This morning’s most important data so far were Chinese annual exports which were up 9.5%, significantly higher than the consensus for about 7% and the previous 7.2%. While demand around the world has improved as economies continue to reopen gradually, Chinese imports declined 2.1% against the expectation for negligible growth. This preview of weekly forex data takes a closer look at the releases to affect EURCAD, GBPUSD and UKOIL.

The main events in monetary policy this week are the meetings of the Bank of Canada and the European Central Bank. As has been customary in recent months, no change is expected in either case to rates, but what central bankers say about ongoing quantitative easing and the outlook for economic recovery over the next few months is likely to be very important for the euro and the Canadian dollar.

Regular data this week is dominated by balance of trade from Germany and the UK plus inflation in China and the USA. Traders will also be monitoring GDP data tomorrow from Japan, the eurozone and South Africa.

Euro-Canadian dollar, four-hour

The euro has recovered somewhat against the loonie since the second half of last week although volatility has remained fairly high. Oil’s losses have generated headwinds for CAD, and Canadian employment change on Friday was somewhat weaker than expected at 245,800. However, the economic situation in the eurozone is also difficult, with the return to growth in most EU countries slow and stuttering so far, so fundamentals seem to be fairly balanced on both sides of this pair.

The 61.8% Fibonacci retracement area could be a zone of support, but a fairly wide one given the move down to C$1.544 last week. Moving averages continue to give a sell signal, with most recent gains capped by the 50 SMA from Bands. Buying volume has generally been higher than selling in August despite the ongoing downtrend – some traders might have been preparing for losses by oil driving the loonie down.

This week’s most important events for EURCAD are the meeting of the BoC on Wednesday and the ECB on Thursday. No change to rates is likely in either case, but comments on QE and its possible expansion are key. Particularly important is how central bankers might respond to the changes in the Fed’s policy confirmed at the recent virtual Jackson Hole symposium. In addition to monetary policy, the euro is likely to be active tomorrow around German balance of trade and the eurozone’s GDP data.

