This article was submitted by Michael Stark, market analyst at Exness.

Inflation in the USA and UK reached fresh highs of 40 and 30 years respectively at 8.5% and 7% last month. Stock markets have generally reacted slightly negatively to the news while gold has made gains so far this week. This midweek preview of upcoming data looks at EURUSD and XAUUSD ahead of the ECB’s meeting later today.

The Reserve Bank of New Zealand unexpectedly announced a two-step hike yesterday at its meeting, its fourth successive hike. However, the Kiwi dollar has declined in the aftermath. The Bank of Canada also decided on a hike of half a percent yesterday afternoon. The main event remaining in monetary policy this week is today’s meeting of the European Central Bank. While no change in policy is expected, traders are looking for some indication of tightening to start in June given March’s record high inflation in the eurozone.

American retail sales and industrial data are among the main regular releases this week. In general, reasonably good job data from most countries and very high and rising inflation suggest that participants in forex and other markets might start to price in even more aggressive monetary tightening over the next few weeks.

Earnings season has also started in earnest, with major financial companies reporting results for Q1 this week, followed by big tech next week. The Western Christian calendar observes Good Friday this week, so activity in markets is likely to be significantly lower tomorrow.

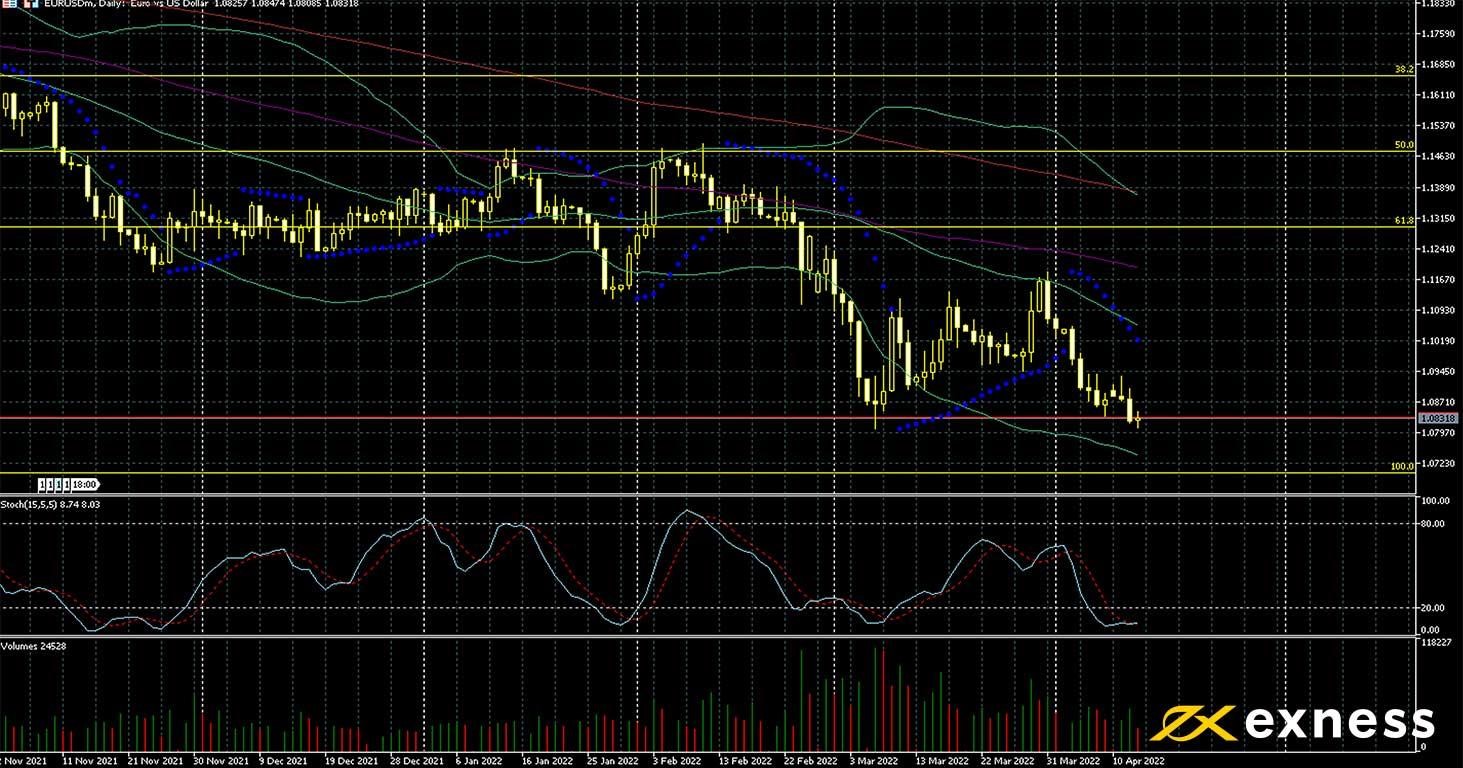

Euro-dollar, daily

Sentiment on the euro has been somewhat more negative this week as the first stage of the French presidential election resulted in a relatively small gap between the incumbent Emmanuel Macron and the eurosceptic Marine le Pen. Markets also remain concerned about the possible impact on economic growth caused directly and indirectly by the ongoing war in Ukraine. The ECB is still among the most dovish major central banks despite record high inflation around 7.5% and increasing calls from members of the EU to try to control rising prices.

