This article was submitted by Michael Stark, market analyst at Exness.

Stock markets around the world have generally started the week somewhat nervously after hawkishness from the Federal Open Market Committee at last Wednesday’s press conference. With the primary narrative of high inflation moving aside to some extent, commodities other than oil plus non-tech shares have generally retreated over the last few days of trading. This preview of weekly data looks at GBPZAR, USDMXN and UKOIL.

The Fed indicated last week its preparedness to act in the face of sharply rising inflation and generally strong economic recovery. Markets are now pricing in two rate hikes in the USA in 2023 plus possibly one towards the end of next year. Last week’s negligible hike of 0.05% in the funds rate, taking it to 0.15%, brought a large inflow of capital, with the New York Fed receiving a record $580 billion stored overnight last Wednesday.

This week’s key event in monetary policy is the meeting of the Bank of England on Thursday, the last before the departure of chief economist Andy Haldane, also known as ‘Mr Boom’. He is expected to be the sole dissenting voice against the consensus for holding the bank rate at 0.1%. The Banco de Mexico is also due to meet on Thursday evening GMT and likely to hold its benchmark rate as well at 4%.

The week ahead isn’t especially active in terms of regular economic data, but there are some regionally important releases including South African inflation on Wednesday. German and British sentiment and American income and spendings might generate some movement on charts. Oil meanwhile is likely to be in focus somewhat more this week given that, among commodities, it isn’t usually correlated very strongly with changing sentiment on inflation, so regular stock data from the USA might drive activity there.

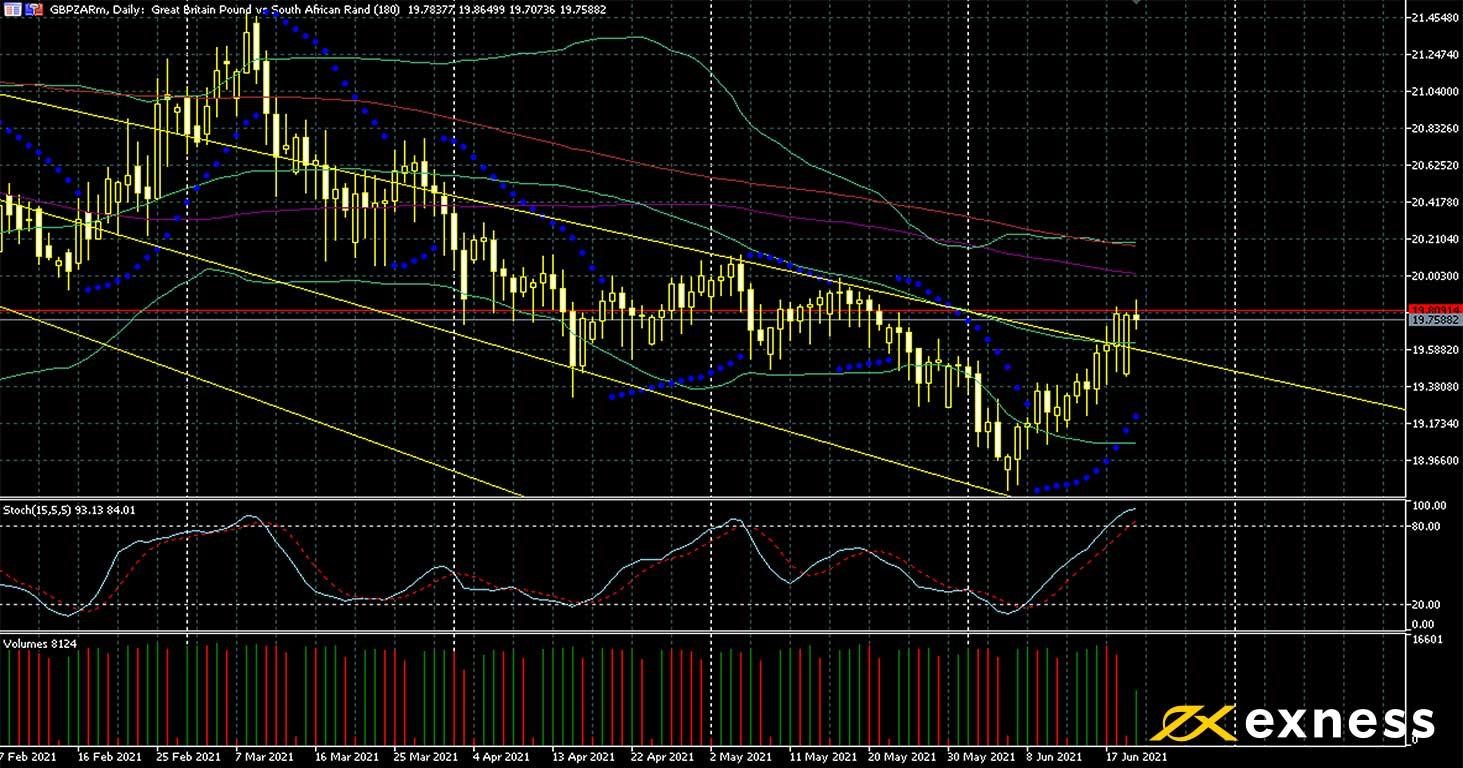

Pound-rand, daily

The pound has regained some strength against most emerging currencies including the rand in the aftermath of a very positive claimant count change last week. South Africa’s recovery is also stuttering somewhat amid extremely high unemployment combined with inflation starting to rise faster in line with major advanced economies. From a fundamental point of view, more weakness might be expected for ZAR if commodities lose their lustre as attention moves away from inflation itself and back to monetary policy.

