This article was submitted by Michael Stark, market analyst at Exness.

Markets started the week without clear direction in many cases although Chinese shares have surged so far today. The People’s Bank of China injected more liquidity into financial markets, and the Shanghai Composite added nearly 2.5% in today’s session. This preview of weekly forex data takes a look at conditions in markets and the key releases to affect GBPJPY, USDCAD and EURNOK.

Japanese GDP data late last night GMT were very negative. Preliminary GDP growth for the second quarter of 2020 indicated a drop of 7.8% (annualised as -27.8%), the worst result since comparable records began in 1980. Thai GDP also dropped 12.2% annually for Q2. Although this latter release wasn’t quite as bad as expected, it’s still the biggest quarterly drop since 1998.

Central banks were fairly inactive last week except for Banxico, which cut its benchmark rate half a percent to 4.5% as expected. This week’s meetings include the Norges Bank and the CBRT.

This week’s main regular releases are inflation in Canada, Japan and the UK. Japan’s balance of trade just before midnight on Wednesday GMT is also an important release. Earnings season continues this week with releases of reports from Walmart, Nvidia and Alibaba on Tuesday, Wednesday and Thursday respectively: sentiment in stock markets is likely to remain key for many currencies throughout the week.

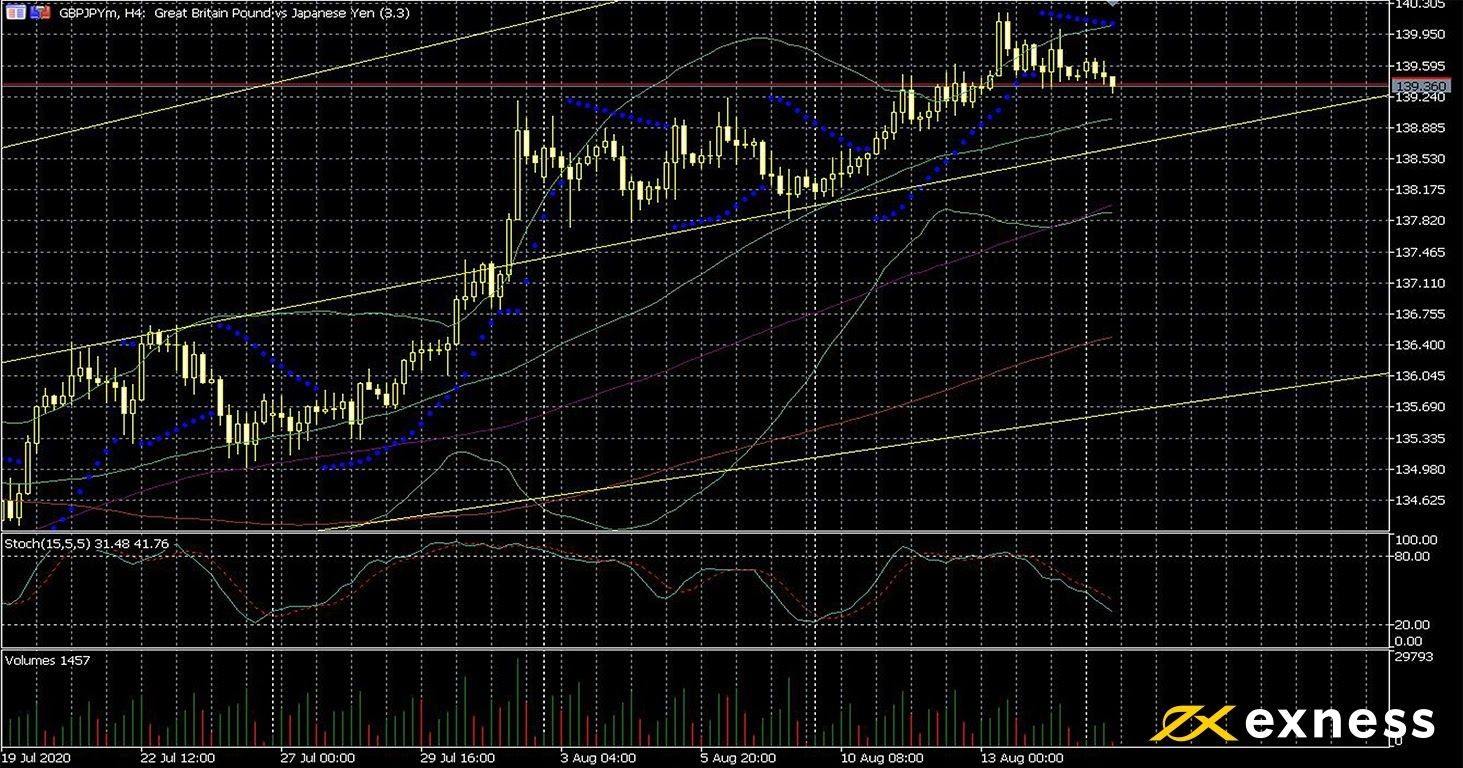

Pound-yen, four-hour

GBPJPY has so far failed to make much headway this week despite the historic negative GDP release from Japan this morning. Sentiment on the pound remains pretty nervous, with Brexit talks resuming tomorrow. Snippets of news from these are likely over the next few days, but the next official report of progress is due on Friday. Meanwhile Japan’s state of emergency continues to weigh on the economy, with various Japanese exports such as cars declining by more than 50% compared with this time last year.

