European shares generally started the week on the front foot after positive Chinese data in the early morning. Official PMI for both manufacturing and services in China showed expansion as the economy continues to recover from the initial wave of covid-19. American shares had also gained on Thursday and Friday as continuing heavy QE remains likely. This preview of weekly forex data takes a look at the releases to affect USDCAD, XAUUSD and EURAUD.

News from central banks was dominated last week by the conference in Jackson Hole, Wyoming, USA which this year took place virtually. The Fed’s chair Jerome Powell’s comments indicated increased tolerance of higher than average inflation and accommodative monetary policy for longer. Meanwhile on Friday Andrew Bailey the Governor of the Bank of England asserted ‘We are not out of firepower by any means’, seemingly opening the door to more easing in the UK over the next few months. However, Dr Bailey didn’t comment on the outlook for Britain’s economy.

This week’s main event among central banks is the meeting of the Reserve Bank of Australia tomorrow morning. The cash rate will almost certainly be left on hold at 0.25% but what Philip Lowe and other senior central bankers say in reaction to Jackson Hole is likely to be very important for the Australian dollar this week.

The most important regular data this week include tomorrow’s Caixin manufacturing PMI, Wednesday’s Australian GDP growth, Thursday’s balance of trade from Australia, Canada and the USA and of course the NFP on Friday. It’s a pretty active week for currencies like the Aussie dollar so some volatility for AUD can be expected around the key releases.

US dollar-Canadian dollar, four-hour

The greenback continued to lose strength against most major currencies last week in the aftermath of Dr Powell’s comments on Thursday afternoon which were generally perceived as being dovish. With oil also set for its fourth consecutive month of gains, the loonie has had considerable tailwinds recently. One of the key questions to affect USDCAD’s fundamentals over the next few months is how the Bank of Canada will change its current monetary policy regarding quantitative easing.

Dollar-loonie’s current downtrend has been active since early April and doesn’t show any signs of stopping yet. Having recently passed the 100% Fibonacci retracement area, i.e. full retracement of all the greenback’s gains during the first phase of the crisis, there looks like plenty more room for losses. The main concern for new sellers then is oversold from the slow stochastic and Bollinger Bands.

This week’s key event for this symbol and indeed for most markets is the NFP. The consensus estimate at the time of writing is about 1.43 million against last month’s 1.76 million; Canadian employment data also come out at 12.30 GMT on Friday. Balance of trade on Thursday from both Canada and the USA is also likely to be important for USDCAD.