The technical picture remains unambiguously negative, with a fresh two-year closing low of $1.0825 on Tuesday. The next key support is the psychological area of $1.07 near the 100% Fibonacci retracement, i.e. full retracement of all the euro’s gains since March 2020. To the upside, any possible bounce in the next few weeks would probably face resistance around $1.10 and above that the 50 SMA. Volatility is likely to be higher in the early afternoon GMT as is typical around a meeting of the ECB.

13:15 GMT: American annual industrial production (March) – consensus 5.9%, previous 7.5%

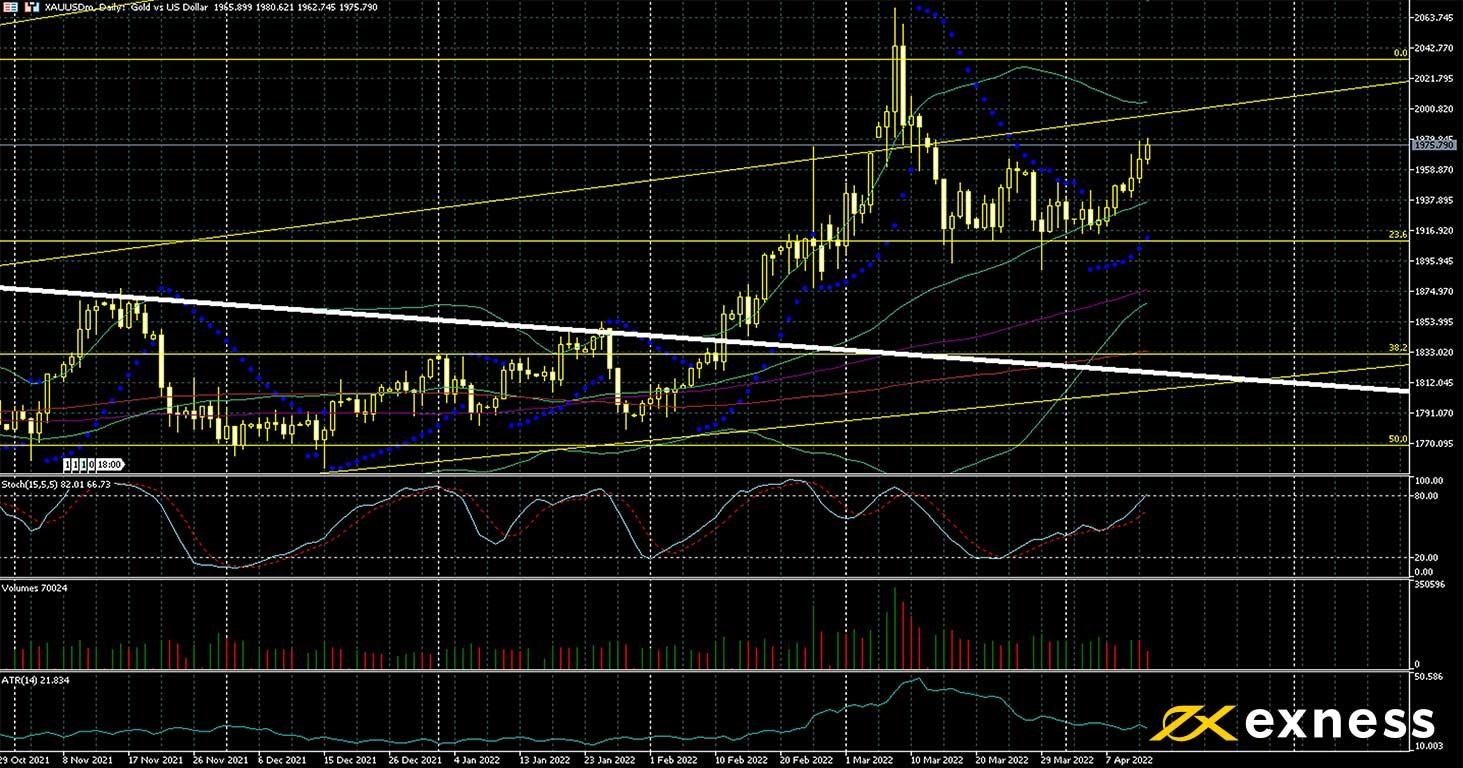

Gold, daily

Gold reached a monthly high yesterday around $1,980 in the aftermath of higher than expected American inflation and a general lack of optimism surrounding talks between Russia and Ukraine. On the contrary, it appears that Russia is preparing a new offensive in the east of Ukraine. A large majority of participants, more than 85%, expects a two-step hike by the Fed on 4 May. Yields of 10-year Treasuries meanwhile reached a fresh post-Covid high above 2.63% on Tuesday.

The chart seems to suggest more gains to come, with the price having moved upward from the range that was established in the second half of last month. However, with buying volume still quite low and buying saturation approaching, an immediate strong breakout upward is unfavourable based on TA. American data this afternoon and tomorrow might drive some movement, but sentiment, the war and events in stock markets seem more important in the near future.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.