This article was submitted by Michael Stark, market analyst at Exness.

Relatively disappointing Chinese data early this morning has put most European and Asian stock markets on the back foot so far today. Gold has continued its recovery while oil has slumped further, erasing last week’s gains. This preview of weekly data looks at NZDUSD and GBPJPY ahead of the RBNZ’s meeting and the FOMC’s minutes on Tuesday and Wednesday.

The only significant change in monetary policy last week was the Banco de Mexico’s hike of 0.25% to 4.5% as expected. The middle of this week is quite active in this area, with the Reserve Bank of New Zealand widely expected to hike to 0.5% early on Wednesday morning GMT and the Federal Open Market Committee’s minutes due that evening. Of lower importance is the Norges Bank’s meeting on Thursday from 8.00 GMT, with a hold at zero likely.

This week’s most important releases include claimant count change from the UK on Tuesday morning plus British, Canadian and Japanese inflation. American retail sales, South African inflation and Japanese balance of trade might also affect the relevant currencies in the next few days. Traders of oil are likely to monitor weekly stocks from the USA more closely than usual given the commodity’s quite strong movements over the last few weeks.

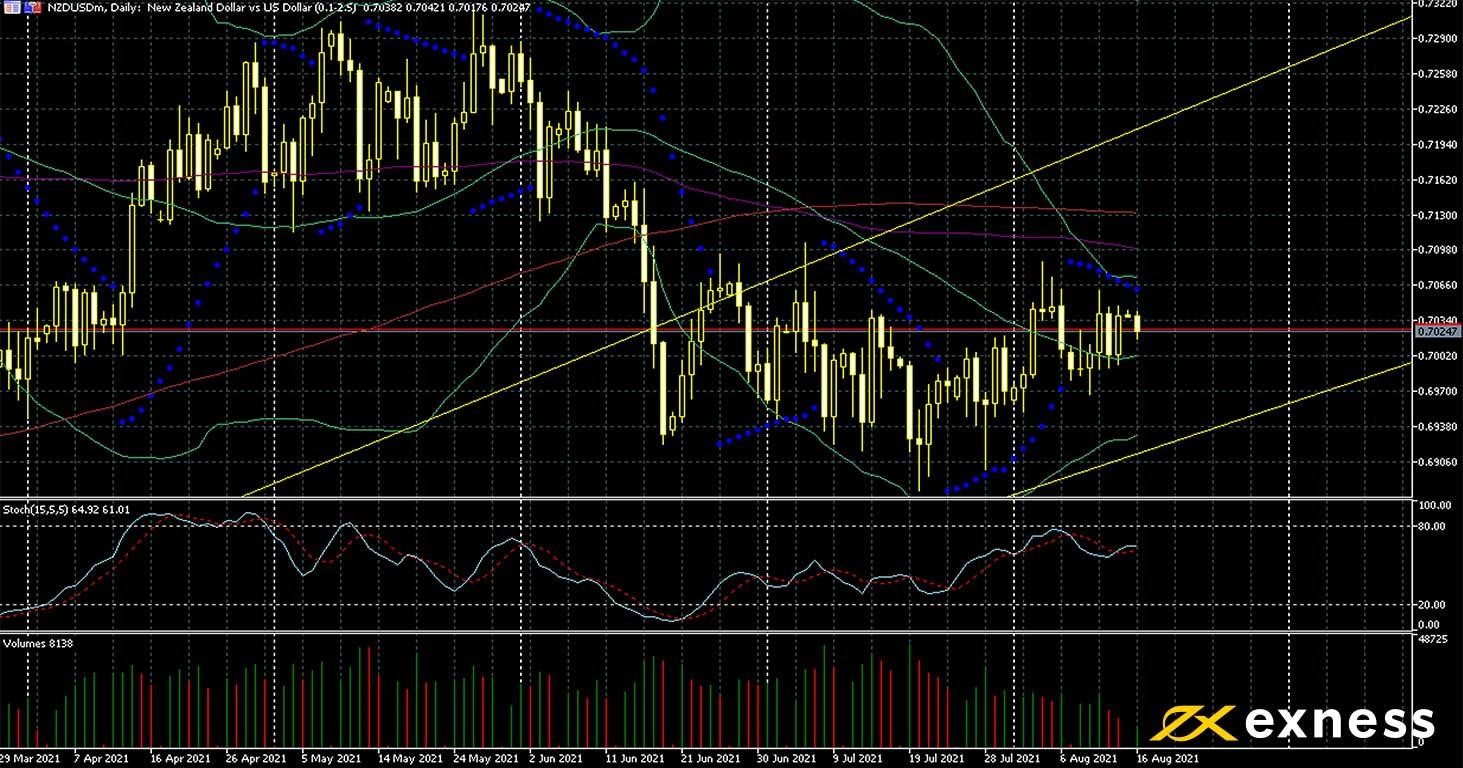

New Zealand dollar-US dollar, daily

NZDUSD hasn’t been particularly active so far this summer, with the price around 70c near where it was during the penultimate day of the large decline in mid June. Lower prices for various commodities have hit the Kiwi dollar, although in terms of monetary policy both the Fed and the RBNZ seem to be among the least dovish major central banks. Strong Kiwi job data in the second quarter have helped to prevent further losses for this symbol.

