This article was submitted by Michael Stark, market analyst at Exness.

Asian and European shares generally moved up slightly on Monday morning as markets anticipate a highly active week in monetary policy and regular data. Gold and oil have both held near familiar areas from the end of last week. This preview of weekly data looks at XAUUSD and EURUSD.

There weren’t any significant noises from central banks last week, but American inflation as released on Friday reaching a high of nearly 40 years now has participants in markets expecting fairly immediate action by the Fed. This is an extremely busy week in monetary policy: the FOMC, ECB, BoE and BoJ are the major central banks due to meet in the second half of the week, while the central banks of Hungary, Norway, Switzerland, Turkey, Mexico and Russia are also due to decide on rates over the next few days.

It’s likely that most currencies will be quite active around these meetings and press conferences, especially on Wednesday night as the Fed meets. The Central Bank of the Russian Federation and the Banco de Mexico are both expected to hike rates.

This is also a busy week in terms of regular economic data. Claimant count change is the top release, with eyes also on British and Canadian inflation plus Australian job data. Oil might continue to take a breather over the next few days and consolidate, but volatility seems to be ahead for most forex pairs.

Gold-dollar, daily

With the FOMC’s statement and press conference coming up on Wednesday, gold’s reaction to increasing American inflation has been muted. 6.8% non-core inflation in November in the USA is the biggest annual increase since 1982, driven mainly by soaring prices for fuel. Participants in markets widely expect the Fed to signal faster tapering of quantitative easing on Wednesday night although clear hints on the timeline for raising rates seem unlikely at this stage.

The current channel is narrow with $1,770 and $1,800 remaining in view as likely boundaries. The bias for gold based on fundamentals seems to be towards buying unless the Fed is very hawkish on Wednesday, but TA remains noncommittal. All three moving averages are above the price and momentum upon emergence from oversold (based on the slow stochastic) was lukewarm at best. ATR has also declined below 16, making a push back to $1,800 less likely in the immediate future.

Perhaps more so than major forex pairs, gold is prone to making sharp movements around key releases such as meetings of the Fed. Going with the flow of sentiment from Wednesday night and avoiding long-term positions at this time of year seem to make sense in the context.

Key data this week

Bold indicates the most important release for this symbol.

from 19.00 GMT: statement and press conference of the Federal Open Market Committee

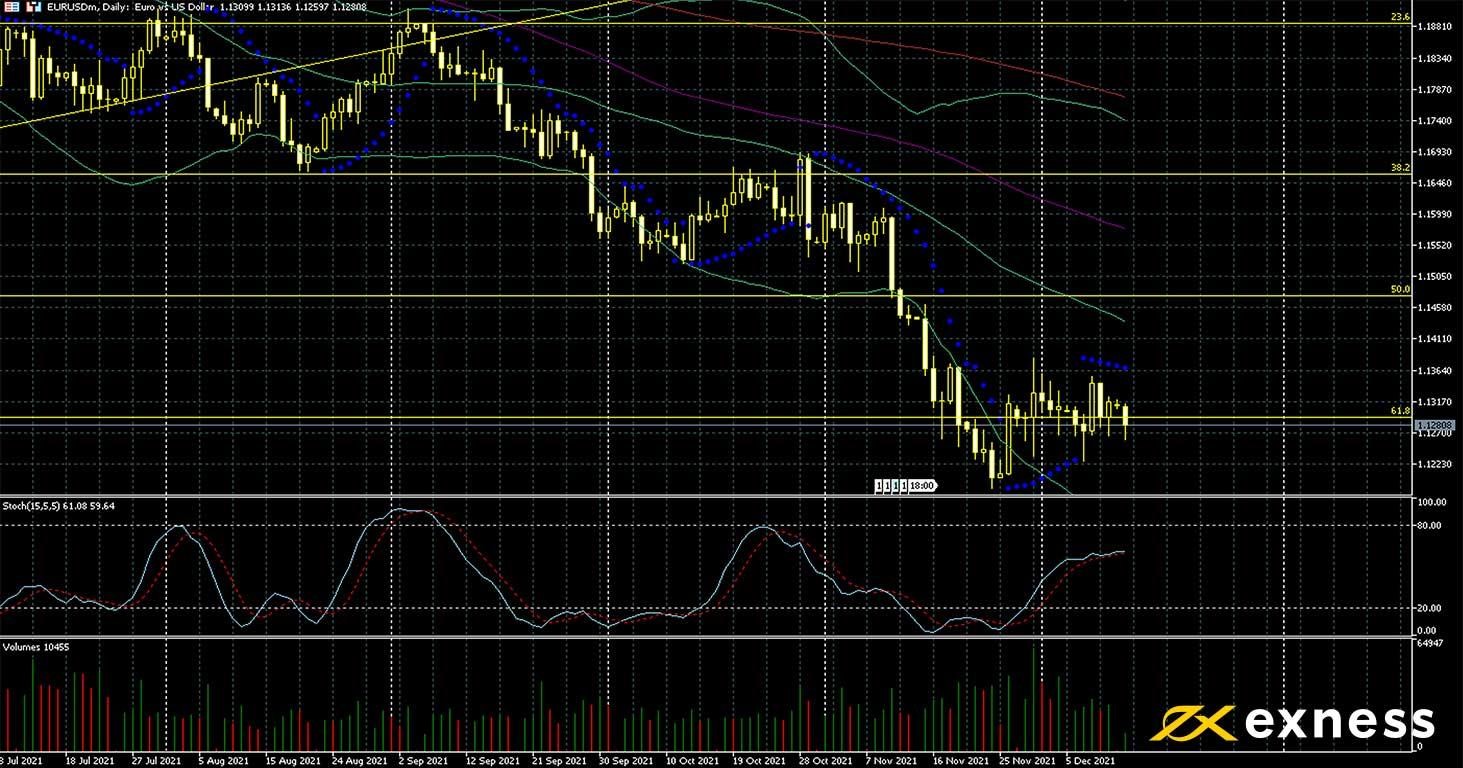

Euro-dollar, daily

Euro-dollar remains close to last month’s low of about a year and a half of $1.12 as participants await the meetings of the FOMC and ECB on Wednesday and Thursday. As of now, it seems likely that the Fed will be much more hawkish than the ECB: the eurozone’s economic growth has slowed overall this quarter, so policymakers are likely to weigh the pros of trying to tackle inflation against the cons of possibly damaging recovery further if loose policy is abandoned too quickly. Based on expected data, inflation in the eurozone in November was less than half that in the USA.

From a technical standpoint, it seems quite possible that the downtrend could continue and maybe even test $1.10 in the new year. The response of buyers around $1.12 was fairly muted and although there has been no clear breakthrough below the 61.8% Fibonacci retracement area, should this be achieved more losses are likely.

Depending on sentiment around the middle of the week, the other clearly possible scenario is consolidation around $1.12-$1.13 for an extended period. Traders should remember that Friday’s data from the eurozone might affect participants’ sentiment significantly and alter the picture that might develop in the aftermath of the central banks’ meetings, so it will be key to monitor medium-term positions closely in the second half of the week.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.