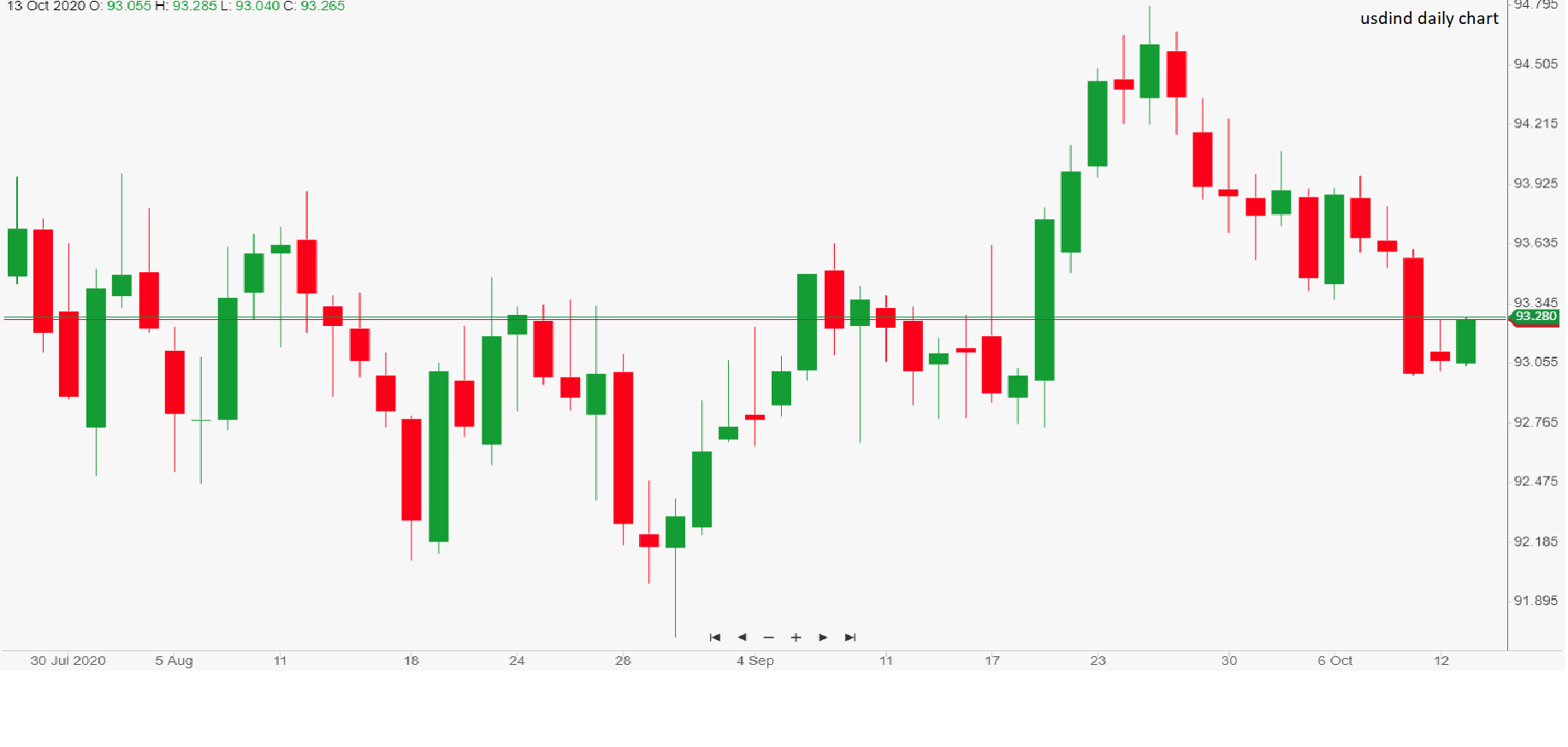

Risk aversion is the prevailing sentiment for financial markets early on Tuesday, with the main stock indices in Asia and Europe in the red and US futures pointing in the same direction. It is therefore hardly surprising that the dollar has recovered some of the ground lost over the last few days, after hitting a 3-week low versus other major currencies on Monday. The greenback’s gains versus risk-related currencies result from a setback in the development of a Covid vaccine by Johnson & Johnson, the continued stand-off between bipartisan lawmakers in Washington preventing the approval of an economic stimulus package plus a new addition to the party in the shape of a fresh dose of Chinese assertiveness banning the import of several key commodities from Australia. The latter factor reminds us that the latent trade and tech conflict between the Asian giant and Western economies continues to cast a shadow over global economic growth perspectives.

The countdown to the US election is drawing into sharper focus and as the odds of a Biden victory increase (implied probability went up from 65 to 69.2% over the weekend), investors are betting on the likeliest scenarios for oil in the next few years. A Biden victory could see less support for the shale oil industry, pulling up the oil price as a result. Vice versa, if Trump manages to defeat forecasts, shale oil would probably benefit from the tycoon’s help. Despite this, Trump could be supportive for the barrel through any potential new stimulus, which could boost (or drug?) the economy further.

From a technical point of view, WTI remains just below $40, after the price slipped yesterday. Investors are waiting for oil industry reports due out today to provide new directionality to the price.

Carlo Alberto De Casa – Chief analyst, ActivTrades

EUROPEAN SHARES

Shares drifted lower at the beginning of the European trading session on Tuesday as market sentiment remains weighed down by increasing uncertainty, despite encouraging Chinese data overnight. Investors’ risk appetite is on hold today following delays and difficulties in the development of a vaccine from Johnson & Johnson, while infection numbers keep on increasing everywhere. In addition, stock traders are becoming ever more disappointed by the failure of the US administration to deliver a new deal on further stimulus measures and must deal with the uncertainty of the upcoming presidential election. Having said that, and after yesterday’s rally on techs, many investors may choose to temper their exposure to stay on the “safe side” ahead of the earning season and its usual higher market volatility. With this in mind, investors’ attention will be focused on the financial sector with Citigroup, JPM and Blackrock all publishing their results today. There is unlikely to be any significant sell-off today as tech stocks are likely to offset any losses in the travel and leisure sector triggered by vaccine delays.

Pierre Veyret– Technical analyst, ActivTrades

Disclaimer: opinions are personal to the authors and do not reflect the opinions of LeapRate. This is not a trading advice.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.