From a technical perspective, the uptrend is still active here although momentum has been somewhat lower since last week. The focus of this chart is the 50 SMA from Bands, coming just above the 50% zone from the daily Fibonacci fan. Currently there’s no sign of overbought from either Bands (50, 0, 2) or the slow stochastic (15, 5, 5). The latter at about 31 is closer to oversold than neutral.

This is a fairly big week of data for pound-yen. The most important releases are on Wednesday and Thursday night, with inflation from both countries and Japan’s balance of trade taking centre stage. British Gfk consumer confidence and retail sales could also drive some volatility.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 18 August, 23.50 GMT: Japanese balance of trade (July) – consensus-¥77.6 billion, previous -¥268.8 billion

Dollar-loonie’s consolidation has continued so far this week as oil remains close to its recently achieved highs and there’s generally little demand for the US dollar. News that the review of the phase one trade deal between the USA and China has been delayed would usually be expected to drive gains on this chart. However, fundamentals have been fairly subdued for USDCAD recently.

The focus of many traders is the 100% daily Fibonacci retracement area, i.e. complete retracement of the greenback’s gains since late February. This critical zone has held as a support since the second half of last week. The catalyst for a clearer bounce could be Canadian annual inflation on Wednesday: if the consensus of about 0.5% is correct (last month’s figure was 0.7%), the US dollar might be able to move up a bit more here.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 18 August, 30 GMT: API crude oil stock change (14 August) – previous -4.4 million

