This article was submitted by Michael Stark, market analyst at Exness.

‘Risk on’ has generally weakened so far this week with European shares mostly posting losses and crude oil moving down after OPEC+’s latest deal to increase production. The spread of the Delta variant of covid-19 amid relatively low rates of vaccination in various countries has generated some nervousness in markets around the world. The main focus this week is on the statement and press conference of the European Central Bank, but eyes are also on emerging markets on Thursday and Friday. This preview of weekly data looks at the releases likely to affect EURZAR and USDRUB.

There was no very significant news in monetary policy last week, with the central banks of Japan, Turkey, New Zealand and Canada all leaving rates on hold as expected. The Reserve Bank of New Zealand announced the end of its bond-buying programme; Turkey and Japan’s central banks were also somewhat positive on the outlook for the rest of the year while the Bank of Canada was overall neutral.

This week’s key event is the ECB’s statement on Thursday just before noon GMT. The Executive Board is likely to remain noncommittal and stress its tolerance of inflation temporarily above 2%, but hints on how its members view the eurozone’s economy into Q4 are likely to be key. The South African Reserve Bank and the Central Bank of the Russian Federation are also due to meet this week.

There is no globally important regular data due this week. The key regional release though is South African inflation on Wednesday. There’s also an unusual number of key data due from Russia. This week then is likely to be highly active for the rand and ruble given these high impact releases and the meetings of the SARB and CBRF on Thursday and Friday respectively.

