The US dollar index, which measures the performance of the greenback versus a basket of other major currencies, is flat during early Tuesday trading. After reaching a multi-decade high earlier in the month, hitting parity with the euro for the first time since 2002, the dollar lost some gas, as investors priced-out the possibility of the Fed announcing a 100bp rate hike tomorrow, when it concludes its July meeting. The scenario everyone is working under is that Jerome Powell will announce a 75bp rate increase, with the markets attention now focusing on the tone used by the Chairman of the Fed; will he remain fully committed to controlling inflation, or instead show concerns over growth prospects for the US economy? The direction provided by the chairman of the Fed during his statement on Wednesday is likely to determine the performance of the dollar in the weeks ahead.

Ricardo Evangelista – Senior Analyst, ActivTrades

Oil

Brent crude oil prices are rising during early Tuesday trading, in a second consecutive day of gains. Concerns over the supply of Russian gas to Europe are having a collateral impact on oil prices, as a potential squeeze on gas supplied to Europe is likely to increase demand of oil and other related fuels such as diesel. As anxiety grows in Europe over gas supplies, many now contemplate the possibility of Russia completely turning off the tap, leading to a switch from gas to oil, diesel and other related fuels, in a dynamic that is likely to see further rises in the price of the barrel.

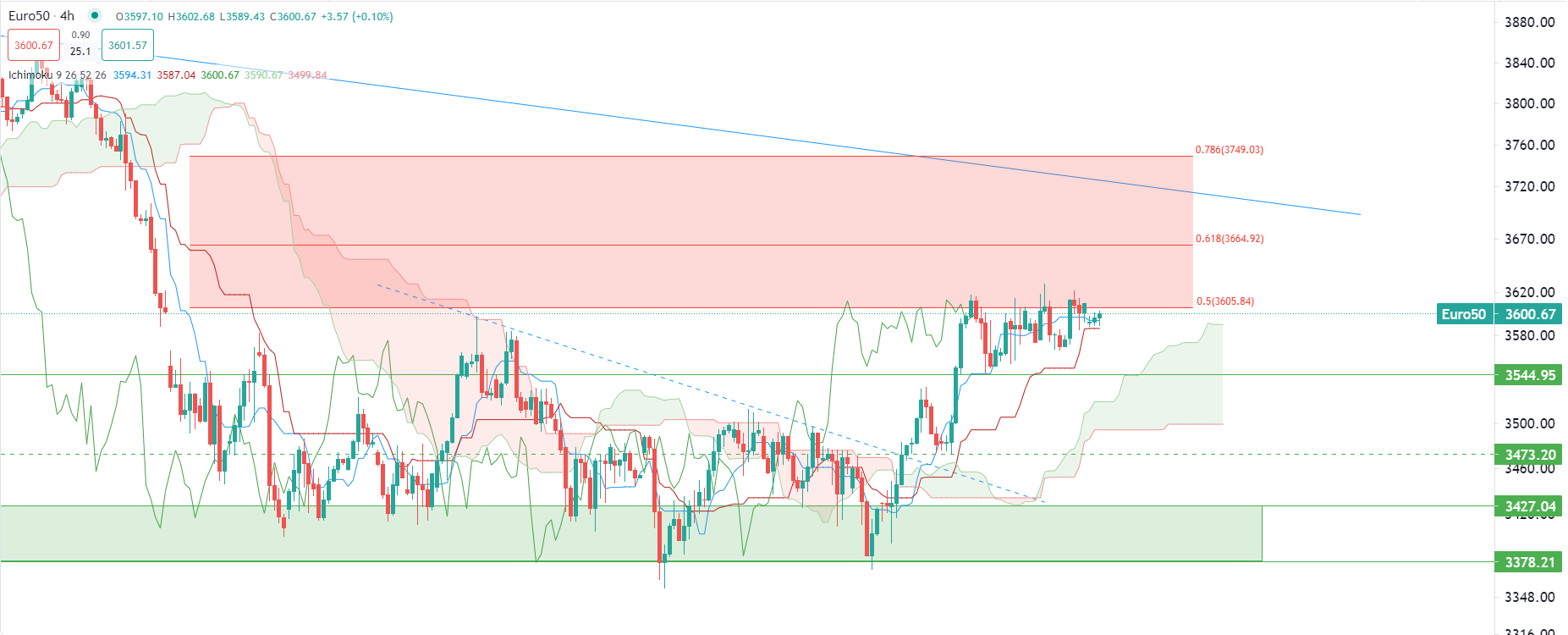

European stocks fluctuated on Tuesday, alongside US Futures, as traders brace for the incoming policy decision from the Federal Reserve this week. There is a sense of the calm before the storm on the market today, with treasuries remaining stable while most indices are trading sideways without clear direction. This is seen as a sign of expectation from investors as most of them are waiting for tomorrow’s widely expected 0.75bp rate hike from the Fed, alongside further potential policy signals. Meanwhile, market operators are likely to keep their focus on the corporate front with earning reports from Coca-Cola, Alphabet, Microsoft and General Motors, while European stock traders will cautiously monitor results from Dassault System, LVMH and Michelin. Even though the current covid curbs in China combined with the energy crisis with Russia stay as lingering risk for European equity markets, the STOXX-50 index remains well oriented. Prices continue to trade around 3,600.0pts with no short-term bearish sign in sight. A clear break-out of this resistance could quickly drive the market further up, towards 3,665.0pts and even 3,750.0pts by extension.

Pierre Veyret– Technical analyst, ActivTrades

Disclaimer: opinions are personal to the authors and do not reflect the opinions of LeapRate. This is not a trading advice.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.