This article was submitted by Michael Stark, market analyst at Exness.

Shares in Europe have generally started the week positively after very strong eurozone-wide retail sales. The annual figure for August was up 3.7% against the consensus of around 2.2%. Meanwhile some risk-on instruments have made gains on reports that Donald Trump, who recently contracted covid-19, might soon be discharged from hospital. The dollar has generally remained weak so far today though in the aftermath of Friday’s disappointing NFP, the last before the presidential election.

There was no news from central banks last week, with most continuing record quantitative easing and trying to analyse the outlook for the final quarter of 2020. The main event in monetary policy this week is tomorrow morning’s meeting of the Reserve Bank of Australia, but the National Bank of Poland is also due to meet on Wednesday.

This week’s most important regular data is balance of trade, which comes from all of Australia, Canada, Germany, the UK and the USA. It’s a particularly big week for Canadian data, with job reports on Friday afternoon and Ivey PMI on Wednesday as well.

Political news has somewhat less potential to generate volatility this week but still should not be ignored. Ongoing Brexit talks and the reactions to these in markets are key, and while American markets are mostly focusing on the President’s illness, polling and rhetoric on the election could return to the fore over the next few days.

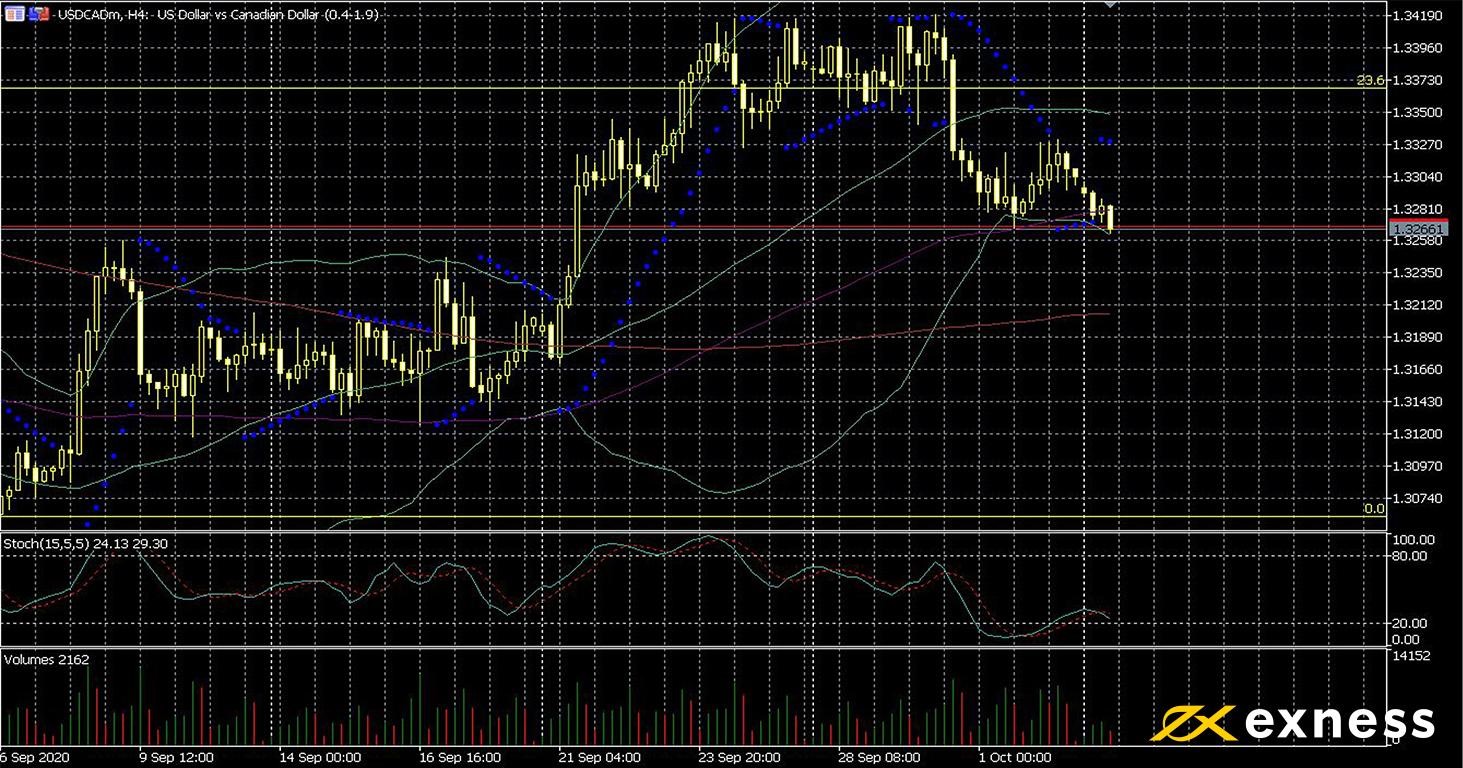

US dollar-Canadian dollar, four-hour

The greenback declined against the loonie last week despite oil’s losses. Wednesday’s quarterly American GDP at negative 31.4% wasn’t quite as bad as expected but still the largest quarterly contraction ever recorded of the USA’s economy. Inconsistent governmental response is one of the main reasons for the USA being the worst affected country from covid-19, especially when contrasted here with Canada’s comparatively timely and competent management of the situation.

The current test of the 100 SMA continues so far this week, and a lack of conviction is apparent among buyers given the series of long wicks at the end of last week. A retest of the 0% weekly Fibonacci retracement area, i.e. the starting point for the dollar in January, looks favourable sooner or later unless there’s a sudden change in the tone of fundamentals.

Apart from this week’s key trade data, USDCAD is of course inversely correlated with oil. Regular releases affecting the price of crude will probably bring movement here tomorrow and Wednesday.

