This article was submitted by Michael Stark, market analyst at Exness.

Cyclical instruments like indices, many shares and commodities have rebounded aggressively so far this week amid the dollar’s retreat and increasing expectations that the pace of monetary tightening could slow down in the next few months. This midweek preview of data looks at XAUUSD and EURUSD ahead of the crucial NFP on Friday.

Thailand and Mexico’s central banks both raised their rates last week, while on Tuesday morning of this week the Reserve Bank of Australia also hiked but by less than expected. The consensus had been for a double hike to 2.85%; however, the RBA delivered only a single hike to 2.6% and noted in its statement that the labour market is strong and that future hikes will depend on data. The Australian dollar has made some losses against most other major currencies in the immediate aftermath.

The outlook for American monetary policy has been more ambiguous since last week. About two-thirds of participants are pricing in another triple hike on 2 November according to CME FedWatch Tool, but the Fed surely has to stop somewhere. The UN’s Conference on Trade and Development directly urged the Fed to stop hiking in its report published on Monday, while it seems difficult for the American economy with moderately high levels of debt to withstand rates much above 4% for very long.

This week’s critical regular release is the US job report on Friday which includes the NFP, rate of unemployment and average hourly earnings. Canada’s monthly job data are also due at 12:30 GMT on Friday. Participants will consider balance of trade from Germany, Canada, the USA and Australia this week as well. This isn’t a huge week of data apart from US jobs but the dramatic movements in many markets over the last few days, especially cyclical instruments, would suggest caution unless one’s tolerance for risk is particularly high.

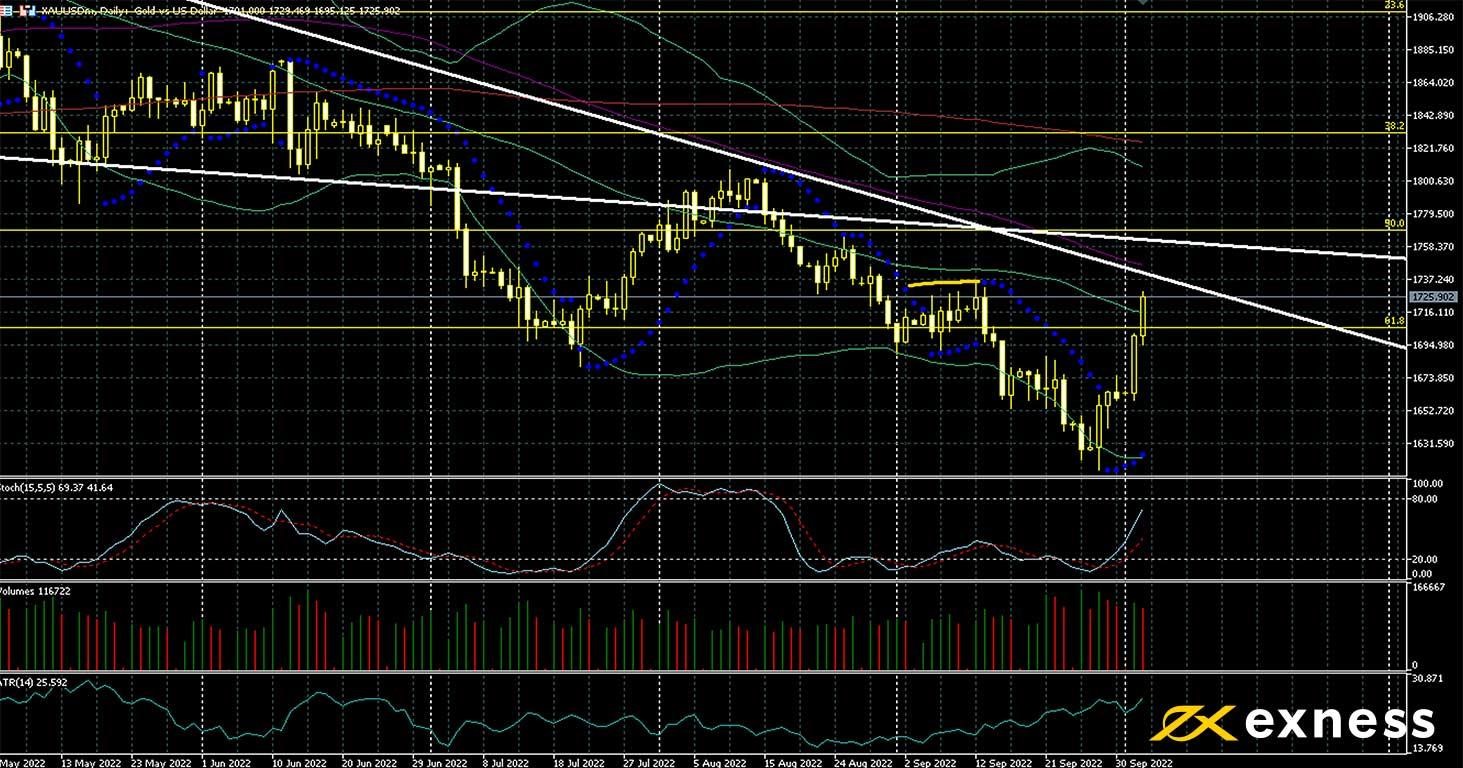

Gold-dollar, daily

Gold has bounced with exceptional strength since the end of September. The primary fundamental reason for this is the increasing expectation that, in the long-term, the Fed will be less aggressive in tightening policy given that the outlook for the American economy has worsened significantly in the last few months. ISM manufacturing PMI has declined to its lowest since May 2020 and there are clear indications that the labour market in the USA is cooling off based on open jobs and layoffs.

Buying here with the price not yet having closed above the 50 SMA and the two main downward trendlines not far above would traditionally be considered very unlikely to succeed. However, the duration of the downtrend might support ongoing gains that could be exploited if a new entrant to buy waited for a retracement lower or used a buy limit. All indicators plus obviously price action demonstrate the really unusual liveliness of the current upward movement, so it seems likely to continue to some degree up to Friday’s NFP barring some major event.

The magnitude of the current bounce suggests considerable institutional involvement, which is practically unknown in the week before a major event such as the NFP. That suggests in turn that the reaction to the job report could also be extremely strong, so the most conventional wisdom of waiting for the dust to settle after a major release before possibly acting seems to have some value this week.

12:30 GMT: American annual average hourly earnings (September) – consensus 5.1%, previous 5.2%

12:30 GMT: American monthly average hourly earnings (September) – consensus 0.3%, previous 0.3%

Euro-dollar, daily

Much like gold, the euro’s move up against the US dollar has been very energetic since last week. Eurozone-wide flash annual non-core inflation last week came in at a full 10%, a fresh record high and significantly higher than the consensus of 10%. National inflation in Spain and France was lower than expected, but Italian inflation increased more than the consensus and Germany’s surged to 10% as well.

Dr Lagarde and other members of the ECB’s executive board have commented on their commitment to stability of prices in recent days regardless of the risk of a significant recession. Various national banks in the eurozone have called for another triple hike later this month.

The technical situation looks quite positive for this symbol with a huge spike in buying volume around 26 September low and daily ATR close to the post-Covid peak. The 50-day moving average from Bands is still being tested, so a retracement lower might be favourable before a possible breakout upward depending on the NFP and any further comments from the executive board or the FOMC. As above, jumping in very quickly after Friday’s releases would be extremely risky under the circumstances.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.