This article was submitted by Michael Stark, market analyst at Exness.

Stock markets in Europe generally started the week somewhat positively as financial shares made ongoing gains in the aftermath of the ECB’s two-step hike last Thursday. This week markets are concentrating on American monetary policy and data given the threat of recession in the USA. This preview of weekly data looks at EURUSD and XAUUSD ahead of the Fed’s meeting and American advance GDP.

The European Central Bank was the main event in monetary policy last week, raising each of its three main rates by half a percent with further hawkishness likely over the next few months depending on data. The South African Reserve Bank also hiked its rate 0.75% last week. This Wednesday evening the Fed will meet: the statement is expected to be very hawkish, with a 100% chance of at least a three-step hike, i.e. to 2.25-2.5%. At noon GMT on Monday the likelihood of a four-step hike, a full percent, was around 22.5%.

However, the Fed’s meeting will not overshadow the other critical release this week, namely advance GDP data for the second quarter from the USA on Thursday. If this is negative, the traditional criterion for a recession will probably be met. Other important figures this week include German consumer confidence, Australian inflation and on Friday a range of preliminary inflation and GDP releases from the eurozone.

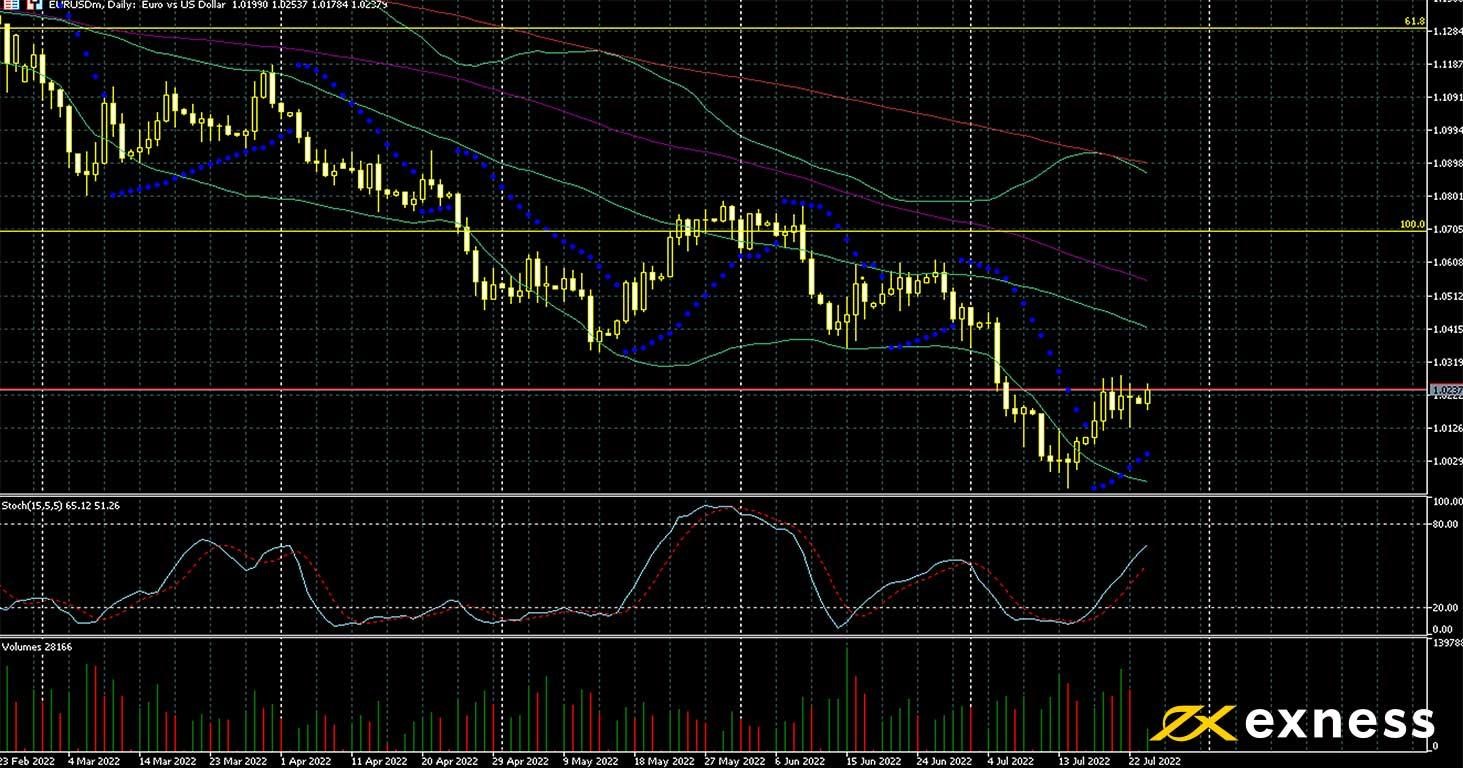

Euro-dollar, daily

The euro has bounced against the greenback since 15 July as concerns over energy problems driving a deep recession in the EU have subsided and the ECB finally delivered on a double hike to attempt to tackle surging inflation. Data affecting both currencies have been generally poor in recent weeks, with the eurozone’s GDP showing negligible growth and American business activity contracting last month for the first time in nearly two years.

The main downtrend is still active with the price below all of the 50, 100 and 200 SMAs, but there is no longer any sign of oversold from either the slow stochastic or Bollinger Bands; the former at around 65 is between neutral and overbought. The next movement for EURUSD depends on the reaction to Wednesday and Thursday’s news. While this might seem like a decent opportunity to sell in, traders can probably expect strong reactions on this chart to both the Fed’s meeting and advance GDP, so caution is advised if holding positions around these times.

12:30 GMT: American personal spending (June) – consensus 0.9%, previous 0.2%

12:30 GMT: American personal income (June) – consensus 0.5%, previous 0.5%

Gold, daily

Gold has bounced slightly since 21 July to trade at around $1,725 as fears of recession increased further in recent days and yields from benchmark decade Treasury bonds declined significantly below 3%. Overall, though, the fundamental picture for gold is quite negative, with the dollar in high demand and of course the Fed’s aggressive moves to hike rates last quarter which are expected to continue this week.

Similarly to euro-dollar, gold-dollar has now moved out of oversold while the main downtrend is still active. Volume here though is significantly lower than the peak in March during the initial stages of Russia’s latest invasion of Ukraine, so participants seem to be biding their time and waiting for this week’s result before committing themselves. The near-term support around $1,680 will almost certainly be tested at some point this week; if the downtrend continues the next main target might be the 200 SMA around $1,655. To the upside, the 50% weekly Fibonacci retracement is likely to cap gains unless data this week deliver a big surprise.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.