This article was submitted by Antreas Themistokleous, market analyst at Exness.

Activity in markets has generally been low so far this week as participants look ahead to key meetings of central banks and Friday’s job report from the USA. All three of the Fed, Bank of England and European Central Bank will release statements with expected rate hikes before the end of the week. This midweek preview of data looks at EURUSD and GBPJPY.

Last week the Bank of Canada hiked its target overnight rate one step to 4.5% as expected. The reaction on charts was mostly muted given that the result had been priced in, but USDCAD has been more volatile so far this week.

The Fed seems to be nearly guaranteed to call for a single hike to 4.5-4.75% this evening, so the main event is the subsequent press conference. The focus of traders there is on Jerome Powell’s comments on inflation and economic conditions. The BoE and ECB are both likely to call for double hikes tomorrow afternoon, an outcome which is also widely predicted, so attention will likely focus on the press conferences in much the same way as the Fed.

Friday’s job report from the USA is another critical release this week, with the consensus of a drop to 185,000 for the NFP itself and unemployment rising slightly to 3.6%. If broadly accurate, this could confirm sentiment that the Fed will continue to be less hawkish because such figures would suggest a clear cooling off in the job market in the USA even though that might be only temporary.

Traders are also going to monitor flash inflation from the eurozone this morning, ISM manufacturing PMI later today, German balance of trade tomorrow and ISM non-manufacturing PMI on Friday. This is a particularly active week on the economic calendar so most traders would traditionally monitor positions more closely than usual and take extra care to avoid overexposure.

