The following is based on research by John Hardy, Head of FX Strategy at Saxo Bank. More of John’s research can be seen at Saxo Bank’s TradingFloor.com.

- EURSEK could test 10.00 level

- EURUSD projections indicate 1.2300-plus

- ‘The Aussie truly is down under’

John Hardy, Saxo Bank

Global equities were under pressure overnight, picking up on the underlying theme of recent wobbles in risk appetite led by emerging market bond spreads and credit spreads.

The action seen in Asia was led by another very weak session in Japan as the JPY strengthened. The key 113.00 area is in play in USDJPY this morning – across FX, we are seeing classic patterns of “risk off” though the JPY has been a bit slow to pick up the pace, perhaps due to the recent rise in global yields that are normally JPY-negative.

As we have recently noted, complacency had reached remarkable levels recently making the current level of volatility appear more impressive than it should. Traders should keep in mind where we have come from in terms of extremely muted trading, so we should appreciate the potential for rapid range expansion.

In FX, this is especially the case in JPY crosses, EM, and even the less liquid of the G10 currencies (note the extreme SEK and NOK moves yesterday; more on those below).

Overnight, the AUD was weaker again on another weak round of wage growth data in Q3 – the year-on-year running at a mere 2.0% versus 2.2% expected and hardly any increase from Q2’s tepid 1.9%. As well, negative news on China has picked up a bit as economic data has cooled over the last couple of weeks of releases.

The lone cylinder that was firing consistently for the Aussie lately – a persistent rally in the large Australian mining stocks – has suddenly gone quiet as multi-year highs in the BHP Billiton and Rio Tinto behemoths have yielded to ugly tactical reversals in recent sessions.

AUDJPY was down emphatically through its 200-day moving average this morning and EURAUD continued its aggravated rally. The Aussie truly is down under, and any pickup in negative risk sentiment could see it in for a further pounding.

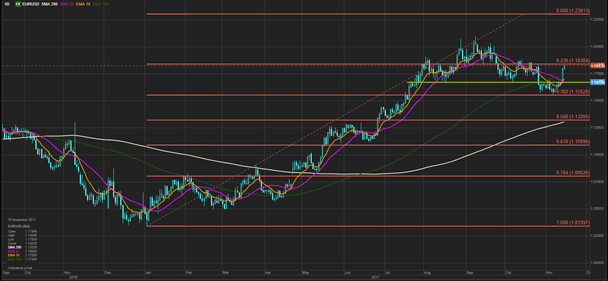

Chart: EURUSD

EURUSD pushed higher with conviction and with virtually no pullbacks as fresh longs were perhaps afraid of being left behind on the implications of the return back above the head-and-shoulders neckline and above 1.1700. The sharp, brutal reversal of the prior selloff wave shifts the tables on the bears and makes a convincing case for a fresh pull to 1.2000 and on to new highs.

The next projection suggests a move to 1.2300-plus in the months ahead if this rally indicates we have have put in a “fourth wave” low. Anticipation of US data up later today could bottle up the action in a nervous range ahead of the US session, but the bar is very high for today’s data to counter this technically decisive move.

Source: Saxo Bank

The G-10 rundown

USD – the EURUSD picture has turned bullish, but the bulk of this is owing to euro strength rather than USD weakness – more convincing for the weaker USD theme (at least within G3) if we see tepid US data today or worse.

EUR – the euro has put on fireworks despite the moribund ECB outlook. The technical situation is promising for bulls, as the consolidation off the prior 1.20-plus top was quite shallow relative to the magnitude of the rally off the lows early this year. A rally extension could target 1.2500.

JPY – historically, we look to the yen for the most volatility potential when risk-on, risk-off is afoot – but it appears we need a considerable wave of fear for the yen to really fire its engines – stay tuned. The breech of 113.00 in USDJPY sets at least some potential in motion.

GBP – sterling still at the low end versus the very strong euro, but not looking weak elsewhere as GBPUSD has bounced well off support – another sentiment test for the pound today on important UK data today – although it is still all about Brexit in the coming weeks into the EU summit mid-December.

CHF – the interest in EURCHF upside may fade if risk appetite weakens further – assuming the CHF retains some shadow of safe haven status. USDCHF needs to find support ahead of 0.9800 or it looks like curtains for the attempt to build a more notable uptrend.

AUD – yesterday’s positive news yielded to last night’s negative wage growth news and the AUD is the dog of the G7 currencies at the moment.

CAD – CAD certainly seems to have a reduced sensitivity to developments in energy markets as yesterday’s steep selloff failed to fire notable CAD volatility. CAD may post middle-ground performance here unless data today (home prices) or especially Friday (October CPI) provide any particularly large negative shocks.

NZD – kiwi finding few buyers in a nervous market and if risk aversion gets white hot, would expect general underperformance due to thin liquidity – though the currency appears to be getting the upper hand against the AUD as the last-ditch AUDNZD rally appears to have failed – a break of 1.1000 there could lead to a significant further retrenchment.

SEK – A tremendous rally in EURSEK points to a test of the 10.00 area and possibly beyond. It wasn’t just about the Swedish CPI yesterday missing to the downside either. An ugly drop in one of Sweden’s house price surveys (3% in October – worst in years) points to massive risk. On top of this, the Swedish financial regulator is calling for higher amortisation rates on Swedish housing data. This situation has the potential to snowball for Sweden and its banking sector and credit growth. The amortisation issue should have been imposed years ago… now it will only enhance downside risks.

NOK – NOK shares SEK’s structural risk in its housing market (perhaps the reason for the similar fate in weakening sharply yesterday) and the strong Euro saw EURNOK also blowing the top above recent range highs. An ugly adjustment lower in energy markets yesterday didn’t help. The prior major cycle high was near 9.75 all the way back in early 2016.

Upcoming Economic Calendar Highlights (all times GMT)

- 0930 – UK Oct. Jobless Claims Change

- 0930 – UK Sep. Average Weekly Earnings

- 0930 – UK Sep. Unemployment Rate

- 1000 – ECB’s Praet to Speak

- 1300 – UK BoE’s Broadent to Speak

- 1330 – Canada Oct. Home Price Index

- 1330 – US Oct. CPI (ex. 2.0% / 1.7% core)

- 1330 – US Nov. Empire Manufacturing

- 1330 – US Oct. Retail Sales

- 2110 – US Fed’s Rosengren (FOMC non-voter) to Speak

- 2345 – Canada BoC’s Wilkins to Speak