This article was submitted by Michael Stark, market analyst at Exness.

Indices generally gained ground on Tuesday as attention shifted away from tension between Russia and Ukraine, at least temporarily. Gold meanwhile posted a large intraday decline but recovered somewhat early on Tuesday evening GMT. This midweek preview of data looks ahead at the releases that might affect XAUUSD and GBPUSD over the next few days.

The central banks of Mexico and Russia raised their base rates last week, although the latter has had little clear effect so far in shoring up sentiment on the ruble. The likelihood of a two-step rate hike by the Fed next month has increased to around 60%, although markets don’t seem to be seriously considering recent wild rumours of an emergency hike. Wednesday evening’s minutes from the Federal Open Market Committee’s latest meeting are the main event in monetary policy this week and might give clues on what’s likely at the next meeting.

British inflation on Wednesday morning is the most important regular release this week, with the consensus of 5.4% for annual non-core the same as last month’s figure; the Bank of England expects inflation to peak around 7% next month or in April. Canada is also due to release statistics on inflation on Wednesday, then on Thursday morning GMT Australian job data rounds off the most important events of the week from the economic calendar.

Gold-dollar, daily

Gold has been somewhat sensitive to Russian sabre-rattling against Ukraine, but with an apparent de-escalation on Tuesday morning GMT, the metal made a significant loss by around lunchtime of the European session that day. In general, though, inflation and the Fed’s possible response to it remain the main drivers behind the price of gold this week.

From a technical point of view, the recent breakout above the medium-term downward trendline has yet to be confirmed although it seems strong. Somewhat higher volume of buying over the last few sessions, rising ATR and price clearly above all three of the simple moving averages seem to point to possible continuation. Traders in this situation might do well to remember that the line of the downtrend is an area rather than a dynamic level even if the news on Wednesday night supports more gains.

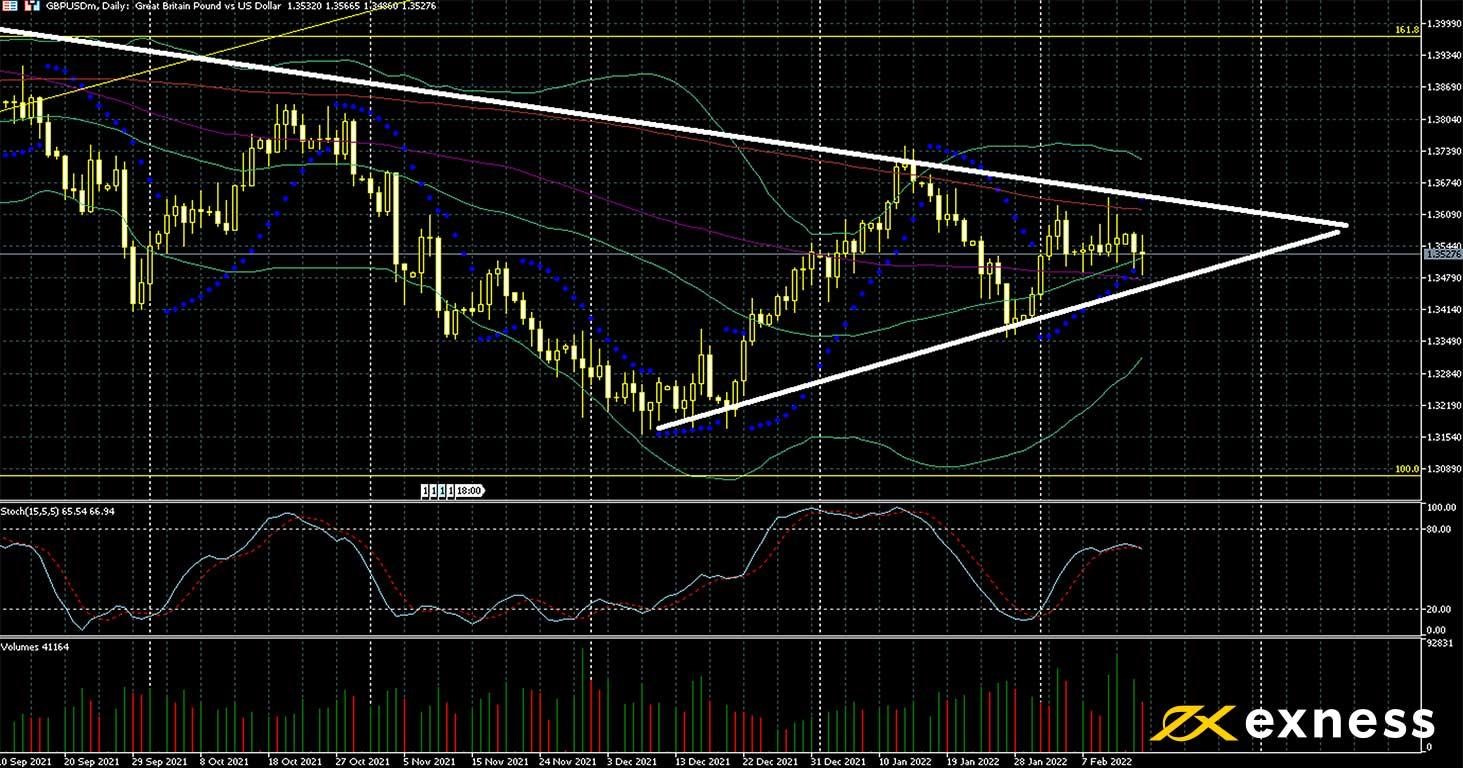

Tuesday morning’s claimant count change showed that nearly 4,000 more people than expected stopped claiming benefits for unemployment in the UK last month. This has strengthened expectations that the Bank of England will continue its recent hawkish policy. Annual growth in average pay also edged up to 4.3%. As noted above, the Fed is also hawkish, with some senior members calling for a total hike of 1% by July. Neither currency seems to have clearly stronger fundamentals or sentiment.

The triangle forming on the daily chart would project a narrowing range followed by a possible breakout around the middle of March; this would coincide with the Fed’s next meeting. The recent golden cross of the 50 SMA from Bands above the 100 might suggest an upward breakout next month and price near the top of the pattern until then, but this of course depends on expectations for monetary policy. The key release this week is British inflation on Wednesday morning, which might influence the BoE’s decision on 17 March.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.