This article was submitted by Michael Stark, market analyst at Exness.

The main event so far this week in CFD markets is gold’s continuing surge upward to new record highs above $1,900. The latest swing high for the yellow metal was around $1,943 in the early morning GMT. This week’s critical event is the meeting of the Federal Open Market Committee on Wednesday night.

Central banks left policy on hold last week, with most continuing unprecedented quantitative easing. This week’s meeting of the Fed is likely to be key for gold and the dollar, with senior members of the FOMC likely to give more hints on the length of their programme of QE and the possible outlook for recovery later in this quarter.

July’s Ifo business climate from Germany this morning beat expectations slightly at 90.5. This positive release could drive momentum upward for the euro in some of its pairs today.

Flash GDP growth from Germany and the USA are some of the most important regular data coming up this week. Other major economies in the eurozone release GDP growth on Friday morning GMT.

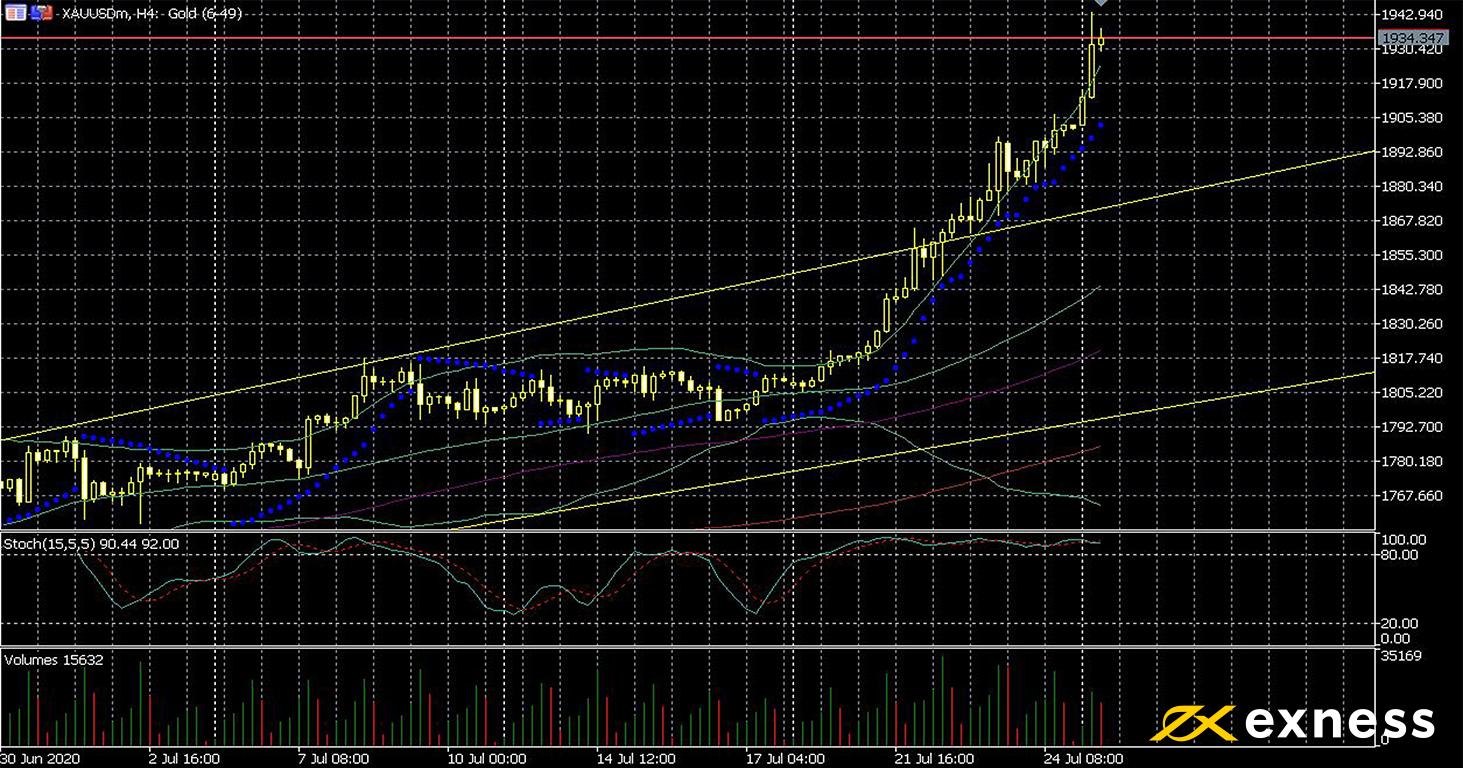

Gold-dollar, four-hour

Gold has surged up since last week and decisively broken resistance around the 38.2% zone of the Fibonacci fan. Extensive printing of money around the world, rumours of a second wave of covid-19 and record low interest rates in most cases have driven very high demand for the metal.

