This article was submitted by Michael Stark, market analyst at Exness.

Risk-on instruments have generally started the week positively amid a flurry of corporate deal-making. Increasing hopes of an effective vaccine against covid-19 being rolled out over the next few months have also helped sentiment. Today’s preview of weekly forex data takes a closer look at EURJPY, XAUUSD and GBPNZD.

There wasn’t much activity among central banks last week apart from the ECB’s meeting. This didn’t really surprise markets, although euro-dollar and other pairs with the common currency were unstable in the short term last Thursday. This week’s most important meetings of central banks are the Federal Open Market Committee on Wednesday and the Bank of England on Thursday. However, the Bank of Japan, the South African Reserve Bank, the Central Bank of the Russian Federation and the National Bank of Poland will also meet this week. The focus at each of these is likely to be on quantitative easing and the outlooks for economies in much the same way as over the last couple of months.

The most important regular data in forex markets this week are claimant count change this morning GMT and British inflation tomorrow morning. The consensus estimate for the former currently stands at 100,000. Other key releases include Japanese balance of trade late on Wednesday night, Canadian and Japanese inflation, New Zealand’s GDP and ZEW sentiment. It’s a fairly active week of data and we can probably expect stock markets to be moving quite strongly.

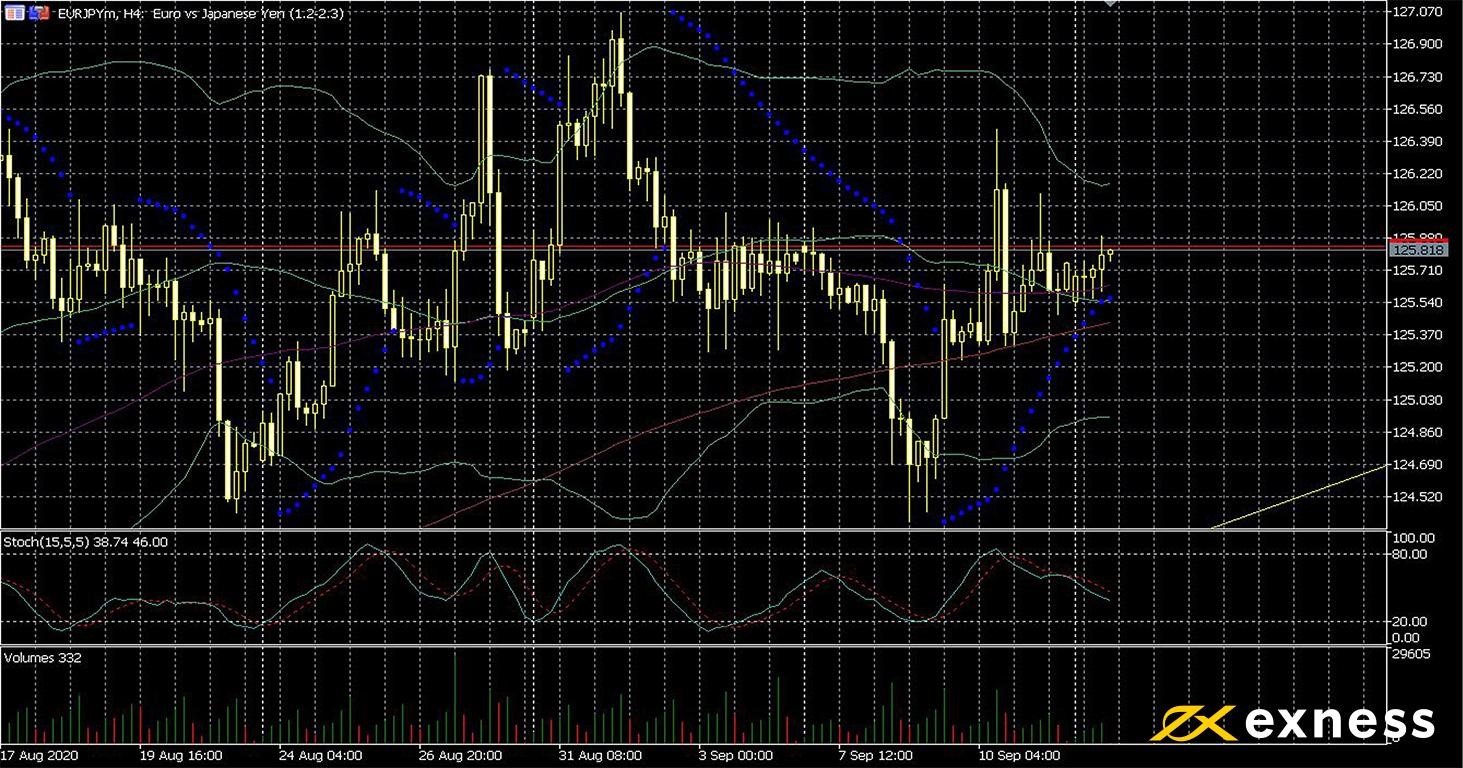

Euro-yen, four-hour

While the yen was up somewhat earlier today against the dollar as in the aftermath of Yoshihide Suga’s election to replace Shinzo Abe as Prime Minister of Japan, euro-yen has been pretty static. Neither the eurozone as a whole nor Japan are among the worst-affected currencies in terms of the coronavirus but both continue to struggle to contain cases and encourage economic growth. Industrial data this morning from both the eurozone and Japan were slightly better than expected.

EURJPY has moved quite far beyond its daily Fibonacci fan, with the 38.8% area only just visible in the bottom right corner of the chart. This combined with what seems to be weaker upward momentum last week might suggest a retracement to come over the next couple of weeks; the 50 SMA from Bands has also recently death-crossed the 100 again.