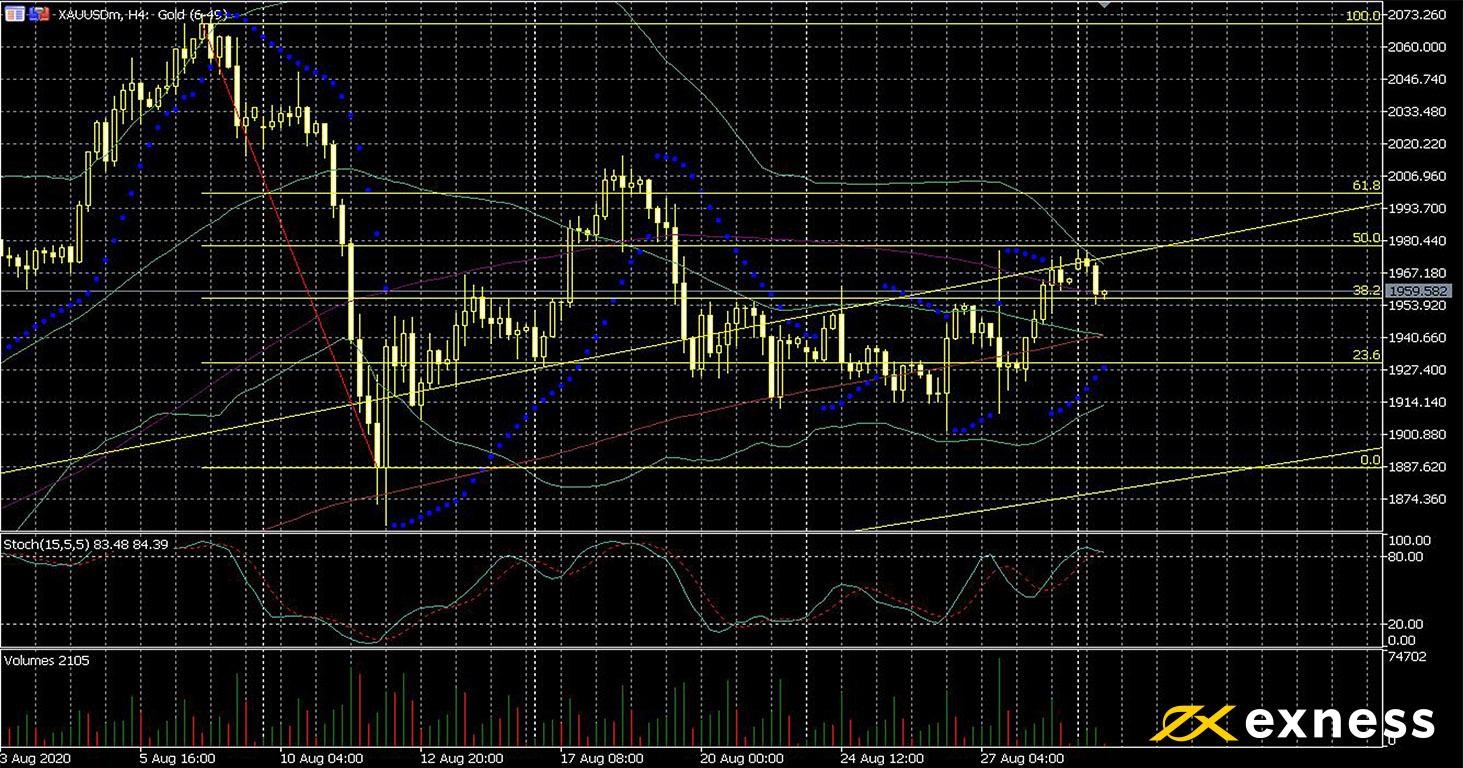

Gold’s volatility has increased again since the second half of last week after very strong initial gains during Jerome Powell’s opening comments at Jackson Hole. The likelihood of at least somewhat higher inflation is a positive for the metal, as is of course ‘lower for longer’ when it comes to rates. The dollar also lost strength last week around Dr Powell’s comments and generally before that. ‘Cash is trash’ is set to remain the dominant narrative for the foreseeable future and gold in addition to shares has recently started to receive more inflows of new liquidity created by central banks.

From a technical perspective, the pieces seem to be there for XAUUSD to continue upward once again, although traders should still be aware of the potential for sudden selloffs. The impending death cross of the 50 and 200 SMAs can be ignored in the context unless price moves back down below the former for a significant time. However, the slow stochastic (15, 5, 5) shows a clear overbought signal at about 85. American balance of trade followed by the NFP are this week’s crucial releases; negative results could lead to a retest of $2,000.

Key data this week

Bold indicates the most important releases for this symbol.

