This article was submitted by Michael Stark, market analyst at Exness.

Shares have generally recovered cautiously so far this week as sentiment has improved, while EU natural gas reached new record highs. Among currencies the biggest mover so far has been the lira, which has bounced strongly after news of a new governmental programme to protect savings from fluctuations. Otherwise this is likely to be a fairly slow week as the USA and many other major economies take a day off on Friday. This preview of weekly data looks at gold and dollar-peso ahead of American data on Wednesday and Thursday.

Central banks were in strong focus last week as the Fed, ECB and BoE all met, with the BoE surprising some by hiking its bank rate to 0.25% from the record low of 0.1%. Generally speaking, the current impression is that central banks will need to taper QE more quickly and decisively in the first quarter of next year given strong, ongoing pressure from inflation, which is continuing to increase in many countries. However, the People’s Bank of China made a very small cut of 0.05% to its loan prime rate yesterday morning GMT. This week there are no meetings of major central banks.

It’s also a fairly inactive week in terms of regular economic data, but participants in markets are looking ahead to American GDP on Wednesday followed by personal income and personal spending on Thursday. Regionally important releases centre on Mexico, which will release retail sales and job data in the middle of the week followed by balance of trade on Friday.

Gold, daily

Gold hasn’t moved very much so far this week as initial lows yesterday by many major indices have been recovered at least somewhat while traders also weigh the balance between a more hawkish outlook for monetary policy with expectations of high inflation lasting well into 2022. So far, the troubled progress of the American government’s Build Back Better hasn’t affected havens significantly.

For the time being, the bias based on TA still seems to be towards the upside but a clear breakout above $1,800 might still be some way off. The latest attempt to move above this important psychological area was rejected on Friday, and with activity likely to drop in the runup to Christmas there probably won’t be a sudden upsurge of momentum this week. However, surprising releases from the USA on Wednesday or Thursday could drive short-term volatility.

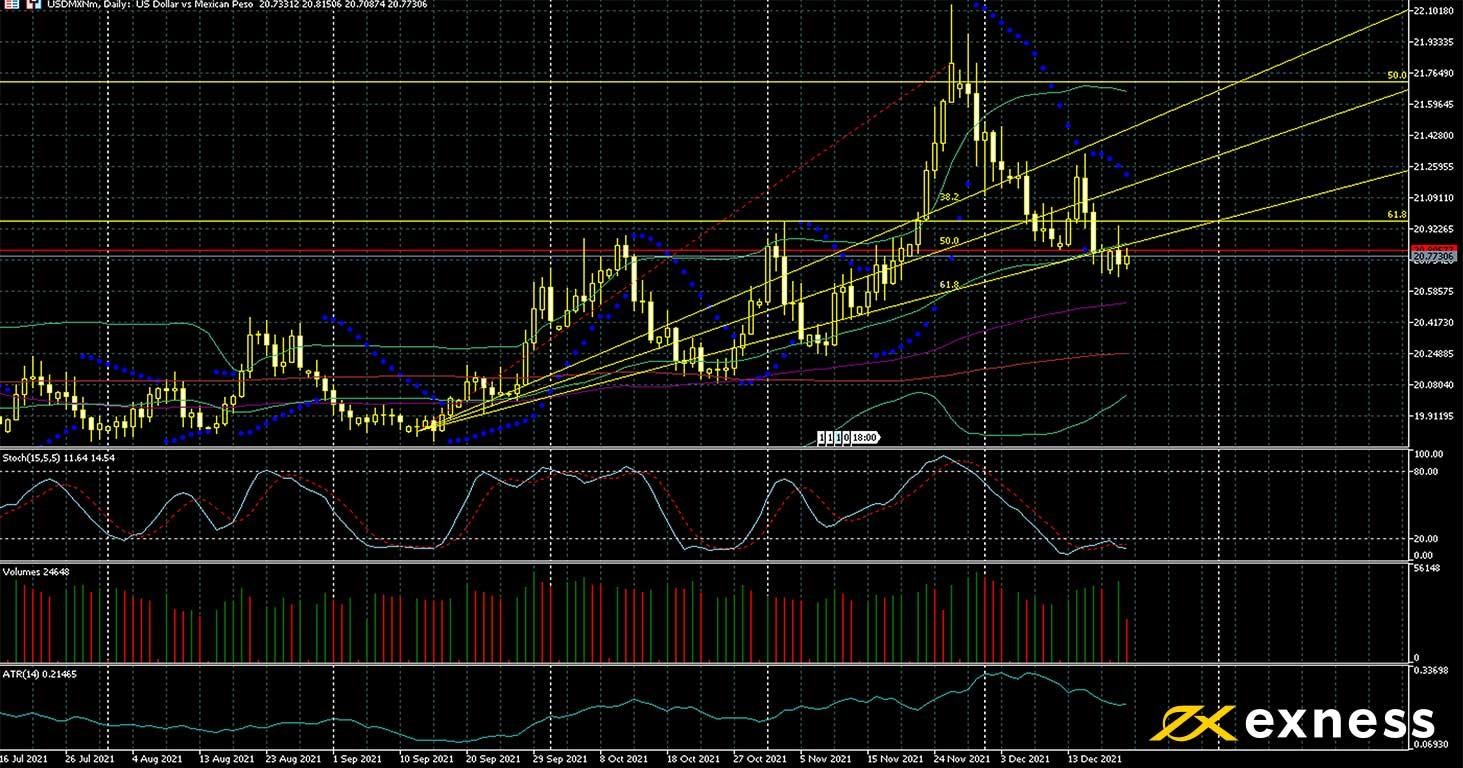

The peso has retraced much of its losses in Q3 so far this month in a fairly consistent downward movement by USDMXN. The hike of Mexico’s benchmark rate of half a percent last week, taking it to 5.5%, was higher than expected, which has boosted sentiment. The Banco de Mexico has been among the most hawkish of OECD/G20 central banks this year, with a total of five rate hikes totalling 1.5%. Inflation in both countries has increased sharply, especially this quarter, with expectations for core inflation next year also going up this month.

Further strong losses from here in the immediate future seem to be unfavourable. The slow stochastic at around 11 has clearly moved into the zone of selling saturation, while the 100 SMA is a potential support around $20.50, before the main psychological area of $20. Average true range of about 21 cents suggests that the maximum likely movement by this week’s close would be around 60c. Equally, though, any bounce from here would also probably be limited by the 61.8% weekly Fibonacci retracement area slightly below $21.

Relatively speaking, this is a fairly active week of data for USDMXN, especially on Wednesday and Thursday, so intraday opportunities in both directions are likely. Christmas Eve is not an official holiday in Mexico, so activity might be comparatively high for the peso that day, especially around balance of trade at noon GMT.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.