Adam Vettese, UK Market Analyst at eToro, has provided his daily commentary on traditional and crypto markets for November 6, 2020.

US stock futures have stalled after rallying strongly this week during the aftermath of the US election. As Trump prepares a legal challenge we could well see some volatility in the days to come.

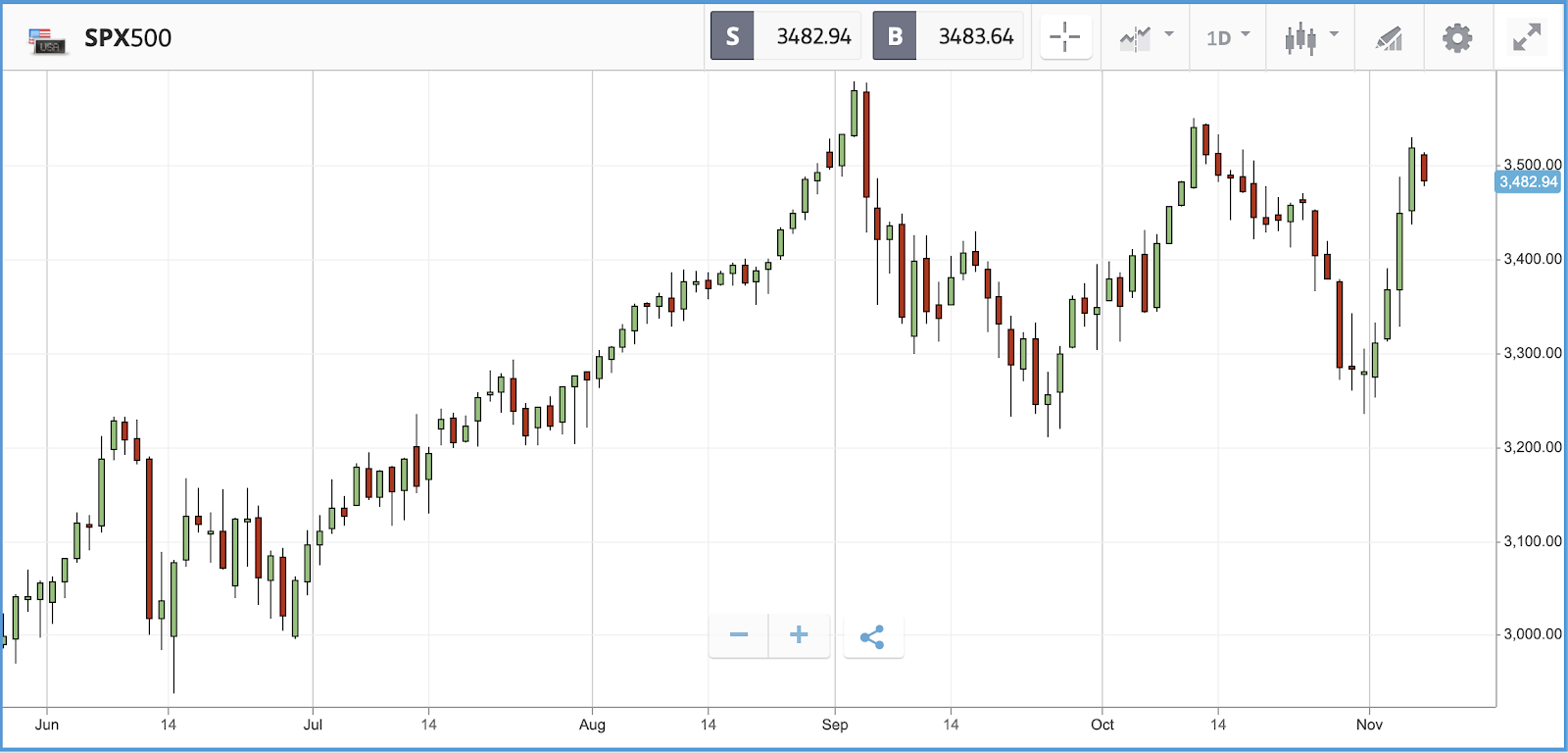

Markets continued their election-induced rally yesterday, as Joe Biden edged towards the presidency in a nail-biting, drawn out race. Once again technology names surged, with the S&P 500’s information technology sector up 3.1%. Thursday’s rally meant the S&P 500 has now posted 1% plus gains for four days straight. According to Bloomberg reporter Sarah Ponczek, that has only happened three other times in the index’s history, with those all happening in the Seventies and Eighties. Since the start of the week, the S&P is up by more than 7%.

Yesterday in the UK, the Bank of England’s (BoE) Monetary Policy Committee kept interest rates set at 0.1% but the central bank announced a new round of bond buying as England locks down once more. BoE Governor Andrew Bailey, vowed to do “everything we can” to support the economy, and committed to another £150 billion of UK government bond purchases.

Qualcomm surges on 5G optimism

Beyond technology stocks, 10 of the S&P 500’s 11 sectors were in the green yesterday, with the materials, consumer discretionary, financials and industrials sectors all up by more than 2%. All three of the major US stock indices gained 2% or more, with the Nasdaq Composite the biggest winner at +2.6%. Chipmakers Qualcomm and Micron helped the Nasdaq higher, gaining 12.8% and 5% respectively after Qualcomm delivered an expectation beating earnings quarter. “We believe the stars are aligning for Qualcomm, with a multi-year global 5G cycle starting to ramp,” Bank of America analysts wrote in a Thursday note, according to CNBC.

In other earnings news, Uber’s share price fell slightly as it reported quarterly earnings, after its Wednesday surge on the back of a victory in its California battle to avoid classifying workers as employees. In Q3, the firm said its food delivery business was still outperforming its ride business, with overall revenue down 18% to $3.1bn year-over-year.

- S&P 500: +2% Thursday, +8.7% YTD

- Dow Jones Industrial Average: +2% Thursday, -0.5% YTD

- Nasdaq Composite: +2.6% Thursday, +32.5% YTD

UK stocks react positively to BoE stimulus news

The bond-buying boost announced by the Bank of England yesterday was bigger than expected and, along with Joe Biden’s continued progress towards the US presidency, that helped to buoy UK shares. The bank said that announcing further bond purchases now “should support the economy and help to ensure the unavoidable near-term slowdown in activity was not amplified by a tightening in monetary conditions.” In addition, the central bank said that it now expects the UK economy to not reach its pre-pandemic size until Q2 2022.

On Thursday, the FTSE 100 ended the day 0.4% higher, while the FTSE 250 gained 0.7%. The FTSE 100 was led by RSA Insurance group, which jumped by more than 40% after receiving a takeover offer. At the bottom of the index was Rolls-Royce, which fell double digits after announcing another round of job cuts.

- FTSE 100: +0.4% Thursday, -21.7% YTD

- FTSE 250: +0.7% Thursday, -18.1% YTD