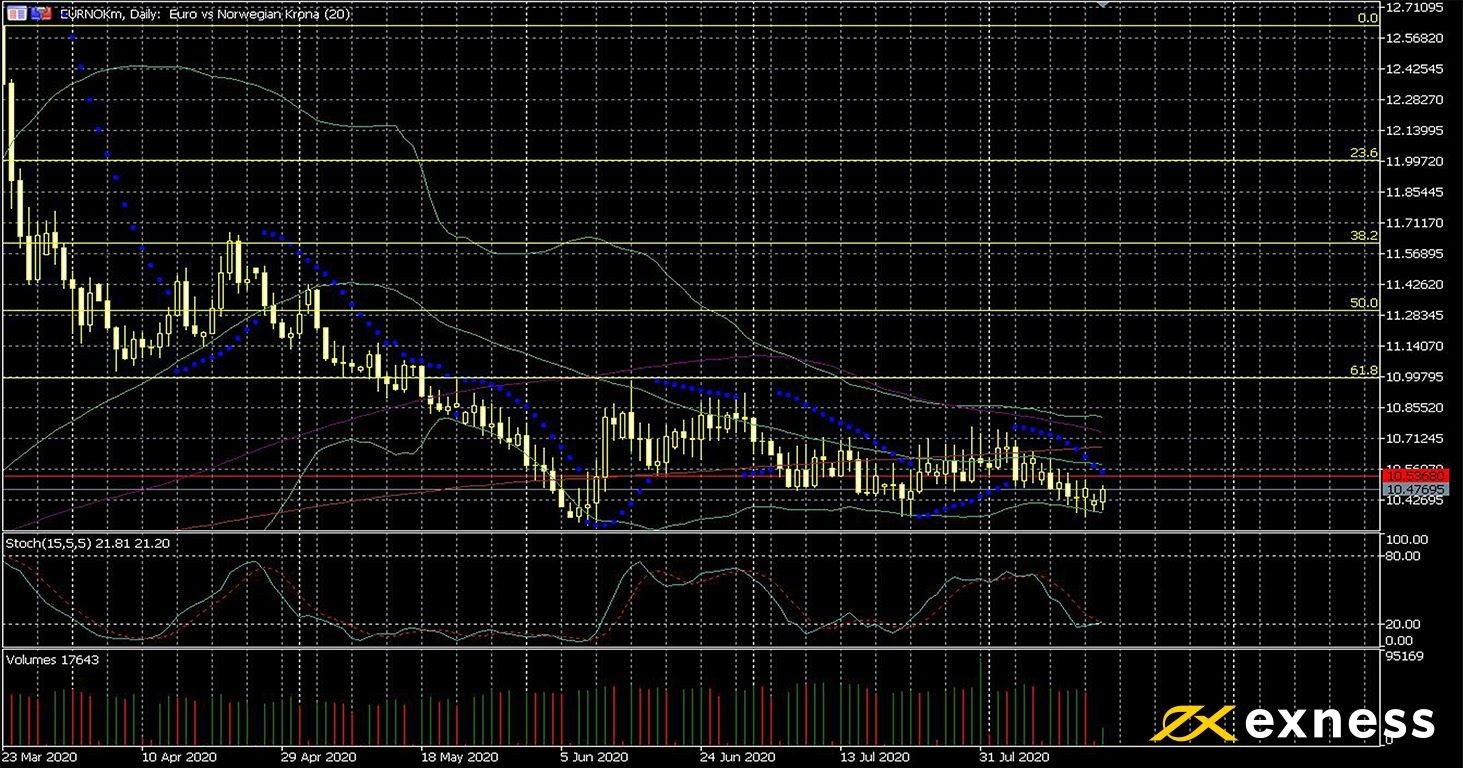

The euro’s recent losses against the Norwegian krone have come to an end for now around 10.30 kr. Oil’s weaker momentum upward and lacklustre data from Norway are key factors. This morning’s balance of trade from Norway for July came in at negative 1.8 billion kr against the expectation for positive 7.8 billion kr. The previous figure was also revised down below negative 10 billion kr. Meanwhile the euro is still doing quite well against most major currencies despite some local increases in cases of covid-19 over the past week.

A common principle in TA is that a trend should be considered active until there is clear evidence that it has ended, so in this case we can expect more losses sooner or later for the euro unless there’s a clear attempt to move back above the 61.8% daily Fibonacci retracement area. The 50 SMA from Bands recently completed a weak death cross of the 200; June’s death cross of the 100 SMA was much clearer. All three MAs have now bunched fairly closely together, reflecting the general lack of direction.

The Norges Bank isn’t expected to make any change on Thursday to its current key policy rate of zero percent, the last cut of 0.25% having come in early May. However, what the central bank says about quantitative easing and the outlook for trade over the next few months is likely to be very important for this pair in the second half of the week. There isn’t any other critical release this week, but traders will still probably watch eurozone-wide inflation on Wednesday morning and German PPI on Thursday.

Key data this week

Bold indicates the most important release for this symbol.