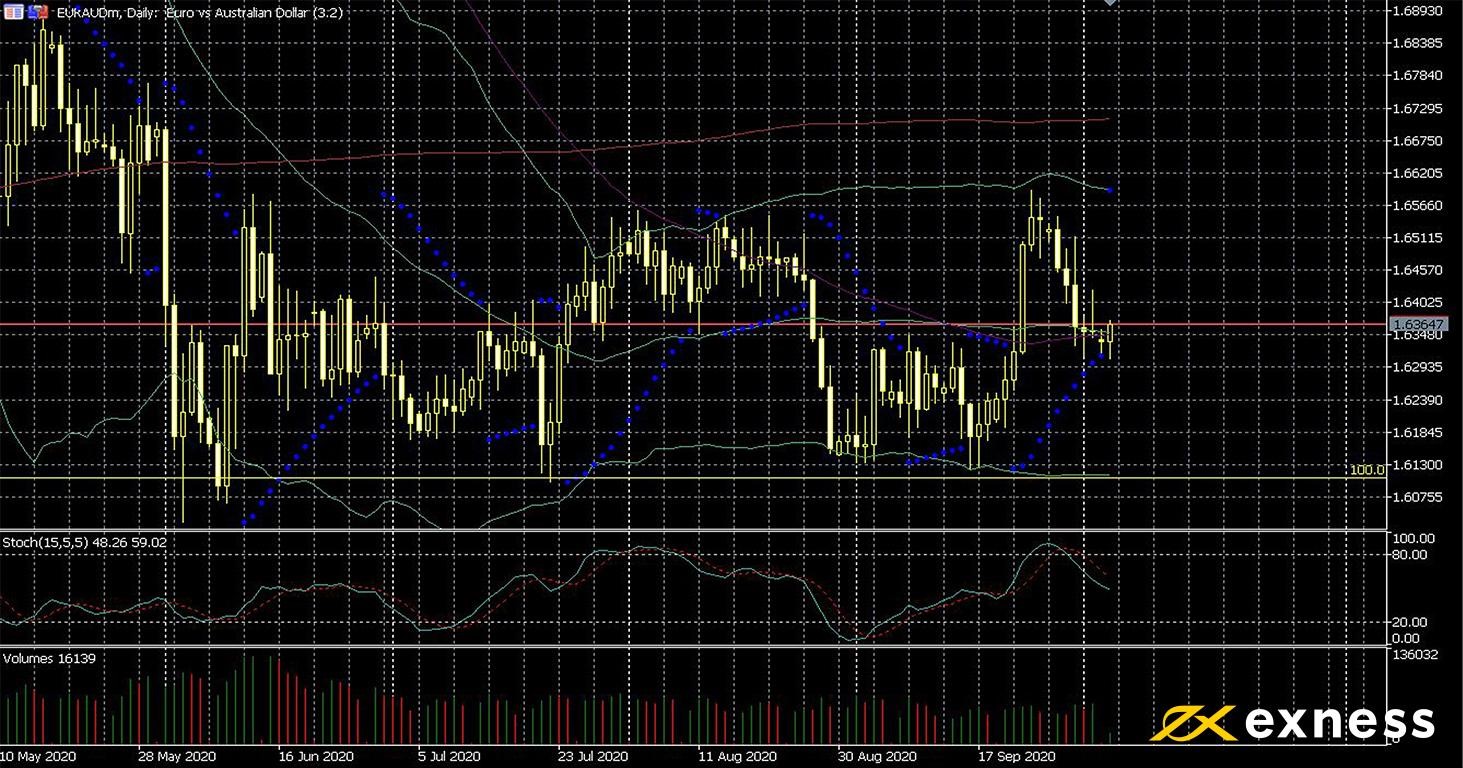

EURAUD had a boost this morning from strong data on retail sales from the eurozone. However, it has generally been languishing fairly low considering that disruptions to trade this year would usually be expected to hit the Aussie dollar harder than the euro.

The 100% weekly Fibonacci retracement area, in other words full retracement from the highs in February, seems to be established as a strong support. There haven’t been any clear fundamental drivers for either a bounce or a test of new lows over the past few weeks, though. Volume has decreased since June and the 50 and 100 moving averages have bunched quite close together.

Tomorrow morning’s trade data from Australia and the meeting of the RBA could provide more direction to the price this week. Equally, a weaker balance of trade from Germany on Thursday as expected could drive the euro down here.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 6 October, 0.30 GMT: Australian balance of trade (August) – consensus A$5.15 billion, previous A$4.61 billion

Tuesday 6 October, from 3.30 GMT: meeting of the Reserve Bank of Australia

Tuesday 6 October, 7.30 GMT: German construction PMI (September) – consensus 50, previous 48

Wednesday 7 October, 6.00 GMT: German industrial production (August) – consensus 1.5%, previous 1.2%

Wednesday 7 October, 6.45 GMT: French balance of trade (August) – consensus -€5.6 billion, previous -€7 billion

Thursday 8 October, 6.00 GMT: German balance of trade (August) – consensus €17.4 billion, previous €19.2 billion

