The following article is based on research by Marshall Gittler, Head of Investment Research for FXPRIMUS.

FXPRIMUS Week in Focus for the week beginning 6 March: People’s Congress, ECB & RBA meetings, UK Budget, US NFP

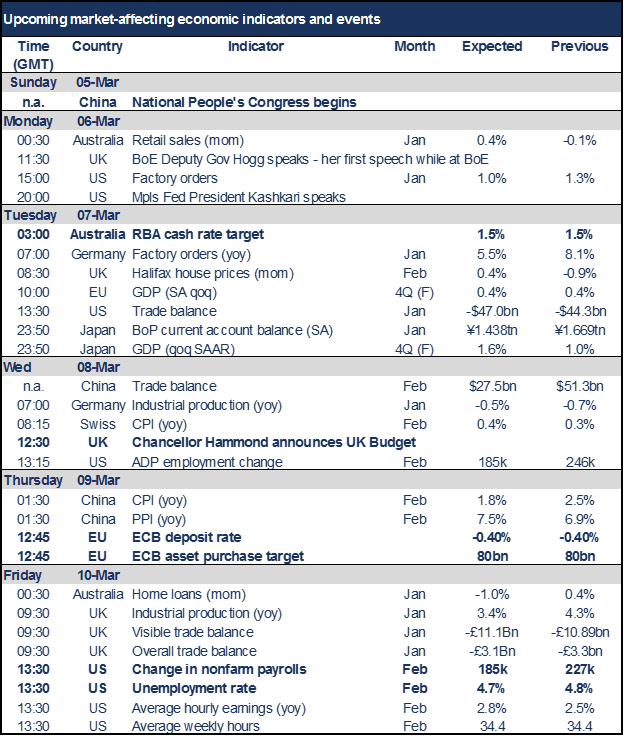

It’s a week filled with important events and indicators from all over the globe.

The week’s events started Sunday with the National People’s Congress (NPC) opening in China, the largest legislative body in the world. The Congress is where the government sets out its working plan for the year and perhaps a development plan for the next five years. On the first day they lowered their growth target slightly from last year’s 6.5%-7% target to just 6.5%, but that small change failed to dent AUD. Investors will pay particular attention to Premier Li Keqiang’s closing press conference. The closing date of the Congress is not yet set.

Britain announces its FY2017/18 budget on Wednesday. It’s been reported that the Government will sharply upgrade its growth forecasts and reduce the borrowing forecast. An upgraded economic outlook could prove positive for the pound.

The ECB meets on Thursday. There’s little expectation that they will make any changes in rates or in their QE program. The focus is therefore likely to be on their new forecasts, particularly for inflation. An upgrade in the economic outlook and inflation forecast could be positive for the euro.

The RBA meeting Tuesday is not likely to attract much attention. Their last meeting was exactly a month ago, and since then there hasn’t been that much news either way. The market still sees only a small chance of a rate hike this year. Following last week’s plunge, AUD is little changed from where it was at the previous meeting. I don’t expect much change in the statement and I therefore don’t expect much change in AUD, either. But with Fed policy largely priced in now, the higher rates available in Australia could prove attractive for investors and boost AUD.

Finally, the other major event of the week is the US nonfarm payroll figure on Friday, preceded as usual by the ADP report on Wednesday. Its importance this month is more difficult to divine than usual, because the market is already forecasting a rate hike in March. It would take a disastrous figure to derail expectations for March and an exceptionally good figure to push forward expectations for the next rate hike, which is forecast to be either June or July. (There’s no meeting in April.) In that case, the market may focus on average hourly earnings. The consensus is looking for a sharp increase there, which could be dollar-positive.

Other notable data from the US this week includes factory orders today (Monday) and trade data on Tuesday.

For the EU, German factory orders on Tuesday and industrial production on Wednesday will be the only other major items in addition to the ECB meeting.

UK industrial production and trade will be released on Friday. The overall trade deficit is expected to narrow, but output is forecast to show a sharp slowdown on a yoy basis. I think that might be the more important number and GBP could weaken as a result.

Japan announces its current account balance and final revision of 4Q GDP on Wednesday morning Japan time. While the current account is expected to fall slightly on an SA basis, GDP is expected to be revised up, which could boost JPY.

Finally, China releases its inflation and trade data for February this week. Since the February data is always distorted by the Chinese New Year (27 Jan-2 Feb this year), the figures are not likely to be that market-affecting.