This week’s most important release for this symbol is likely to be today’s ZEW economic sentiment from Germany. However, balance of trade from Japan tonight and the eurozone on Wednesday could also provoke reactions on the chart. Finally, Thursday night’s key figure is Japanese inflation.

Friday 18 September, 6.00 GMT: German PPI (August) – consensus -0.1%, previous 0.2%

Gold-dollar, four-hour

Gold has not been particularly active so far today but continues to show some signs of technical strength. The environment of near-zero rates and a relatively weak dollar have led to the area of $1,915 being established as a fairly strong support. The 50 SMA is also in view as a support since the second half of last week, so gains might be expected based on both technicals and fundamentals in the runup to the Fed in the absence of any other significant data.

Wednesday’s meeting probably won’t really surprise anybody but traders will still be looking for more clues on the effects of the Fed’s new inflation-targetting strategy. As usual, plans for QE will also be studied closely. Retail sales a few hours before the Fed probably won’t have much effect on XAUUSD in the context.

Key data this week

Bold indicates the most important event for this symbol.

Gains for the pound in most of its pairs including GBPNZD in July and August came as many participants in markets discounted negative predictions for the then-upcoming round of Brexit talks and focussed more on the reopening of the British economy and generally strong industrial and manufacturing data (considering the circumstances). Now though with exchanges of threats between the UK and the EU and increasing expectations that the UK might just pull out of the ongoing trade talks, the pound has taken a hit.

The 100% Fibonacci retracement area based on July and August’s gains seems to be a strong technical zone which might trigger another bounce if retested. More losses from here don’t seem to be especially likely given also the clear oversold signal from the slow stochastic (15, 5, 5), which at about 8 today is close to the minimum. With claimant count change, a meeting of the BoE and Kiwi GDP data this week, though, there’s a lot riding on economic numbers, more so than charts.

Whether the British government actually has some sort of hidden master plan to conclude the trade talks successfully is a question, but given the number of u-turns over the summer it’s probably unwise to assume anything much at this stage. Rumours could move out of view somewhat this week given the number of critical releases affecting GBPNZD, most prominently claimant count change today.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.