Thursday 8 October, 11.30 GMT: accounts of the ECB’s monetary policy meeting

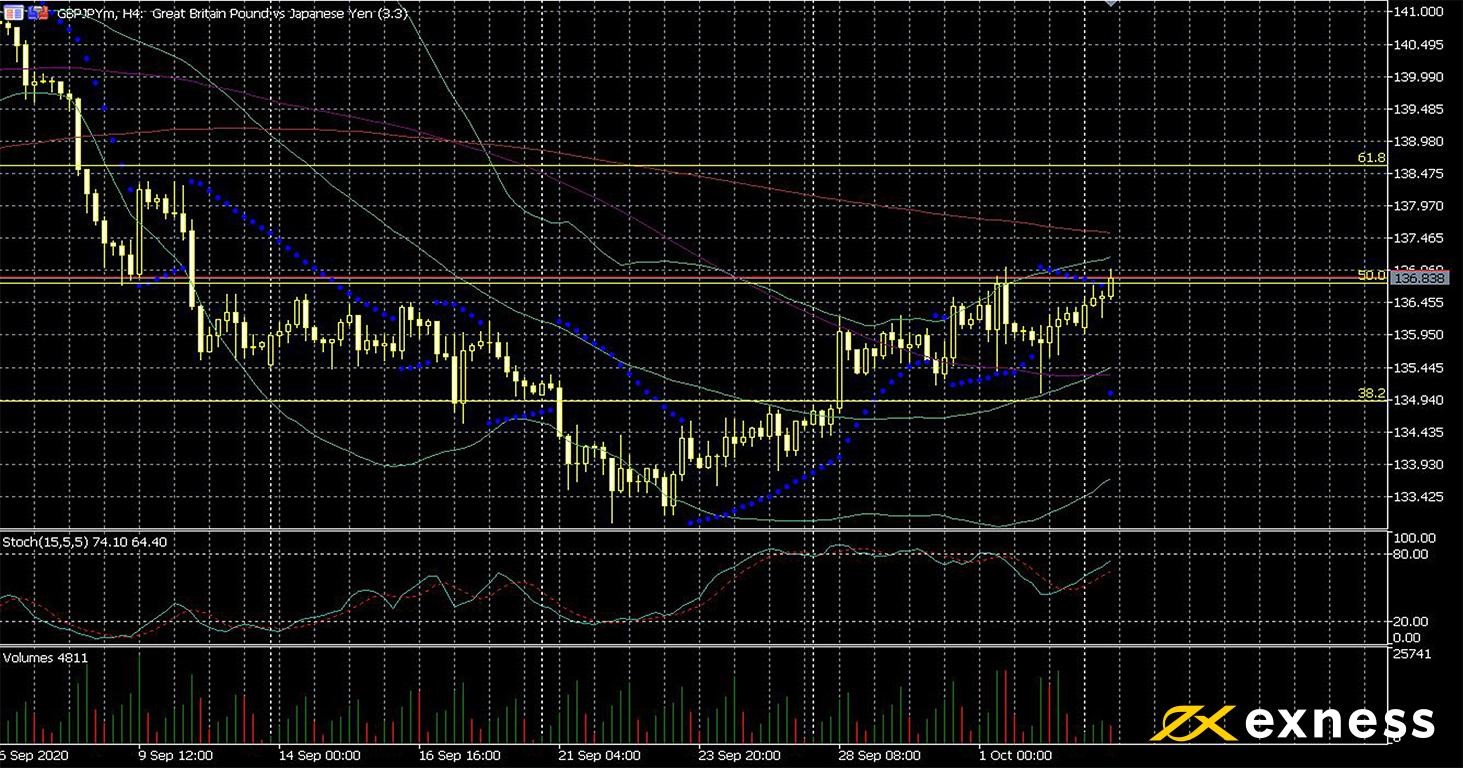

Pound-yen, four-hour

Very little has been heard of recent progress (or lack thereof) in ongoing UK-EU trade negotiations apart from Boris Johnson’s claim at the weekend that the UK can ‘more than live without’ a deal. No news has generally been bad news over the last few rounds of talks, but the pound is generally holding its strength against most major currencies so far this week.

From a technical point of view, it looks difficult for the pound to continue much beyond the 50% Fibonacci retracement area. The last test of this on Thursday failed very close to overbought. However, buying volume has remained dominant so far today and the 50 SMA from Bands is in the process of golden crossing the 100 while the slow stochastic (15, 5, 5) at 74 still hasn’t reached overbought.

Continuation upward over the next few weeks is probably contingent on at least a decent release from Friday’s balance of trade. While less important, traders will also probably monitor tomorrow’s construction PMI and Wednesday’s property data from the UK.

Key data this week

Bold indicates the most important release for this symbol.

Tuesday 6 October, 8.30 GMT: British construction PMI (September) – consensus 54, previous 54.6

Wednesday 7 October, 7.30 GMT: annual Halifax house price index (September) – consensus 6.6%, previous 5.2%

Wednesday 7 October, 23.50 GMT: Japanese current account (August) – consensus ¥1.98 trillion, previous ¥1.47 trillion

Friday 9 October, 6.00 GMT: British balance of trade (August) – consensus £600 million, previous £1.1 billion

Friday 9 October, 6.00 GMT: British annual construction output (August) – consensus -8.8%, previous -12.8%

Friday 9 October, 6.00 GMT: British annual industrial production (August) – consensus -4.6%, previous -7.8%

Friday 9 October, 6.00 GMT: British annual manufacturing production (August) – consensus -5.9%, previous -9.4%

Disclaimer: opinions are personal to the author and do not reflect the opinions of Exness or LeapRate.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.