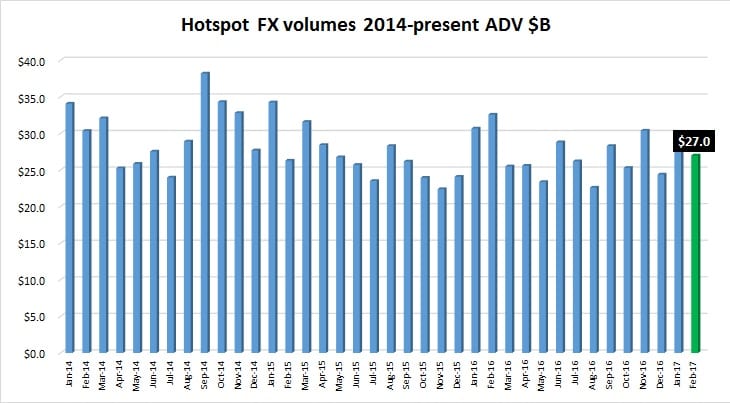

As its new owner CBOE Holdings Inc. (NASDAQ:CBOE) unveiled the new company logo (above), institutional Forex ECN Hotspot FX reported that February trading volumes cooled somewhat from the company’s hot start to 2017.

February volumes at Hotspot FX averaged $27.0 billion daily, down 8.8% MoM from January’s $29.6 billion ADV. Hotspot’s February figures begin a parade of what we believe will be volumes in the FX sector down from January, which was a very strong month at many of the leading retail and institutional eFX venues.

As noted above, as of March 1 Hotspot FX has a new owner, CBOE. CBOE completed yesterday its $3.2 billion takeover of Bats Global Markets Inc (BATS:BATS). The company wasted no time in rebranding its Forex ECN unit as: Hotspot – a CBOE company.

As time ran out on BATS as an independent company, BATS CEO Chris Concannon sent out his final CEO’s newsletter, which read as follows:

Dear Bats Customers, Issuers and Supporters,

Bats Global Markets, Inc. is expected to close its transaction with CBOE Holdings, Inc. tomorrow and, as a result, this is the last official Bats CEO Newsletter. So, let me start with a simple thank you. Thank you for your support. Thank you for your business. And thank you for your loyalty to this little company from Kansas City since 2005.

Bats employees have created an amazing history the past 12 years, making it difficult to sum up the company’s successes in a sentence or two. I could focus on our leadership positions as the #1 stock market in Europe and #2 stock market in the U.S. Or our ability to operate 11 markets globally with only 300 employees, or our successful moves into the U.S. Options, ETF listings and Global FX markets. And, of course, the many market-structure changes that Bats has advocated for or introduced — all for the benefit of the markets and investors.

Instead I will leave it to John Lothian, the longtime market participant, observer and curator of industry news, who put it simply — and best — on January 2, 2014, when he wrote a single, brief sentence in his daily newsletter:

“Bats has changed the game.”

Yes, Bats has changed the game. That statement, as much as any, encapsulates what this company and its employees have accomplished in the firm’s brief but unprecedented history, whether creating a more competitive dynamic or paving the way for a market structure that benefits all investors and market participants.

Founded in 2005 by Dave Cummings and 12 associates, including eventual CEO and current Chairman Joe Ratterman, BATS Trading began as an electronic communications network (ECN) in a North Kansas City storefront, surrounded by a bakery, a barber shop, a florist and a drug store. The firm, largely comprised of innovative software engineers tasked with building the industry-leading Bats technology, was immediately a leading advocate for competition, working closely with customers and other industry participants.

The company was aggressive from the beginning, both with its pricing and its unique marketing campaign, led by frequent CEO emails (or “newsletters”) to the industry, advocating for changes to the status quo and creatively critiquing the competition. I should know — as a competitor at Nasdaq at the time, the Bats CEO newsletters made me laugh with references like “Bob the Bully” and cringe when I was challenged to a public debate. Once, I even referred to these brilliant marketing ploys (since adopted by some politicians) as “Hugo Chavez emails.”

In the past 12 years, the tone of the Bats CEO newsletters has certainly changed — first from Joe and then hopefully from me — but the message hasn’t wavered since the company was founded: to be aggressive, to be thought provoking, to find inefficiencies in the market and root them out for the benefit of the markets and all investors.

Over the past decade or so, this Kansas City upstart — comprised of nearly 300 hard-working people — has morphed well beyond what one could have imagined, creating a company valued at more than $3 billion. Bats has become one of the world’s leading exchange operators, conducting business and applying competitive pressure across three continents. No longer just a KC company, we now have employees based in New York, London, Chicago, San Francisco, Singapore and Quito.

Bats’ many successes would not have been possible without the hard work and dedication of all our associates and the vision of my predecessor, Joe, with his ability to select and support an unbelievably talented team. Under his leadership from 2007-2015, the company completed the transformative Chi-X Europe (2011) and Direct Edge (2014) transactions, moved into U.S. Options and Global FX and, just as importantly, further optimized the highly efficient, team-oriented Bats culture.

Of course, the pending combination with CBOE doesn’t spell the end of the journey for Bats but is instead a major milestone in our mission to Make Markets Better by leveraging great technology and a unique spirit of innovation. As we prepare to become part of CBOE, working alongside CEO Ed Tilly and his great team, we are excited for the future of Bats and the opportunity to make an even bigger impact on global markets.

As a customer, issuer, supporter, vendor or competitor, you can expect to see Bats’ same vibrant competitive forces — and many familiar faces — as we join with CBOE. More than anything, we look forward to continuing our work alongside you as our partner as we move into this next phase of Bats history.

Thank you, again, for your enduring support.

Sincerely,

Chris Concannon

CEO

Bats Global Markets

P.S. Because this is the final Bats CEO newsletter, it would be a shame to not make some market-structure predictions. Here are a few of my thoughts for the coming year:

Reg NMS – Will come under serious review in 2017;

IPOs – 2017 should be a banner year;

Tick Pilot – More data will simply reveal the same as the early data;

Mifid II – It won’t be delayed again but may see some last-minute adjustments;

FX Global Code – The difficulty will be the adherence; and

Volcker Rule – The market-maker exemption gets bigger.