Global brokerage Saxo Bank today released their Q1 2017 Quarterly Outlook. The 22-page report includes topics including Brexit, Dollar outlook, US, EU central bank forecasts, China currency policy and more with FX forecasts for CHF, AUD, CAD, NOK, SEK and emerging markets.

Check out a snippet below of the first article by Steen Jakobsen, Saxo Bank’s Chief Economist and CIO, the download link to the full report you can find here (PDF).

Steen Jakobsen is Saxo Bank’s Chief Economist and CIO

The 1970s all over again

The direction of the US dollar is the key question for 2017 because a currency that is up 20% over the past year will trigger a reaction, and the incoming Trump administration can be expected to jettison the more than 20-year-old dogma that a strong dollar is in the US’ interest.

Welcome to 2017 and Trump-mania, a world where tweets set the agenda randomly across the US and where being unorthodox is the new black.

For all the guess work we can do on Donald Trump and his new policies, the key questions remain the same:

What is the general direction of the US dollar?

Where is China’s currency and growth headed in 2017?

Is the double whammy of Brexit/Trump the end of a cycle, or the beginning of something new?

What’s the most important question of the three? That’s the direction of the US dollar. We have such a simplified economic world, or globalised market, that dollar represents in excess of 75% of all transactions globally.

So, when the US dollar is up over 20% year-on-year — as it is now — there will be a “reaction” to the “action”. This reaction will be a considerable slowdown in growth in the US driven by higher-than-expected interest rates (which reduce potential growth) and indirectly also by reducing global growth as the heavy burden of US-dominated debt hurts emerging markets’ ability to repay their excessive loans in dollars.

Foreign banks have lent $3.6 trillion to companies in emerging markets, and roughly 50% of that amount is to China, so questions one and two are interlinked.

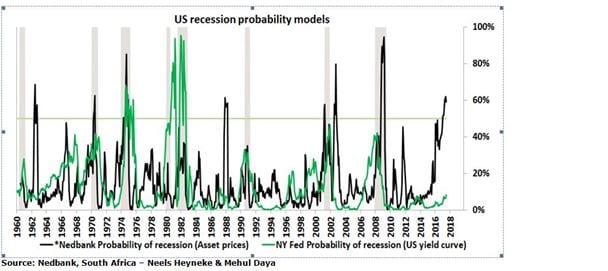

The risk of recession is increasing. My good friends at NedBank, South Africa, Neels Heyneke and Mehul Daya, have the best recession model I have seen, combining monetary conditions with fundamentals. The present reading: 60% probability of recession against a market consensus of only 5-8%.

US recession looking more than likely? Source: Nedbank, South Africa – Neels Heyneke and Mehul Daya

We can’t ignore the voices of populism in the US, but also shouldn’t overlook them in Europe in an election year. But rest assured, this is the end of a cycle, not a new beginning. The world will not move forward on an agenda of closed borders, anti-globalisation and trade restrictions, and against competition, but nevertheless these forces need to be respected, especially as we see a change of leadership in the global arena…

Trump taking the US “back home” on trade, overseas troops, Nato and reversing a China policy in place since the 1970s will have consequences. German chancellor Angela Merkel is now the de facto leader of the developed world, a position she never wanted and feels uncomfortable in during an election year for Germany. China will fill any vacuum left behind by the US changing course.

The Chinese leadership seems more “open” than ever before on foreign policy and investment, partly out of opportunity and partly by virtue of a desperate need to draw attention away from ever rising domestic debt and capital outflows.

China will most likely continue to weaken the CNY and CNH to the tune of 5-10% — probably gradually, but, if forced, also through another “devaluation” as retaliation for US policy…

To check out the full report click here (PDF).