This article was submitted by Michael Stark, market analyst at Exness.

This week in markets started fairly quietly with a holiday in the USA for Washington’s Birthday and declines for many European shares as participants continued to focus on tension around eastern Ukraine. With commodities still experiencing high volume of trading amid very high inflation and the Reserve Bank of New Zealand likely to hike its cash rate on Wednesday morning, this preview of weekly data considers XAUUSD and NZDUSD.

There wasn’t much activity last week among central banks, with the likelihood of a two-step hike by the Fed next month now having dropped below 20%. This Wednesday, eyes are on the Reserve Bank of New Zealand which is widely expected to hike its cash rate to 1%. Annual non-core inflation at 5.9% is lower than in the USA but still a significant challenge, so this might be the start of a cycle of rate hikes.

The most important regular data this week come from the USA, specifically GDP growth on Thursday and income and spending on Friday. This isn’t likely to be a particularly active week but there might be opportunities for commodities and the Kiwi dollar as sentiment possibly changes from Tuesday’s open.

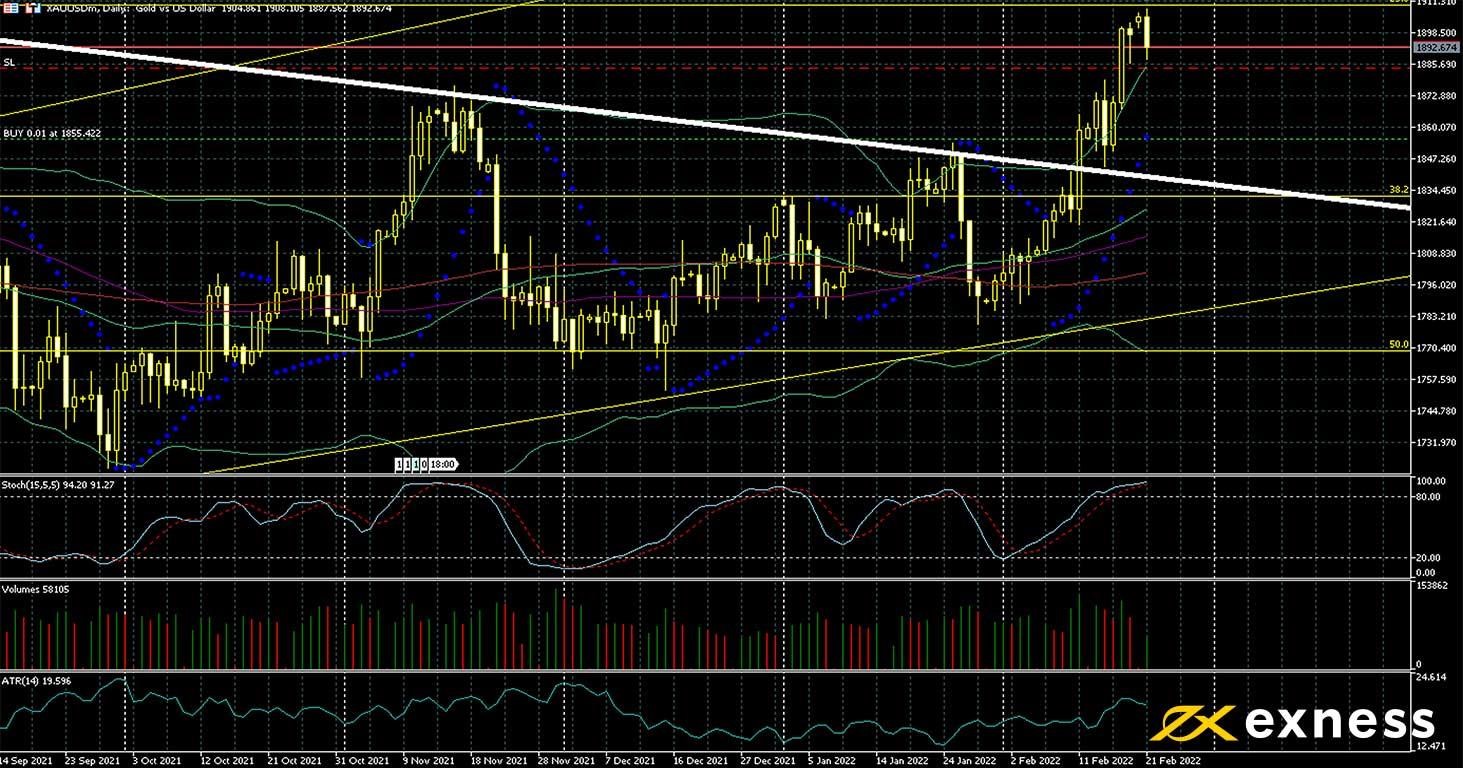

Gold, daily

Gold’s decisive breakout has been halted for now around the key psychological area of $1,900. The focus remains on 40-year highs in American annual inflation combined with opinions among some participants that the Fed isn’t acting quickly enough to tackle rising prices. Although tension between the USA and various European countries on one side and Russia on the other has remained quite high, the immediate threat of war seems to have receded at least for now, so demand for havens has decreased.

With very strong buying saturation based on both the slow stochastic and Bollinger Bands and the presence of an important psychological resistance, another move up in the immediate future doesn’t look likely. Instead, new buyers would traditionally look for a fairly small retracement to the area of about $1,880 based on ATR before looking to join another possible upward wave. There’s no critically important data for gold this week but sentiment on monetary policy can change rapidly, especially with active American markets from Tuesday.

30 GMT: American personal income (January) – consensus negative 0.3%, previous 0.3%

30 GMT: American personal spending (January) – consensus 1.5%, previous negative 0.6%

New Zealand dollar-US dollar, daily

Participants in forex markets widely expect the Reserve Bank of New Zealand to hike its cash rate to 1% on Wednesday morning. After two hikes last year, the RBNZ seems likely to hike its rate at every opportunity in 2022; if this impression holds over the next few days, the Kiwi dollar might try to move up more seriously. Despite unemployment in New Zealand at 3.2% – the lowest since equivalent records began in 1986 – and inflation at nearly 6%, a half percent hike doesn’t look like more than a remote possibility.

On the chart, the 100% weekly Fibonacci retracement – full retracement of all losses in the first quarter of 2020 – remains an important area that might continue to cap losses. However, the three moving averages above the prices also present potential hurdles if there’s a move up this week. Apart from the meeting of the RBNZ, traders of NZDUSD and others are looking ahead to Friday’s balance of trade from New Zealand as well.

Key data this week

Bold indicates the most important releases for this symbol.

Wednesday 23 February

from 1.00 GMT: statement and press conference of the Reserve Bank of New Zealand

Thursday 24 February

30 GMT: American quarterly GDP growth (second estimate, Q4) – consensus 7%, previous 2.3%

30 GMT: American quarterly GDP price index (second estimate, Q4) – consensus 6.9%, previous 5.9%

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.