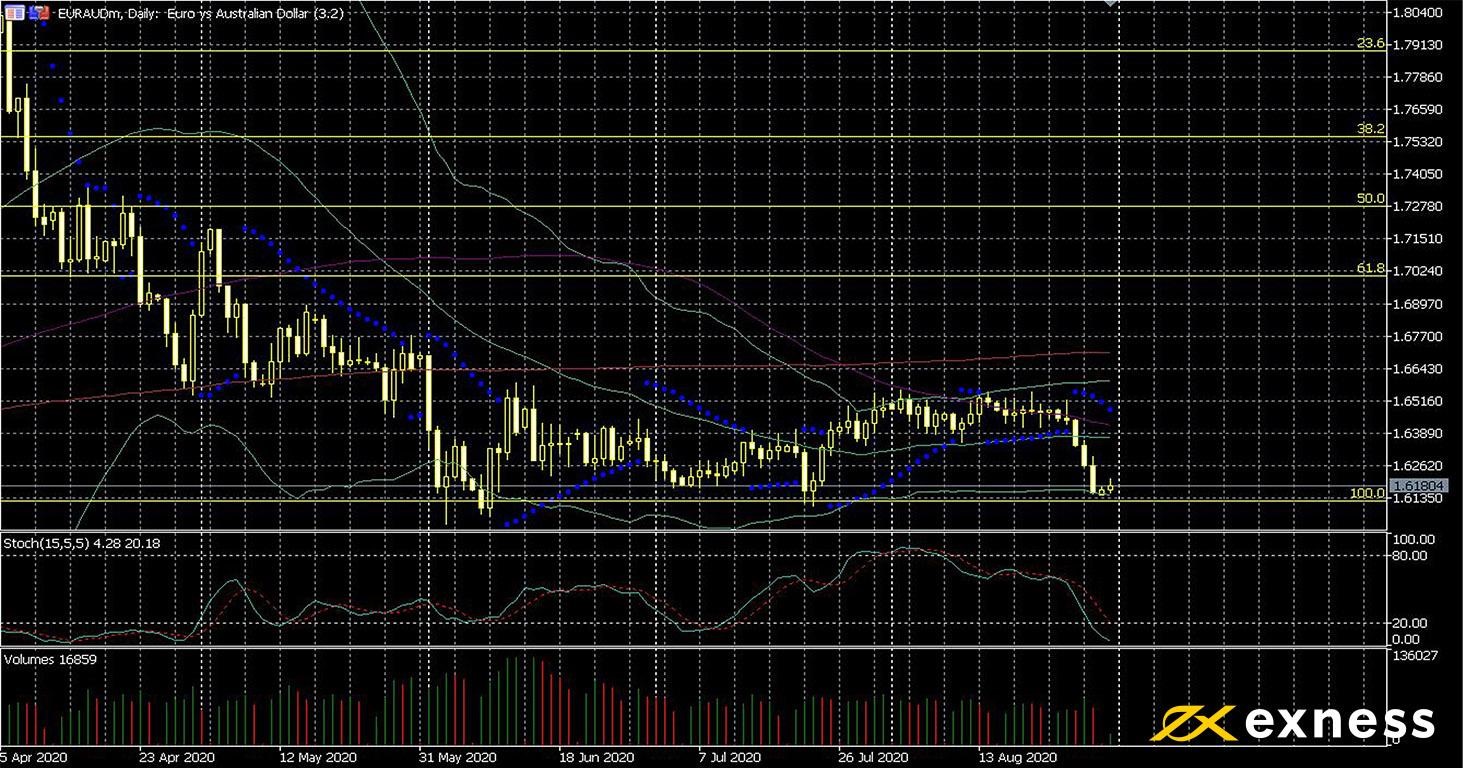

Euro-Aussie dollar moved back down again late last week amid dovishness at Jackson Hole, even retesting the 100% Fibonacci retracement area briefly. This comes despite negative fundamentals for AUD: Australia’s fiscal support is now among the highest in the world as a percentage of GDP, around 13%, behind only New Zealand and Singapore by this measure. At the same time, the RBA is one of the least supportive central banks, having ruled out negative rates and buying the least government debt relative to GDP of all major advanced economies.

Australia’s critical trade relationship with China has also continued to deteriorate sharply over the last few weeks. Exports of meat, cheese and wine all face increasing hurdles, and iron ore could be next. With around 80% of Australia’s exports of ore going to China, this sector is likely to be the next key point of contention in the current diplomatic souring.

Based on the situation today, it looks like a triple bottom. Each time the 100% Fibo around A$1.61 has been tested, there’s been a fairly quick bounce from oversold. The deviations of Bollinger Bands (50, 0, 2) have also contracted significantly since the end of July, so any breakout coming should logically be to the upside unless there’s a sudden turn in the tone of fundamentals. A lot depends on what the RBA says and doesn’t say tomorrow, but key Australian data later in the week could also drive some losses for AUD unless they’re surprisingly positive.

Key data this week

Bold indicates the most important releases for this symbol.

Monday 31 August, 22.30 GMT: Ai Group manufacturing index (August) – consensus 52.9, previous 53.5

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.