Given that overbought based on both Bollinger Bands (50, 0, 2) and the slow stochastic (15, 5, 5) has persisted for more than 20 consecutive periods now, it seems difficult to predict when a retracement might occur. One possibility in this situation is that a clear retracement does not occur and that price instead consolidates after the large gains; this could provide a point of entry for new buyers. On the other hand, we can probably expect activity to decrease tomorrow and on Wednesday as many traders will want to wait for the news from the Fed this week before committing themselves.

Friday 31 July, 12.30 GMT: American personal income (June) – consensus -0.5%, previous -4.2%

Friday 31 July, 12.30 GMT: American personal spending (June) – consensus 5.5%, previous 8.2%

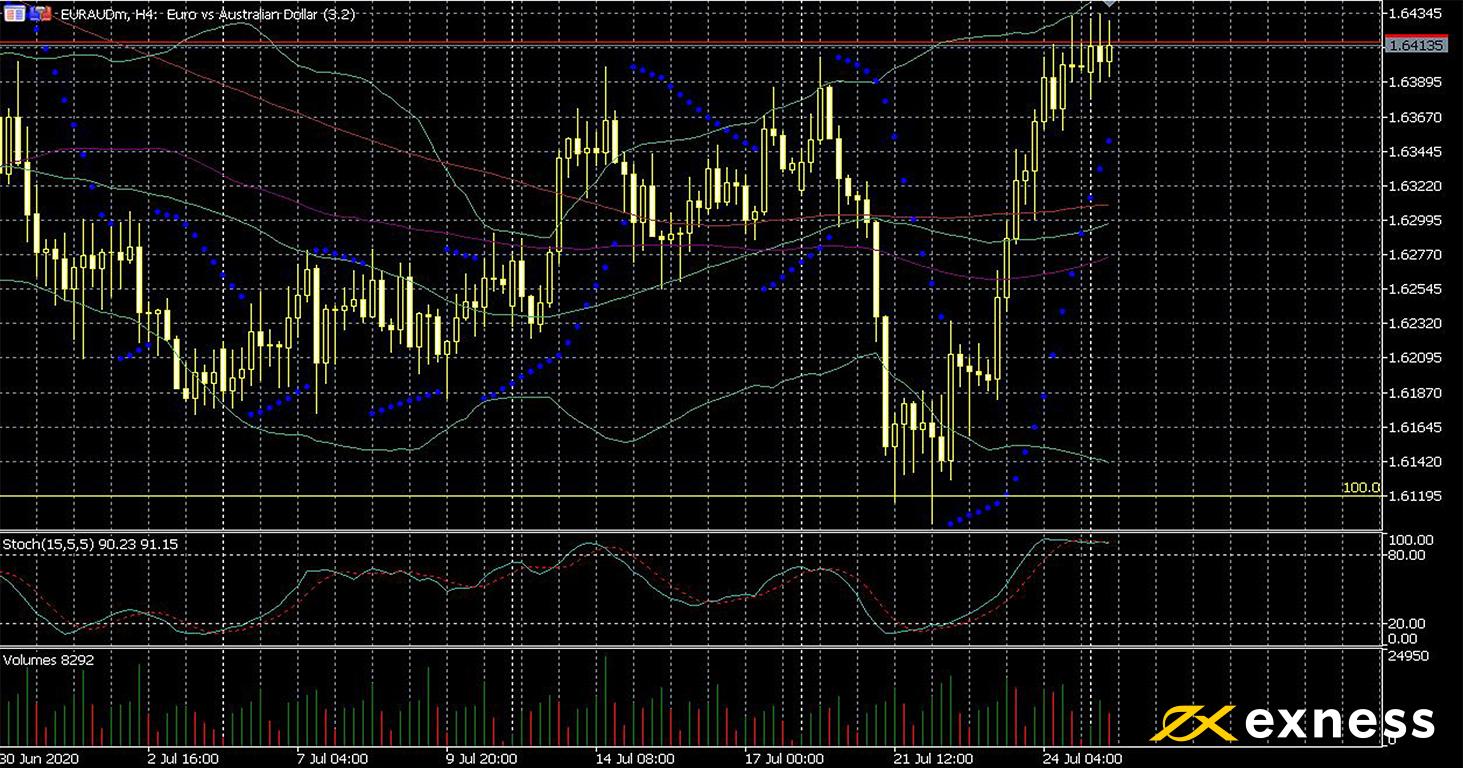

Euro-Aussie dollar, four-hour

A convergence of fundamental and technical factors has driven EURAUD’s bounce since the middle of last week. More new cases in China – the highest since April over the weekend – have hit sentiment and weakened the outlook for Australian exports. Meanwhile leaders in the eurozone agreed last week to a historic aid package for struggling Mediterranean economies.