The obvious near-term resistance here is the value area between the 100 and 200 SMAs. Whether this might be tested on Wednesday morning is likely to depend on how markets perceive the accompanying commentary from Dr Orr and other senior members of the RBNZ, not just whether the cash rate is hiked as expected. Lower volume since the end of last month is typical for the time of year but also common in the runup to possible significant changes in monetary policy.

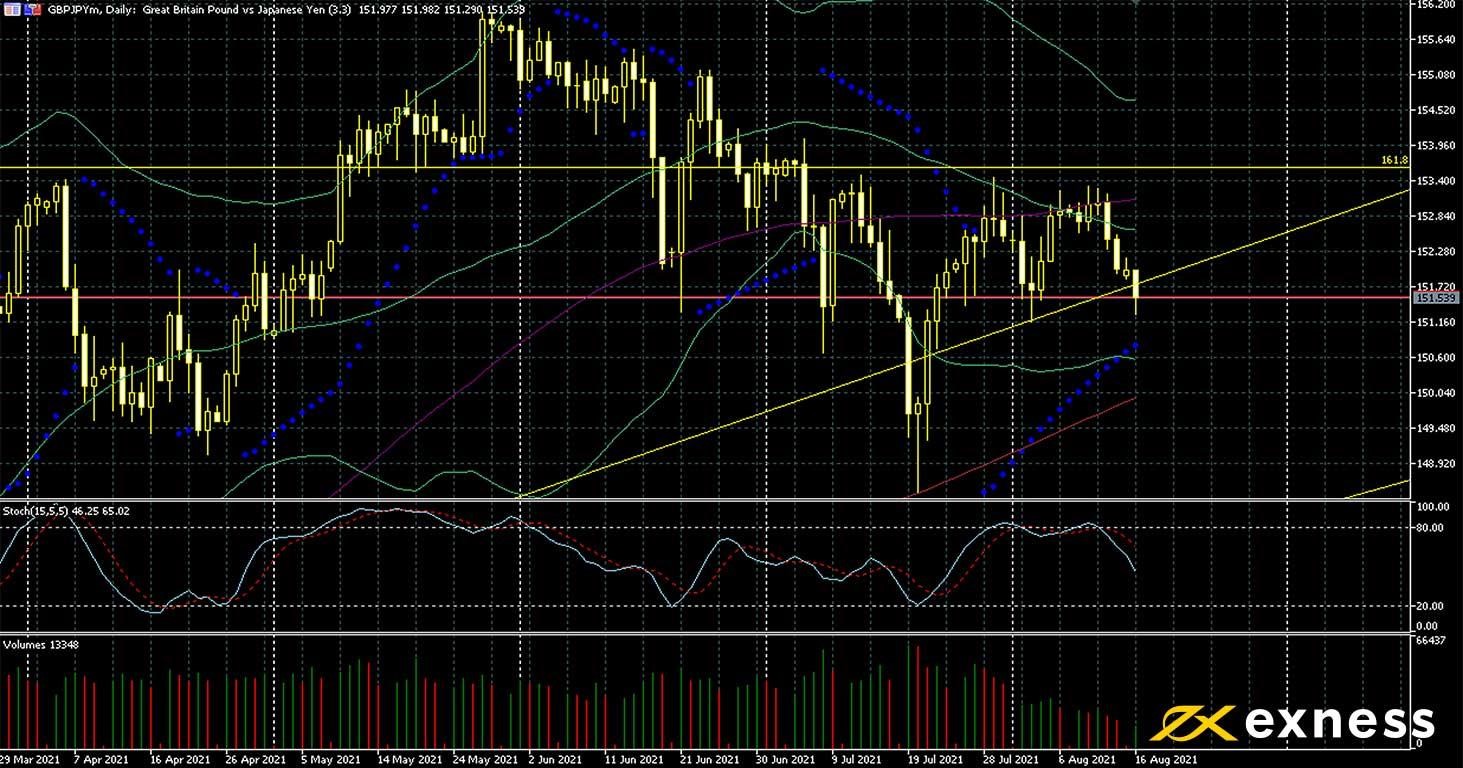

General caution in markets after high American inflation and the ongoing spread of Delta have dented sentiment on the pound to a degree against the haven yen and some other currencies. Conversely, higher forecasts for British inflation and the BoE’s expectation that ‘some modest tightening’ of policy would be required by next year if economic growth continues are positive factors for sterling.

As above for NZDUSD, volume has been much lower here so far this month, a normal situation in the middle of summer. The 200 SMA around the key psychological area of ¥149.95-150 seems to be a candidate for support in the near future, while the 161.8% weekly Fibonacci extension area slightly above ¥153.55 could cap a bounce. The key data likely to drive strong volatility for GBPJPY this week are British inflation (core and non-core) on Wednesday morning, but tomorrow’s claimant count change and Japanese balance of trade are also important.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.