The dollar is starting the week on the backfoot, reaching a new multi-week low against the euro. Despite last week’s publication of economic data that came up well above expectations, providing evidence of the strength of the American economic recovery, the inflationary fears that led to rising treasury yields and dominated the trading agenda during the month of March have all but vanished from the horizon of investors.

The Fed has successfully passed the message that any spike in prices is likely to be transitory and therefore the central bank will not accelerate the timing of the tapering.

This stance has reassured investors, leading to a drop in treasury yields and causing dollar weakness. At the same time, on the other side of the Atlantic prospects of a more efficient management of the ongoing health crisis during Q2 are providing support to the single currency. With such a dynamic in place there may be scope for further euro gains that may test the $1.22 resistance line, which was last touched in January, before inflation fears started dominating the markets narrative.

We are picking up where we left off last week with gold: the precious metal is consolidating its recovery as the EUR/USD exchange rate jumped above 1.20. US yields are continuing to weaken and this scenario is supportive for bullion, as the negative correlation with the greenback remains in place. After surpassing $1,750, gold is continuing to gather momentum. Bullion is also showing its strength and its resilience to any kind of market shock, at a time when bitcoin is confirming, once again, to still be a young and not yet fully mature market, with strong rallies followed by sharp corrections.

Carlo Alberto De Casa – Chief analyst, ActivTrades

EUROPEAN SHARES

European benchmarks drifted on Monday, mostly in green territory but with lower volumes than usual. Despite last night’s directional session in Asia, where Chinese shares strongly outperformed due to reassuring news regarding Huarong Asset Management Co., investors are now bracing for this week’s new batch of corporate results. Indeed, most of them expect solid earnings this week, as a confirmation of the strong economic data recently posted by the top economies. That said, any setback in corporate reports may dent market sentiment on a short-to-mid-term basis. Meanwhile, the lack of significant data release today is likely to turn the current trading session into a technical one, during which key levels are likely to be tested.

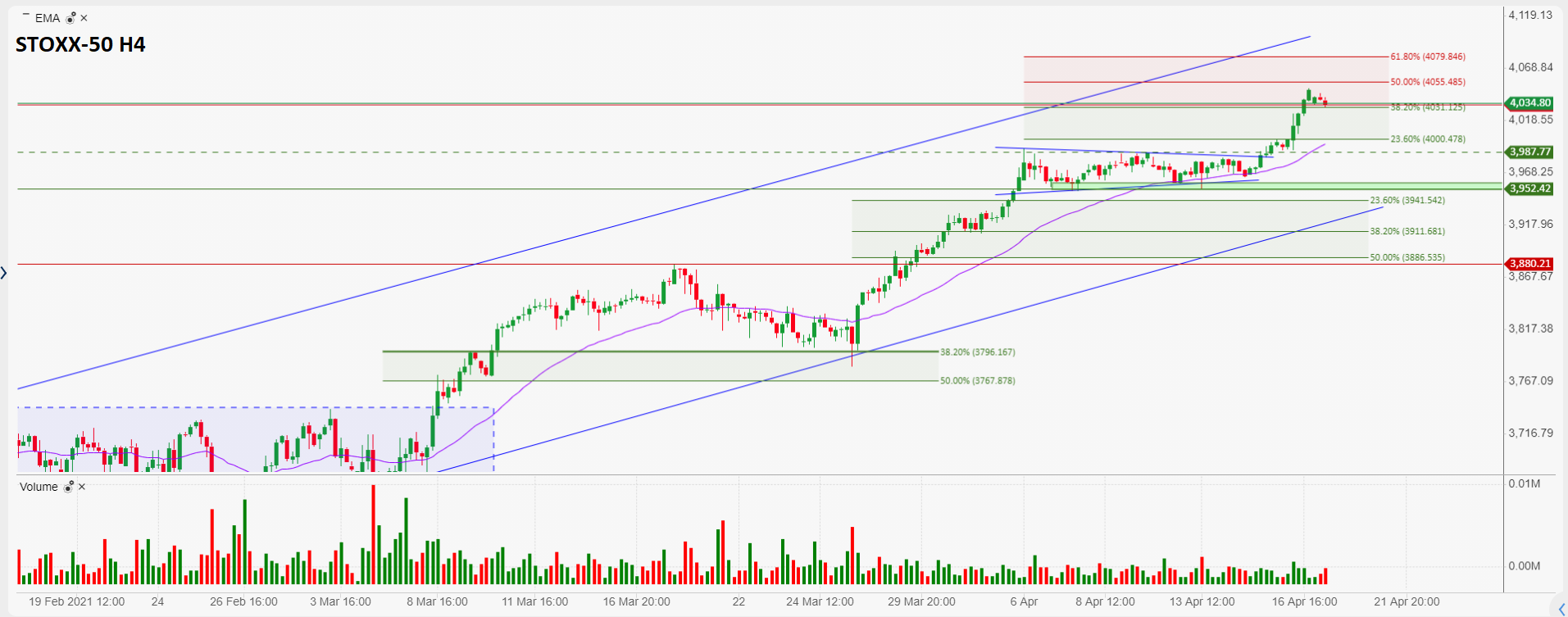

The Stoxx-50 index is still trading well above 4,000.0pts, challenging the 4,030.0pts level. Any bounce above that zone could drive prices further up towards 4,055.0pts and 4,080.0pts by extension.

Pierre Veyret– Technical analyst, ActivTrades

Disclaimer: opinions are personal to the authors and do not reflect the opinions of LeapRate. This is not a trading advice.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.