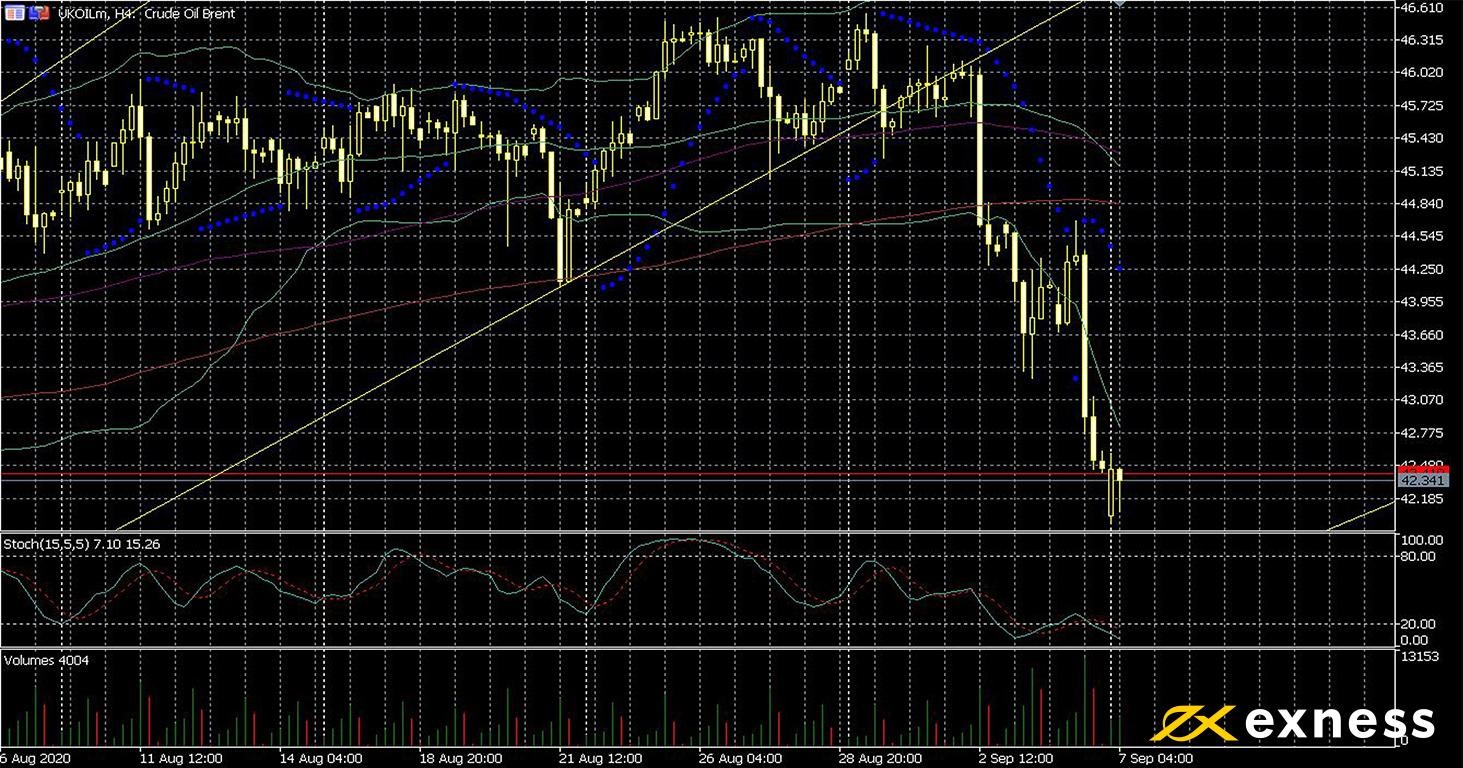

Oil’s relatively sharp decline since the middle of last week hasn’t shown any signs of stopping today. Weaker Chinese imports are a negative for the commodity, as is Saudi Arabia’s cut to the official selling price of Arab light crude to Asia yesterday. Trade tensions between the USA and China continue to rumble, with the latest rumour on this front being that the former is considering export restrictions on Semiconductor Manufacturing International Corp.

From a technical perspective, it’s probably still too early to hail a breakout downward. The daily Fibonacci fan remains active unless there’s a clear break below the 61.8%, which at the moment doesn’t seem favourable. Given that crude oil is usually one of the most volatile of the widely traded CFD instruments, the latest movement might just be a return to ‘normal’ after a fairly long stretch of calm. High buying volume despite losses indicates traders’ inclination to buy the dips, while the clear oversold conditions mean that a bounce seems likely this week unless the regular data are particularly negative.

This week’s data include the API and EIA’s weekly crude stocks, both unusually taking place a day late because of the American holiday, plus Baker Hughes’ rig count as usual on Friday. Apart from the typical releases, though, Saudi activity and the outlook for Chinese manufacturing are likely to remain in view.

Key data this week

Bold indicates the most important release for this symbol.

Wednesday 9 September, 20.30 GMT: API crude oil stock change (4 September) – previous -6.36 million

