If anyone was waiting for a bargain price for Bitcoin below $10,000, they had a brief chance to buy at $9,850 and above, as the world’s favorite digital asset plummeted over the weekend. During its momentous rise to stardom, the one characteristic that has stood out most over recent months is that, once again, volatility is in abundance over the weekend, whether BTC happens to be moving up or down. This time it was a fall, from roughly a perch of $11,450, then down to the lowlands of $9,850.

Bitcoin has since recovered gradually. At this writing, it rests at $10,800, with a positive recovery slope and signs that its bullish nature has not been depleted. The net loss has been trimmed to less than 6%, but altcoins had a rougher time of it, dropping by 10% or more in several cases. If you do the math, Bitcoin has recovered to the 61.8% Fibonacci benchmark, if measured from its original highpoint of $11,450 when the weekend began.

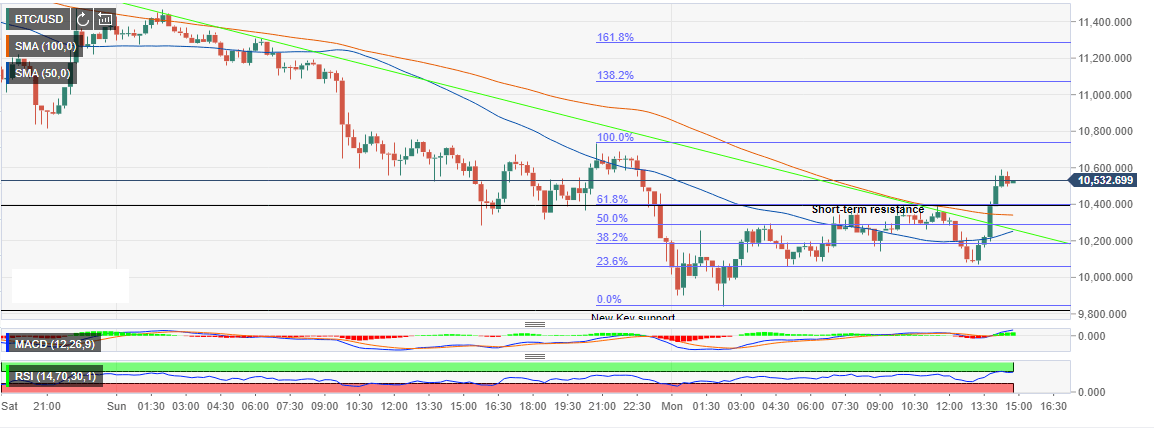

The above chart was constructed a few hours back. The Fibs apply only to its most recent display of support, mid-way through the above depiction. The Relative Strength Index (RSI) is signaling an overbought condition, while the Moving-Average Convergence Divergence (MACD) indicator is still bullish.

Analysts have a varied list of reasons for the wild action over the past few days. Profit taking was an obvious cause, but there were also signs that the bulls were tired, after several weeks of running hard. Google search volume on BTC was also down by 45% since June, an indicator that some analysts track religiously. And there was Trump’s tweet-fest, declaring that he was no fan of cryptos, especially Facebook’s Libra project. Lastly, a few negative comments had occurred during a recent hearing of the United States House of Representatives Financial Services Committee. The latest reporting is that a draft bill appeared in the committee entitled “Keep Big Tech out of Finance”.

The surprise over the past week, however, has to go to President Trump, our beloved Tweeter-in-Chief, who chose this time to dump on the notion of cryptocurrencies. He is already known for creating distractions to avoid accountability from another front, but his remarks were also typical for skeptics that had spoken out before him:

Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity… We have only one real currency in the USA, and it is stronger than ever, both dependable and reliable. It is by far the most dominant currency anywhere in the World, and it will always stay that way. It is called the United States Dollar!

John McAfee, 2020 U.S. Presidential hopeful and cyber security pioneer, chose to mock Donald Trump’s recent crypto tirade on Twitter. Speaking to the oft-cited issue of innovation and criminal activity, McAfee pointed out that the telephone was a boon for criminals, and the automobile increased bank robberies ten-fold, but no one suggested banning them. He concluded: “Please, Sir, get a clue.”

Cryptocurrencies are in the process of being adopted by the mainstream. For the more informed set of contributors to the national debate, the issue is simple and straightforward. More regulation will bring the necessary controls that will cull the criminal herd, so to speak. There is no need to ban cryptos in their entirety, an action that would allow the rest of the world to then benefit from its many innovative aspects.

Tom Lee, head of research at Fundstrat Global Advisors, was not that perturbed by anything that he was observing:

It’s healthy to see (Bitcoin) pullback here. As for the search traffic for bitcoin being low, I also think that is a good sign. It means the rise in bitcoin has not been accompanied by massive hype. The price action has obviously been very bearish having lost the key low I’ve been watching at 10900. Also we are right up against the megaphone trend line. A close below 10580 would mark a new daily low and therefore I’m expecting new lows if/when that occurs.

Amazingly enough, the chorus of “a 30%+ correction in BTC prices is long overdue” was nowhere to be seen or heard from during this wild weekend ride. Several well-respected analysts have been preaching this gospel for months to anyone that would listen, citing historical patterns, as evidence to support their claims. The odd thing is that Bitcoin almost hit $14,000 a few weeks back on some exchanges, and with this fall to $9,850, the correction in process actually measures out to be 30%, on the nose. Perhaps, we can finally move on and accept that the time for bargain prices has come and gone.