The following market analysis was prepared for LeapRate by Ramy Abouzaid, ATFX (AE) Head of Market Research.

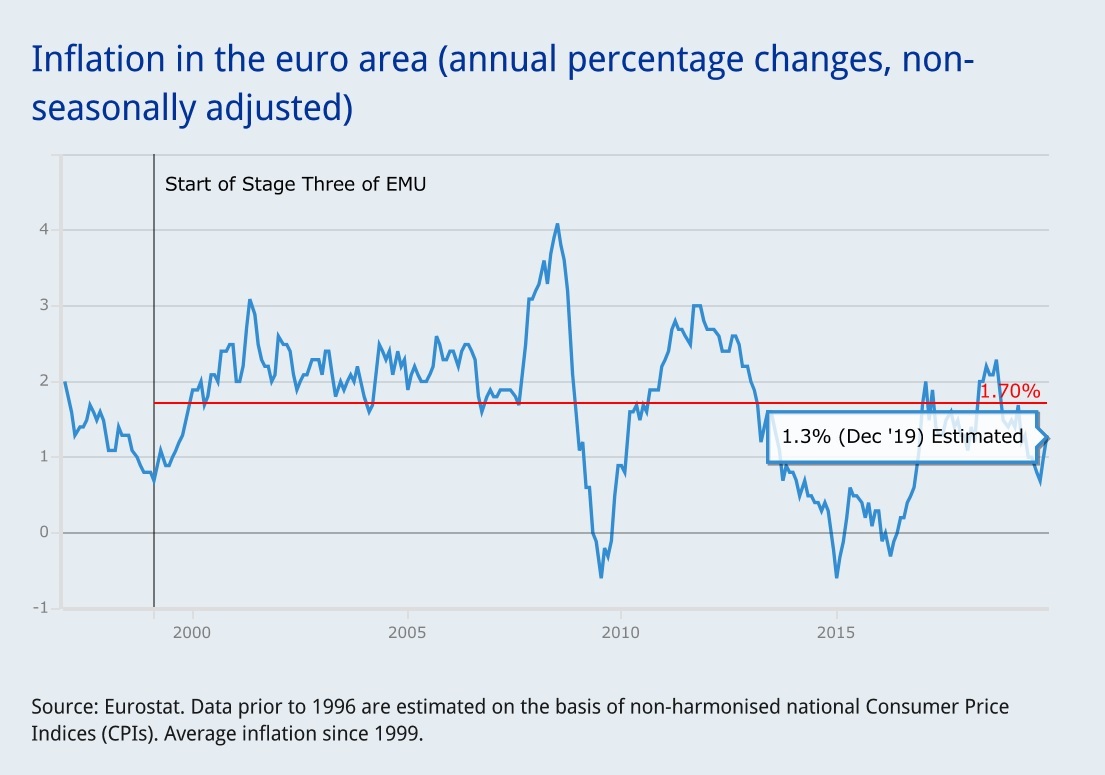

Despite the significant spike of the inflation rate across the 19 economies of eurozone, which reached a six-month high last month – the European Central Bank is still far from reaching its range of 2% inflation rate needed to reflect how healthy the economic landscape really is.

The main reason behind all the fuss of the 2% rate, is to maintain price stability in the euro area as a whole. Maybe we’re not there yet, but it might seem that we’re heading towards the right direction. Latter reports of CPI in Euro Zone countries, show a steady growth since October. In the past 3 months, the inflation increased respectively from 0.7% to 1% reaching its peak in December with a 1.3% rate. One thing to keep in mind while reading the chart below; the recent inflation rates are directly influenced by the increase money supply, a policy applied by the ECB through quantitative easing to give an artificially boost to the economy.

So, the CPI are showing improvement but still below target – what should we conclude from that, you may ask?

Well, the markets are eagerly waiting for any statement, slip, hint, or really anything from the ECB officials to come up with assumptions. According to Yves Mersch, ECB’s governing council member, the final reports are showing good signs of stabilization, and his body language showed confidence – if you’re into reading behavioral signals. He also went to proudly stating that they “were proven right to have accommodative policies” and that “other policy areas need to kick in to help the ECB”. Being on the conservative side for too long, Mersch new laidback attitude could help the markets feeling more revealed towards reaching inflation target.

But, should we really just count on Mersch rare good mood?

It is definitely too early to conclude whether the eurozone economic slowdown has reached its end. Especially when another ECB governing council member doesn’t share Mersch enthusiasm. For Robert Holzmann, even if the rates are getting better, as long as the target isn’t reached “negative rates will send the wrong signal” –and he might be right. Markets do dance to signal rhythms. Holzmann worry is also backed by the fear of a possible negative impact on the long term, on “productivity, banks and financial stability”.

Maybe it is better to leave them arguing until this week’s ECB meeting, and switch our focus to other significant indicators.