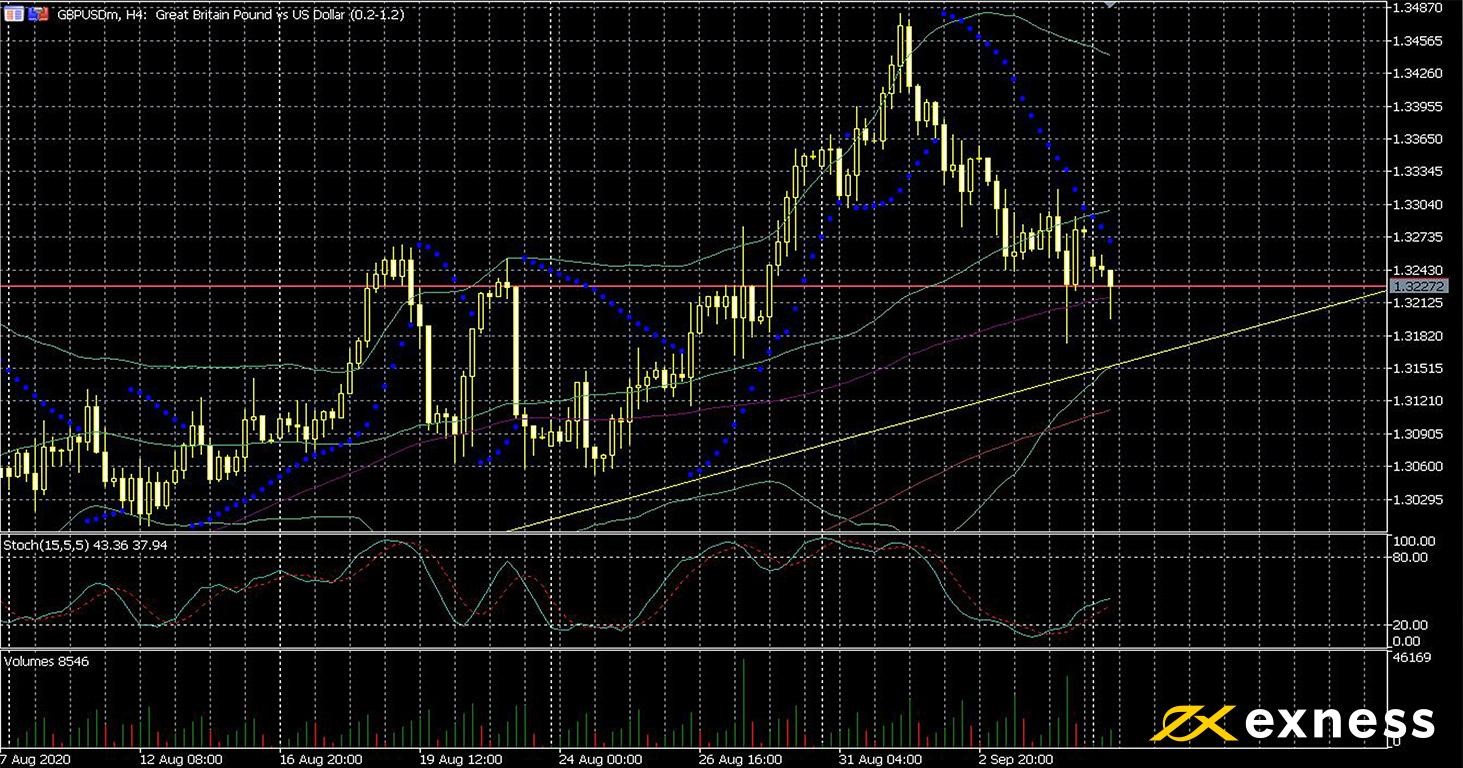

The pound has faced a bit of pressure against the US dollar since last week after rampant gains over the previous few weeks. Reports that the UK might backtrack on previous commitments in Northern Ireland related to state aid and customs have caused some nervousness, but the main issue coming back to the forefront is that the UK might now be as far away as ever from a trade deal with the EU at the end of the transition period. The second-last round (for now) of Brexit talks is due to start tomorrow, but nobody seems to expect a sudden breakthrough at this stage.

TA still paints a positive picture for cable although price has moved below the 50 SMA from Bands and is now testing the 100 SMA. The next key zone to the downside is the 38.2% area from the daily Fibonacci fan: a move below this might spur momentum downward to retest $1.30. With the dollar still experiencing a strong selloff in most of its pairs, though, there is certainly scope for cable to move back up to last week’s high depending on this week’s economic releases.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.