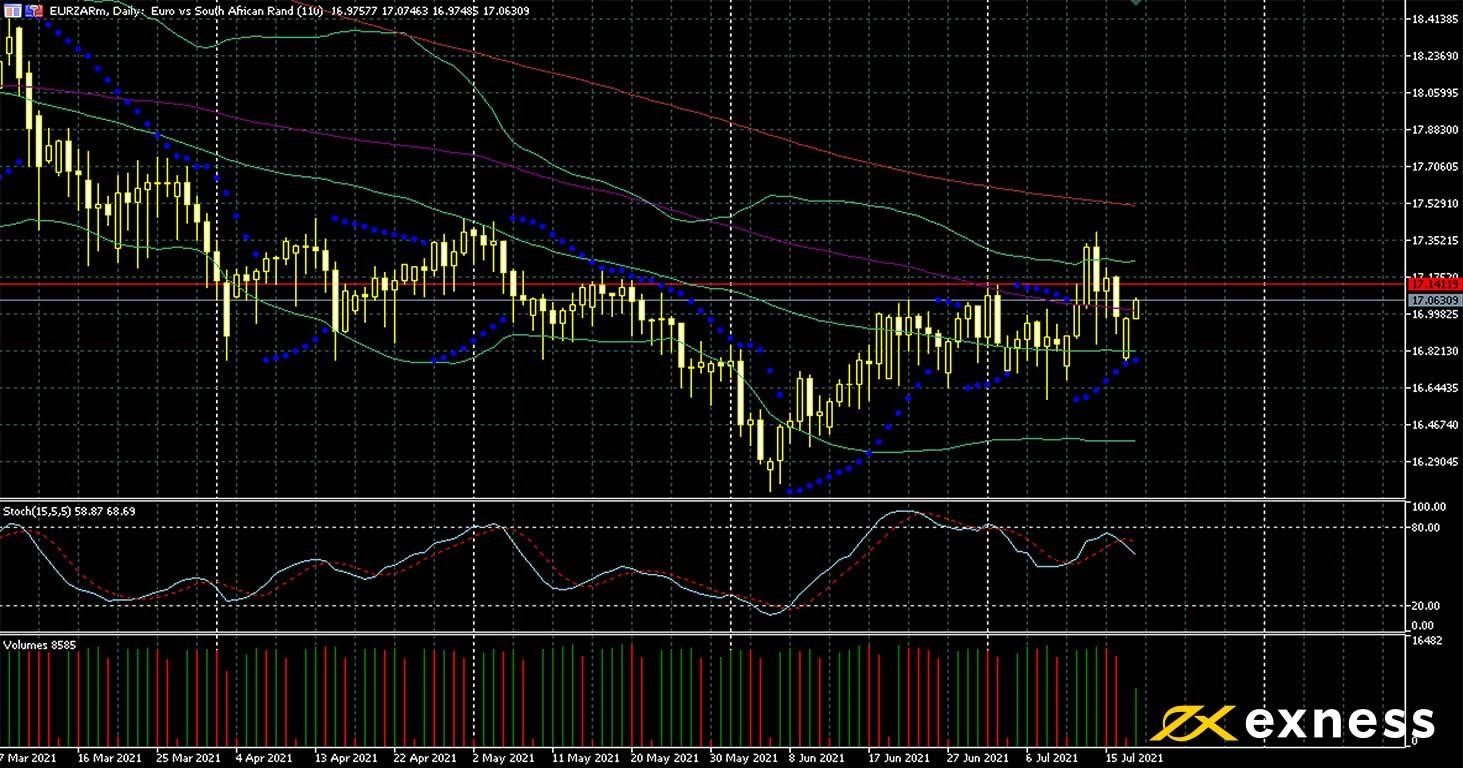

Euro-rand, daily

Considering the scope of recent civil disorder in parts of South Africa and its likely effect on economic recovery – not to mention creating ideal conditions for newer, more infectious variants of covid-19 to spread – the rand’s losses have been limited over the last few weeks. South Africa’s level 4 lockdown will continue until 25 July.

Sentiment on the euro though is weak: strong data around the end of 2020 and beginning of 2021 have generally been replaced by more lacklustre figures from major economies, and the Delta variant is likely to dent many countries’ plans to ease remaining anti-covid measures.

Tuesday’s close at R17.33 was a two-month high for EURZAR, but since then buying demand has been less strong. The 100 SMA is likely to continue as an important technical reference unless there’s a significant surprise from this week’s data and meetings of central banks.

A higher low (7 July’s R16.84) and higher high might traditionally be taken as evidence that the main downtrend has ended, but this symbol’s usually very high volatility and the strong reaction to the latter extreme might make sideways movement more favourable over the next few weeks. Again, though, data and the South African government’s reaction to internal disturbances could alter the technical picture significantly.

Key data this week

Bold indicates the most important releases for this symbol.

Tuesday 20 July

00 GMT: German annual PPI (June) – consensus 8.4%, previous 7.2%

00 GMT: German monthly PPI (June) – consensus 1.1%, previous 1.5%

00 GMT: South African leading business cycle indicator (May) – consensus 3.4%, previous 3.7%

from 11.45 GMT: statement and press conference of the European Central Bank

from 13.00 GMT: statement and press conference of the South African Reserve Bank

Dollar-ruble, daily

The dollar’s gains against the ruble since last week have been mirrored very closely by the ruble’s losses, with the direct correlation between crude and Russia’s currency remaining strong so far this year on the whole. As elsewhere, sharply rising cases of covid-19 in Russia have hit sentiment on the ruble. Conversely, expectations remain high that the CBRF will hike its key rate again by another half a percent. If accurate, this projection would take Russia’s base rate to a full 6%.

TA also seems to support the somewhat negative picture for the ruble. USDRUB is no longer overbought from either Bollinger Bands or the slow stochastic but it remains above the 100 and 50 SMAs. The main resistance in view is still the 200 SMA slightly above the price, while further ahead previous intraday highs around ₽75.20 and ₽75.70 could cap any ongoing gains at least temporarily.

Whatever markets’ longer term reaction to the releases, short-term opportunities are likely to be many this week for dollar-ruble given the number of important Russian data, particularly on Tuesday afternoon. The regular stock data and rig count from the USA are also in focus for traders of the ruble.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.