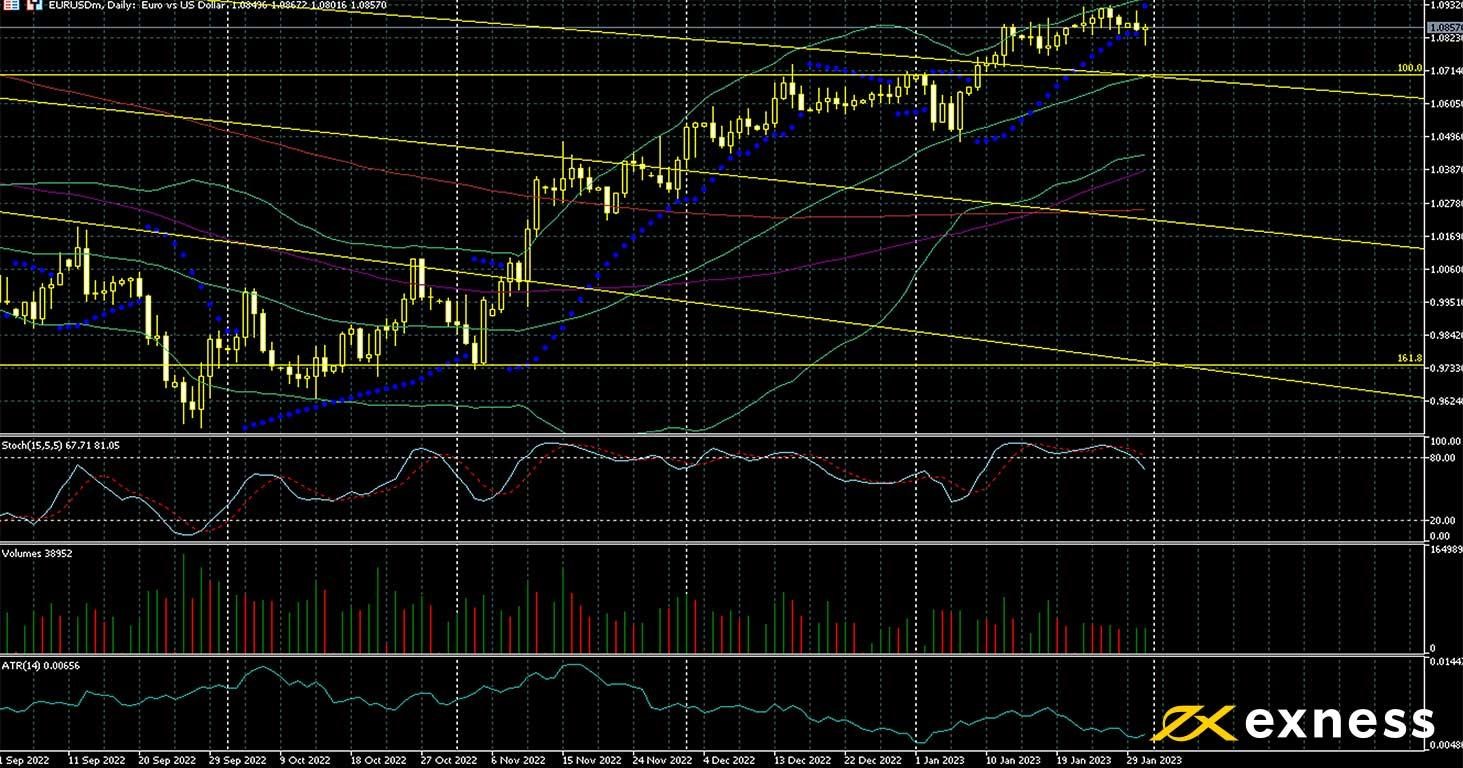

Euro-dollar, daily

Economic data from the eurozone have mostly been more neutral than negative this month despite the occasional blip from Germany. That’s one of the main sources for somewhat more positive sentiment on the euro compared to early in the fourth quarter of last year combined with expectations that the ECB will continue to hike its rates strongly into the summer.

There’s now a fairly consistent trend of slower inflation in the USA while flash inflation data from some European countries this week showed continuing though small growth. The energy crisis in most of the eurozone isn’t having quite as catastrophic effects as some had predicted last summer because the prices of oil and gas have decreased significantly from peaks last year and because this winter so far has been mostly mild or average in Europe.

The chart itself definitely suggests that the euro has reached a plateau and might decline in the near future. Momentum to the upside has been low since the middle of January and the price has hovered in overbought for weeks while volume and ATR have both dropped significantly.

Based on TA alone, one might expect a retreat to the confluence of the 50 SMA and the 100% monthly Fibonacci retracement around $1.07 before a resumption of the upward movement to test $1.10. However, unexpected hawkishness from the Fed or dovishness from the ECB would drastically change this impression, so it’s critical to monitor the press conferences and Friday’s NFP.

Key data this week

Bold indicates the most important releases for this symbol.

Like various other major pairs, pound-yen has been mostly flat since last week as traders await important news coming in the next couple of days. Sentiment on the pound has generally worsened so far this year as indicators point to a recession in the UK this year more clearly than in most other advanced economies while ongoing strikes and generally weak demand are also negative factors.

The Bank of Japan’s interventions to stabilise the yen since late last yesterday have been successful on the whole so far. However, the BoJ is still looking for inflation above target in a sustained way before it seriously considers tightening policy.

The medium-term downtrend on the chart is becoming somewhat established even though momentum has been weaker recently. The 50 SMA clearly death crossed the 100 and 200 SMAs in January but the 161.8% weekly Fibonacci retracement has held. Now though the pound’s bounce seems to have petered out in overbought close to dynamic resistance, so there could be further losses and possibly another test of the 161.8% Fibo.

That would depend on how participants perceive the Bank of England’s comments tomorrow. Expectations for the BoE’s final rate of this cycle and its timing are quite divergent at the moment, but Dr Bailey has tended to err on the side of pessimism in most of his comments since he took charge, so allowing the dust to settle first might be wise if a trader wants to find a significant position this week.

Key data this week

Bold indicates the most important release for this symbol.

Thursday 2 February

from noon GMT: statement and press conference of the Bank of England

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.