coca-Cola Co – consensus EPS 41c, same quarter last year’s EPS 44c

Pre-market: General Motors Co – consensus EPS $1.62, same quarter last year’s EPS 5c

After hours: Uber Technologies, Inc – consensus EPS negative 53c, same quarter last year’s EPS negative 64c

Thursday 11 February

Pre-market: PepsiCo, Inc: consensus EPS $1.46, same quarter last year’s EPS $1.45

After hours: Walt Disney Co consensus EPS negative 47c, same quarter last year’s EPS $1.53

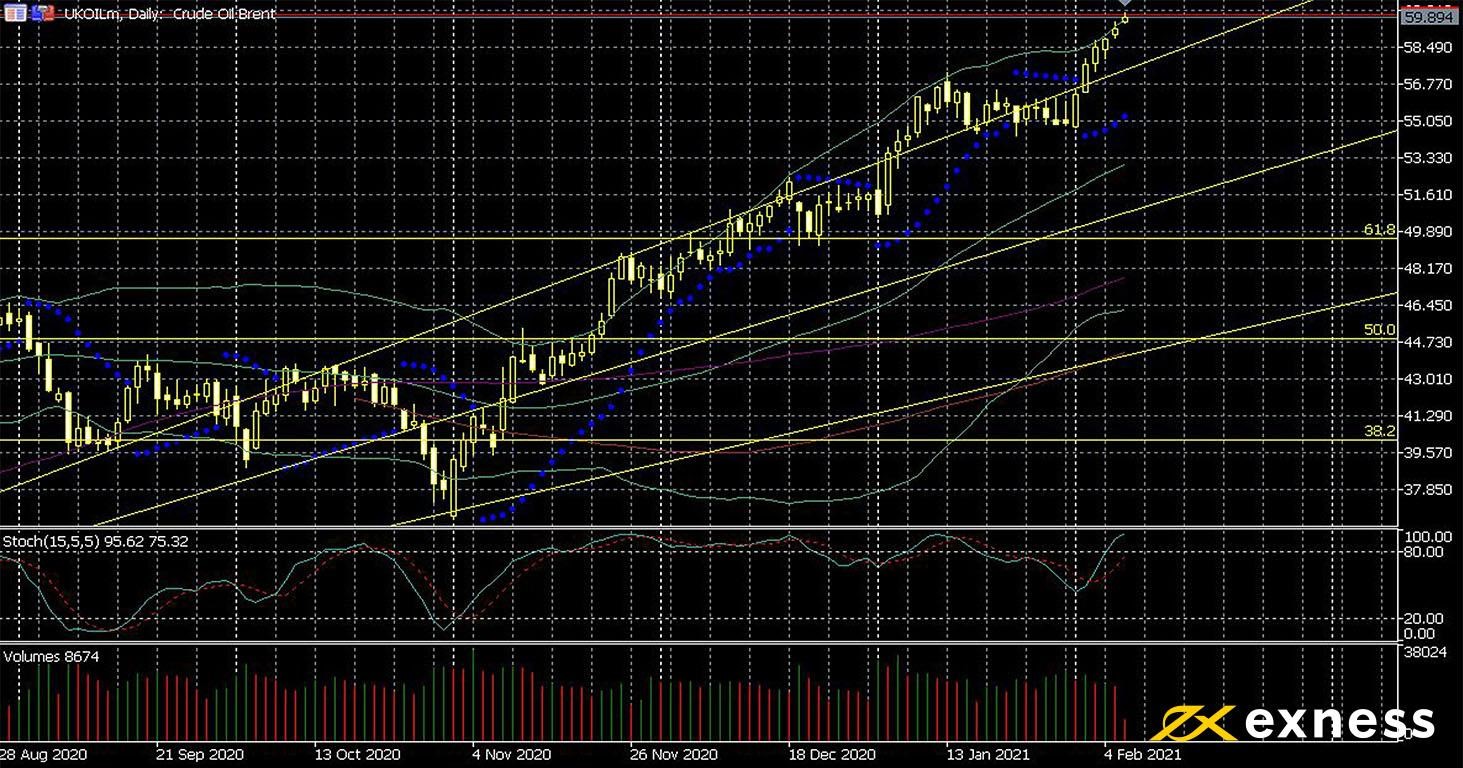

Brent, daily

Brent (UKOIL) hit an annual high above $60 this morning GMT with sentiment as elsewhere boosted by the prospect of new American stimulus but also recovering demand in many countries. Most important of these is China, where industrial activity has surpassed early 2020’s levels. American stocks of crude meanwhile have generally declined so far this year.

As above with US500, markets don’t usually go in one direction constantly for three months, so a correction might reasonably be expected here depending on this week’s regular stock data. Brent like American light oil has been clearly overbought based on the slow stochastic since November, although volume of buying here has remained consistently high.

Key data this week

Bold indicates the most important release for this symbol.

Tuesday 9 February

30 GMT: API crude oil stock change (5 February) – previous negative 4.26 million

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.