Price seems to have broken through the 61.8% area of the weekly Fibonacci fan with two daily closes in succession above this area. Moving averages still give a sell signal, but the value area between the 100 and 200 SMAs has shrunk considerably. Movement above this area might signal more gains to come for the pound, but this depends on Wednesday’s data and participants’ reaction to the Bank of England’s statement and press conference on Thursday.

The dollar appreciated sharply against most currencies in the second half of last week after the Fed signalled faster and stronger tightening of monetary policy than had been expected earlier this year. The first rate hike, albeit minimal at 0.05%, also came last Wednesday, while markets are now awaiting more clarity on the timeframe and scope of scaling back bond buying over the next several quarters.

USDMXN’s bounce is technically significant because it has driven golden crosses by the 50 SMA from Bands over the 100 and 200 SMAs where previously all three had bunched quite closely together. However, the greenback is very strongly overbought here based on both the slow stochastic at about 88 and price clearly outside the upper deviation of Bollinger Bands.

Traders of this symbol are likely to focus on Mexican unemployment on Thursday morning GMT and the meeting of the BdeM that evening above other releases. However, Friday’s income and spending from the USA could also drive the dollar up if sentiment remains mostly positive.

Key data this week

Bold indicates the most important releases for this symbol.

30 GMT: American personal income (May) – consensus negative 2.5%, previous negative 13.1%

30 GMT: American personal spending (May) – consensus 0.3%, previous 0.5%

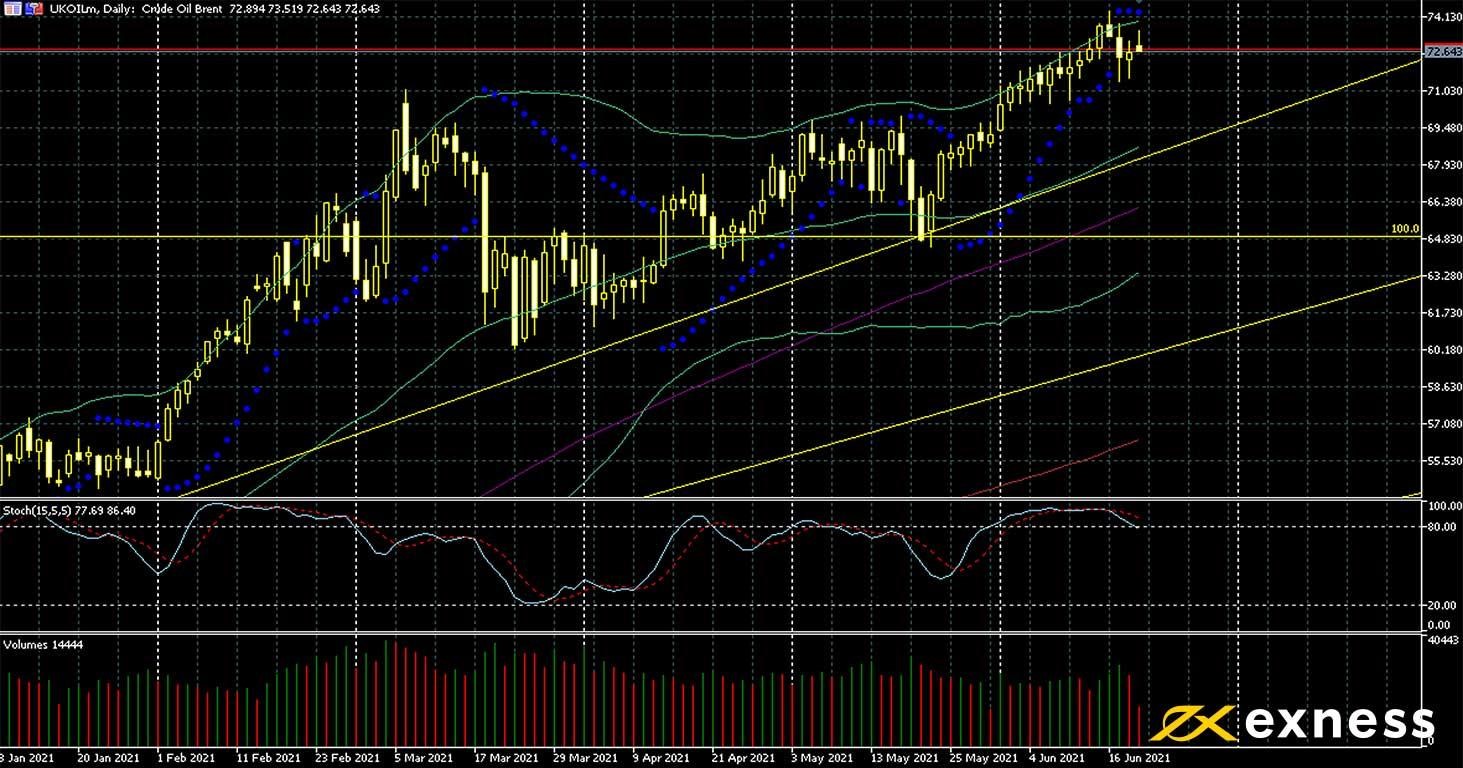

Brent, daily

Oil markets have generally discounted last week’s news from the Fed and focussed instead on positive factors. The main ones are the breakup of Iranian nuclear talks with no agreement and general optimism about demand. OPEC+ is also positive on the market’s fundamentals and still plans to decrease curbs in supply gradually next month.

Technicals are also strongly positive for Brent, with moving averages giving a strong buy signal and volume relatively high compared to the first quarter of 2021. Price has also recently moved slightly outside the overbought zone of the slow stochastic. The usual American stock figures and rig count are the main releases in view for traders of oil this week.

Key data this week

Bold indicates the most important release for this symbol.

Tuesday 22 June

30 GMT: API crude oil stock change (18 June) – previous negative 8.54 million

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.