This article was submitted by Michael Stark, market analyst at Exness.

Asian and European shares have started the week somewhat negatively on the whole as Chinese data on Monday morning missed expectations. The focus on high inflation around the world is likely to continue over the next few days although few major economic releases are expected. This preview of weekly data looks at USDZAR and CADJPY.

The meeting of the European Central Bank last week was somewhat negative for the euro. The ECB reiterated its commitment not to start raising the deposit facility rate until quantitative easing has been wound down, which is expected early next quarter. The Bank of Canada though was much more hawkish, calling for a two-step hike and announcing the end of reinvestment from maturing assets.

The main central bank meeting next week is the Bank of Japan, but traders are concentrating on the Federal Open Market Committee on 4 May. As of 18 April, a very large majority of traders – around 90% – expect a two-step hike of the funds rate according to CME FedWatch Tool.

While there’s no really critical regular data due this week, attention is on Canadian and Japanese inflation plus Japanese balance of trade and British retail sales. Regionally important releases include New Zealand and South African inflation. In this situation, the war, stock markets, sentiment on monetary policy, bond yields and possibly other political factors are likely to be more important drivers this week for many symbols than economic releases..

US dollar-rand, daily

The dollar index broke above 100 on 12 April for the first time in two years in response to a new 40-year high of 8.5% in annual non-core inflation, rising bond yields and a greater focus on cash in the last few weeks as stock markets have generally been lukewarm. A hike of the funds rate on 4 May to 0.75-1% seems to be nearly certain as of now. Apart from monetary policy, the focus of traders in the next few weeks will probably remain on economic data and whether inflation might have peaked or could continue to rise into the third quarter.

However, the rand has remained strong in the last few weeks as the South African Reserve Bank also appears to be in a cycle of tightening. On the whole, the outlook for South Africa’s economy seems to be stronger now than it was at the start of 2022: prices of important commodities, key to South Africa’s exports, have risen further with the war in Ukraine amplifying Covid’s effects on supply chains. The main risk is local inflation, particularly of food and fuel.

On the chart, it seems unlikely that the recent downtrend might continue immediately. ATR has reached a 2022 low of less than 15 rand cents and momentum has declined since late March. Volume has also been much lower since the end of last week. This week’s data, notably South African inflation, are unlikely to have an ongoing effect on the price but might drive a bounce to the area of the 50 SMA or a relatively small loss to the latest low around R14.40.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 19 April

12:30 GMT: American annual housing starts (March) – consensus 1.75 million, previous 1.77 million

12:30 GMT: American annual building permits (March) – consensus 1.83 million, previous 1.87 million

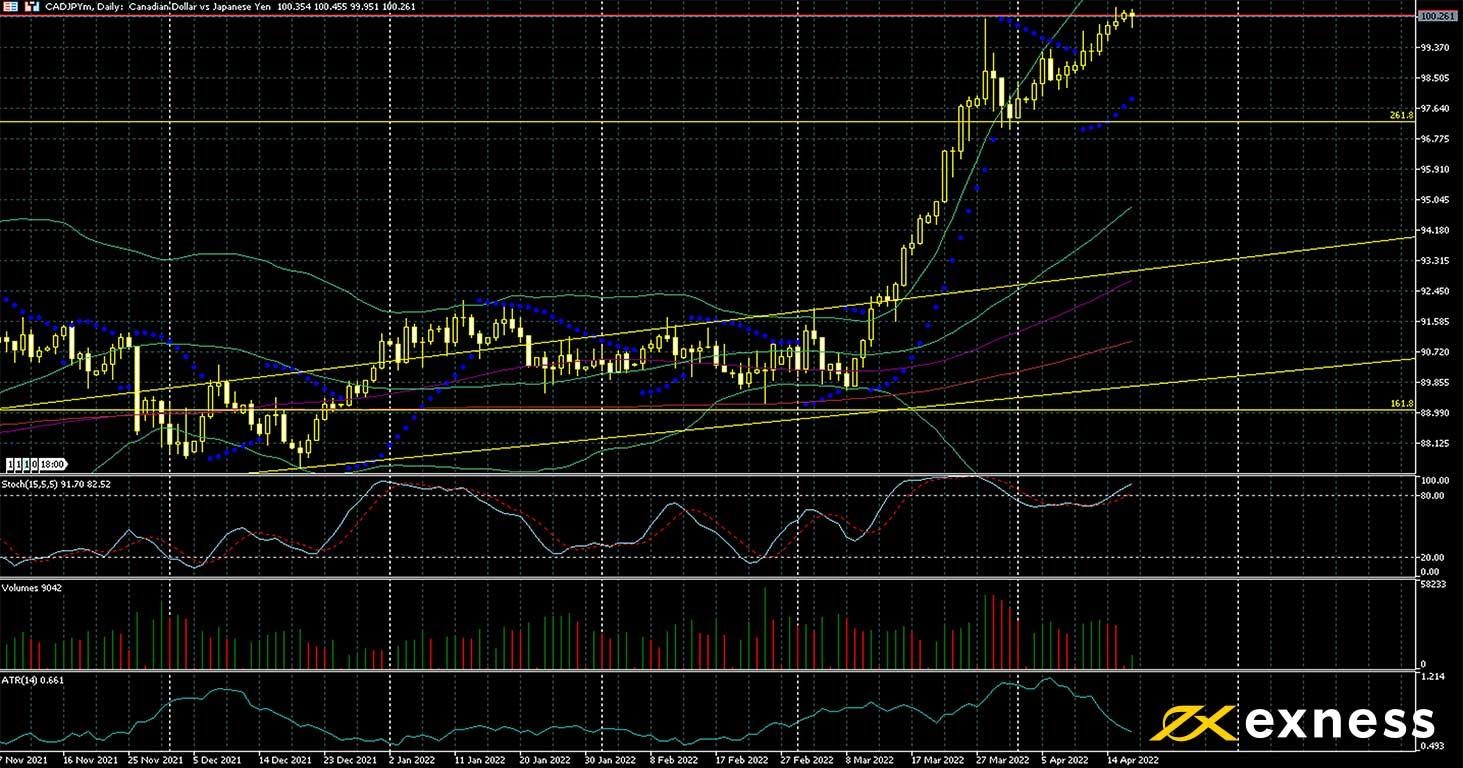

As for the greenback and various other major currencies, the Canadian dollar has made strong gains against the yen since last month as the divergence of monetary policy becomes increasingly clear. Last week’s hike of the target overnight rate in Canada was the first half percent hike in more than 20 years, demonstrating the Bank of Canada’s commitment to tackling inflation. With oil remaining above $100 quite consistently in April so far, the loonie has also had support from the prices of exports. Meanwhile the yen has reached a low of around seven years in this pair as the Bank of Japan remains committed to ultra-easy policy amid stubbornly low inflation: excluding food and energy, annual deflation in Japan is around 1%.

¥100 exactly is a critical psychological area which the price has yet to clear fully. Entering here as a new buyer would traditionally be regarded as unacceptably risky, so some traders might prefer to wait for a retracement, possibly to the 261.8% weekly Fibonacci extension around ¥97.25, before buying in. A declining ATR and very strong overbought conditions might support this approach. Beyond ¥100, there is no clear resistance until November 2014’s closing highs around ¥105.

CADJPY is the major forex pair with the most important economic releases this week. Traders can reasonably expect significantly higher volatility over the next few days.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 19 April

23:50 GMT: Japanese balance of trade (March) – consensus negative ¥100.8 billion, previous negative ¥668.3 billion

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.