The 100% Fibonacci retracement zone, i.e. full retracement of the euro’s gains in Q1, has now been established as a strong support. Unless the tone of the news suddenly turns very positive for Australia, we can expect another bounce if this area is tested again. Moving averages are somewhat mixed here, with the 50 SMA from Bands having recently completed a golden cross of the 100 but remaining below the 200. German GDP data is clearly the most important release for the euro-Aussie dollar this week, but Australian inflation early on Wednesday morning is also in view.

Key data this week

Bold indicates the most important releases for this symbol.

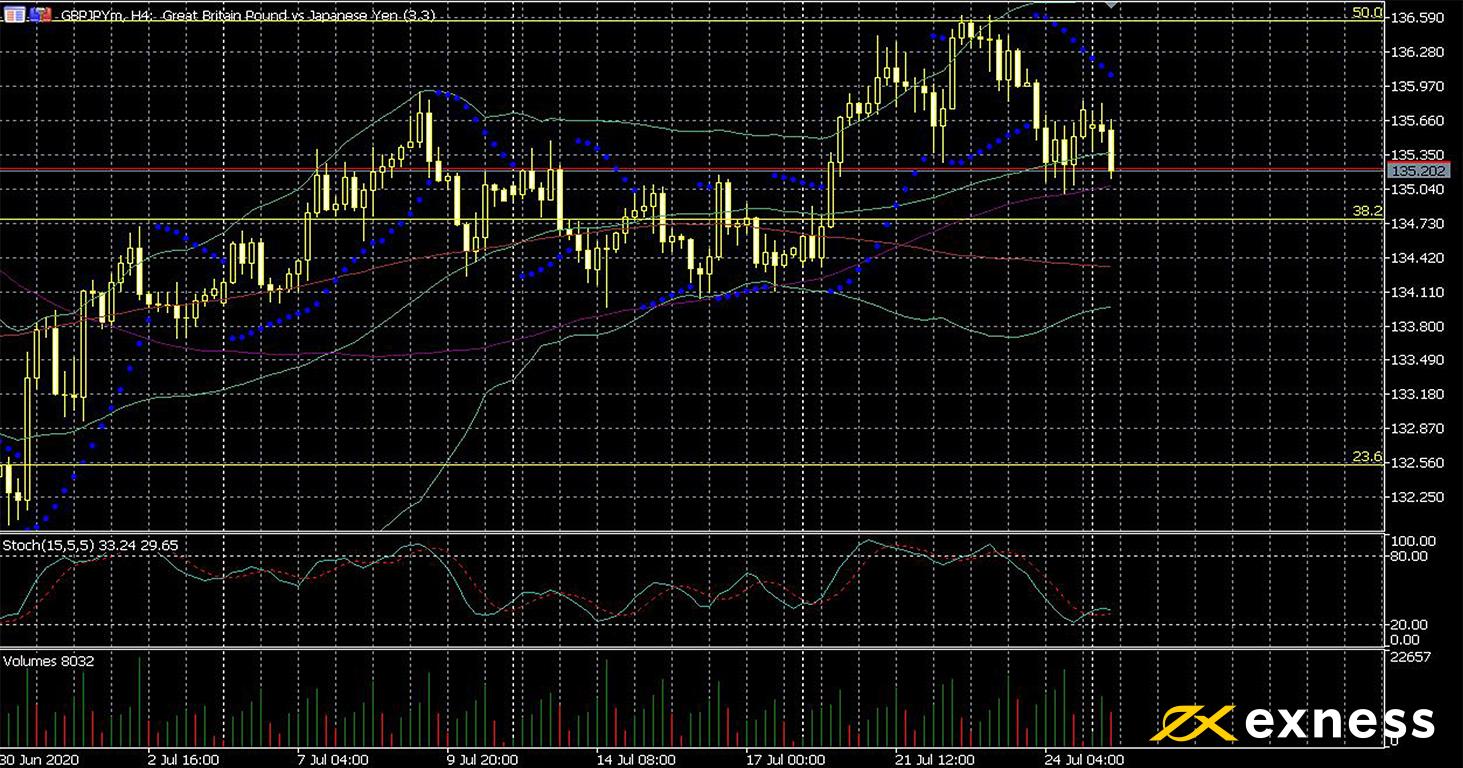

GBPJPY has yet to interact very clearly with the latest change in sentiment towards negative although it has retreated from its six-week high of 136.60 since last week. Fundamentals overall seem to favour the yen, but the relative recovery from the coronavirus in the UK has overshadowed some negative factors. Once markets again begin to price in a minimal at best British-EU trade deal, the pound seems to have some way to fall against most currencies.

The four-hour chart of pound-yen still shows a positive technical picture, though. The 50, 100 and 200 SMAs are successively above each other and below price, with the 100 having golden crossed the 200 last Tuesday morning GMT. Price is currently testing the 50 SMA with no real signs of selling strength from price action or volumes just yet. This week’s key data for GBPJPY are mostly Japanese, with the main event being consumer confidence on Friday morning.

Key data this week

Bold indicates the most important release for this symbol.