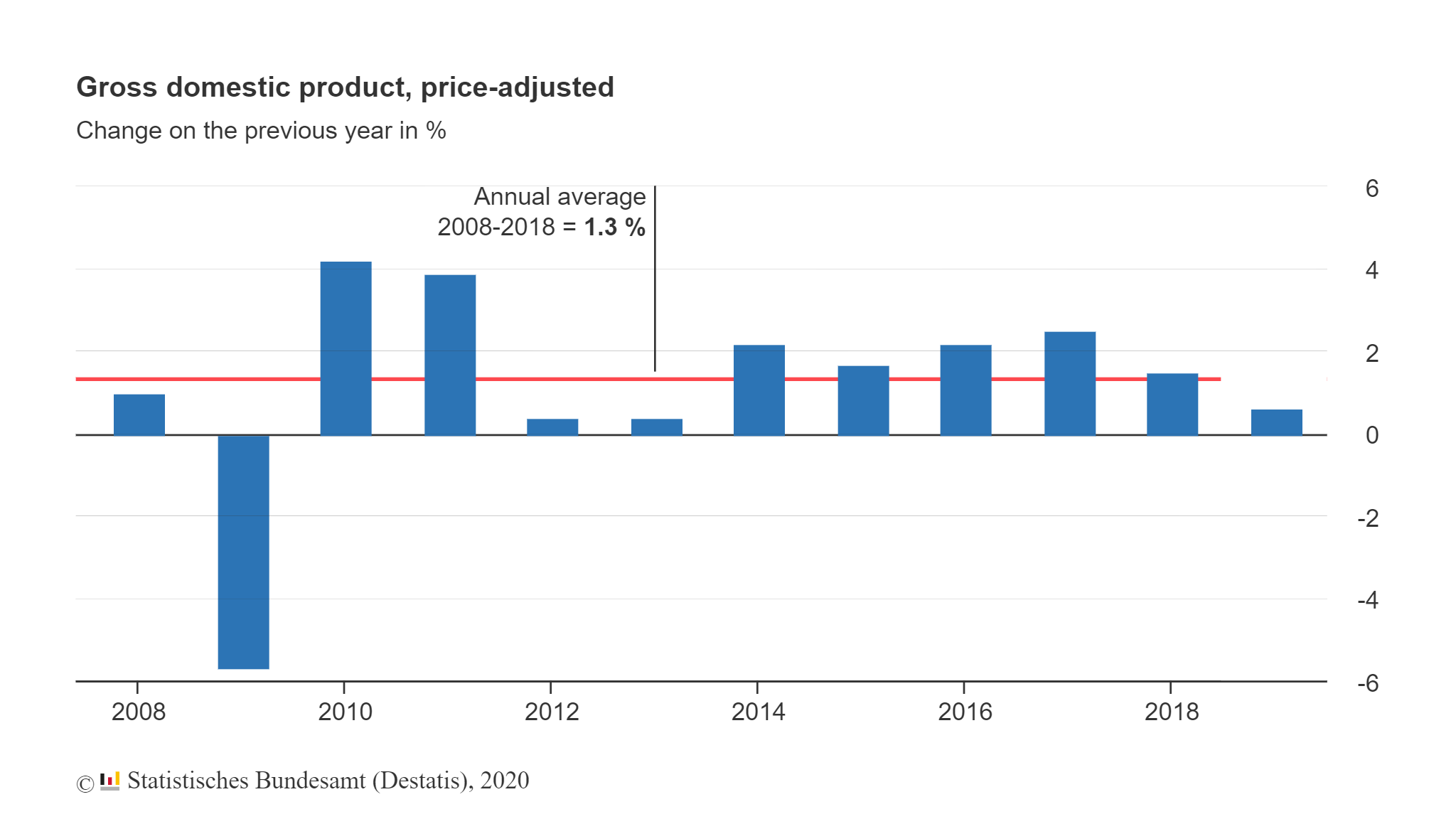

According to primary reports from the German Federal Statistical Office, Germany’s GDP witnessed an up stretch of 0.6% in 2019 compared to previous year. Even though the growth has been steady in the German economy for ten years in a row now – longest period of continuous economic growth in Germany – but it has definitely reached a slower tempo in 2019. We can have a better understanding of that, if we compare last year’s growth to its previous two years (GDP for 2017 grew by 2.5%, and in 2018 grew to 1.5%).

Nothing seems too worrying, but most European economies do remain under pressure. Besides, final inflation rate doesn’t necessarily say the whole truth. A breakdown of main components in the inflation reports could be more important indicators for the ECB. For example, the main player in last month’s report results was energy price inflation, which went from -3.2% in November to 0.2% in December. Since non-energy industrial goods are directly connected to the state of global economy, the ECB should be keeping an eye on that.

For now, the main “gossips” in the markets are talking about a readjusted inflation target. A strategy that might help removing pressure from adapting tightening policy. Another scenario would be extending quantitate easing for a bit longer; a strategy that could serve the markets for the upcoming months, in hope that the economy can get itself together, act like a grownup for a change and leave the parents garage for good.

In any case, our expectations for the impact of this meeting on the euro will likely be instantaneous. However, If the ECB’s headed by Lagarde, adopted a different unexpected action, would it be a pleasant surprise for the markets or not? We can only wait and see.

What ECB Dove and Hawk members chart?

In general, “Hawk” are members inclined to tighten monetary policy to reduce inflation and accelerate growth while “Dove” members tending towards easing monetary policy to support growth and inflation.

Note – We have built this evaluation of the ECB Dove and Hawk members based on published members statements, interviews and recent voting in the monetary policy meetings, but it must be noted that all views here are self-evaluating – and that very few “Centralists” bank members explicitly describe themselves as Hawk or as Doves. Our opinions may differ from the views of others. It should also be noted that some members tend to historically stick to one side, while others tend to be more flexible in their decisions, shifting from one side to another.