This article was submitted by Michael Stark, market analyst at Exness.

Many shares and ‘risk-on’ instruments have recovered so far this week as markets seem to perceive positively the ongoing talks between Russia and Ukraine for a possible ceasefire. Most commodities meanwhile have declined sharply for similar reasons plus very large numbers of new cases of Covid-19 in key regions of China. This midweek preview of data looks at gold-dollar (XAUUSD) and Brent Crude (UKOIL) ahead of the Fed’s crucial meeting tonight.

The last major central bank to raise its base rate was the Bank of Canada on 2 March. Signals from the ECB last week were mostly noncommittal, since many central banks are now in a quandary with surging inflationary pressure from the war in Ukraine combined with a high degree of economic uncertainty.

Tonight’s meeting of the Federal Open Market Committee is almost certain to result in a hike of the funds rate, but the small chance of a two-step hike to 0.5-0.75% is still there. Also widely expected to hike is the Bank of England, which would be the first three-in-a-row tightening in 25 years. The Central Bank of the Russian Federation is due to meet on Friday morning, but with the ruble suspended for trading as a CFD this is unlikely to have any significant effect on other markets.

The main regular data still to come this week include Australian employment, New Zealand GDP and Japanese inflation. The main new narrative other than the war, inflation and monetary policy is the new wave of Covid in China: with all of Jilin Province and the city of Shenzhen now under lockdown, sentiment on oil and other industrial commodities could take another hit.

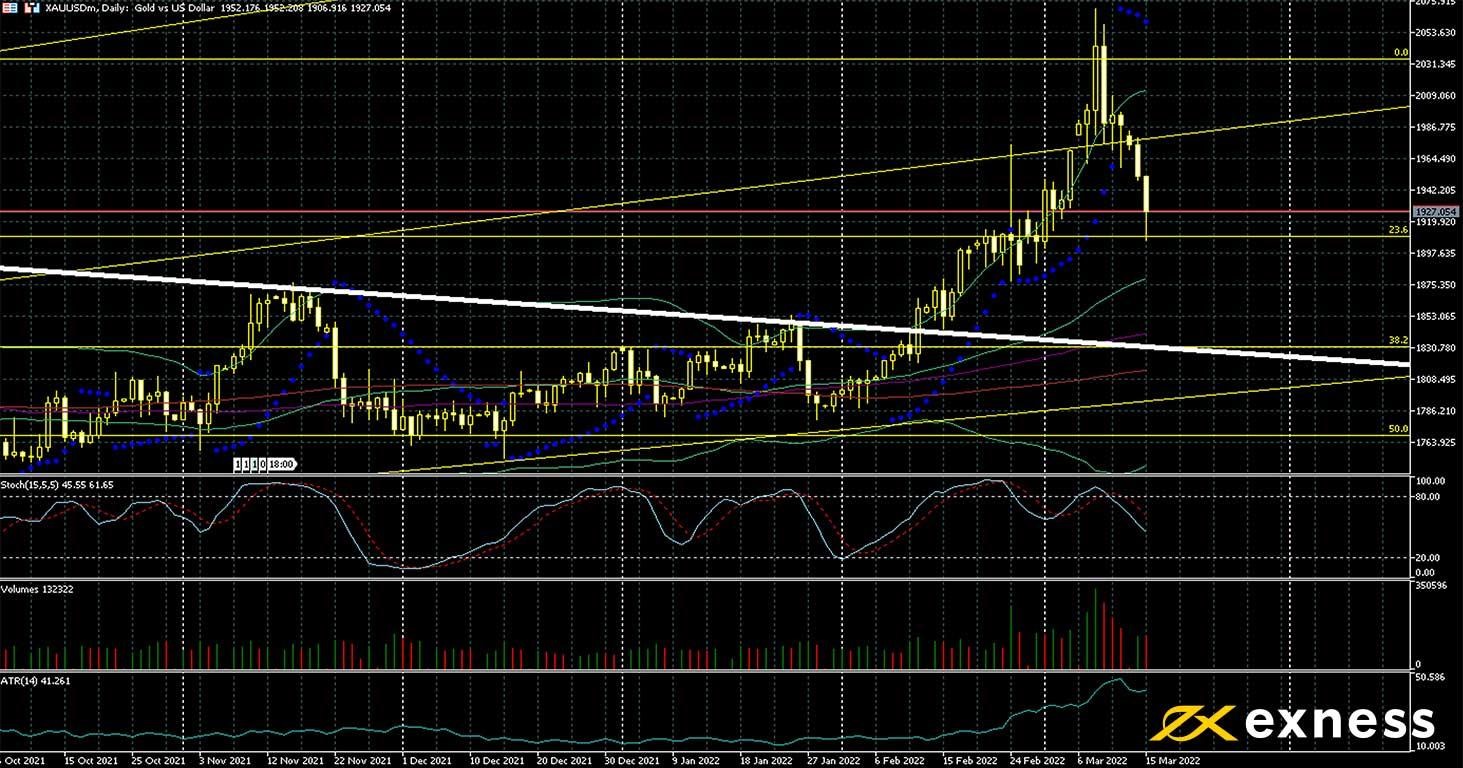

Gold-dollar, daily

Gold hit its lowest in a week late on Tuesday afternoon GMT as participants started to expect a quicker resolution to this phase of the Russo-Ukrainian War, yields from American Treasury bonds rose and the Fed seems certain to hike at least 0.25% this evening. 40-year highs in inflation in the USA and other major economies remain a key narrative supporting gold.

A return to strength looks unlikely as of now based on TA. Although yesterday’s test of the 23.6% weekly Fibonacci retracement area has been rejected for now, selling volume has been high since last week and the downward reaction on 9 March from the area of the all-time high has been very strong. With ATR now around $40, a move at least temporarily below $1,900 seems to be very likely today, although the reaction to the press conference would determine whether this might continue. To the upside, $2,000 is an obvious psychological resistance around the 50% zone of the monthly Fibonacci fan.

14.00 GMT: American existing home sales (February) – consensus 6,100,000, previous 6,500,000

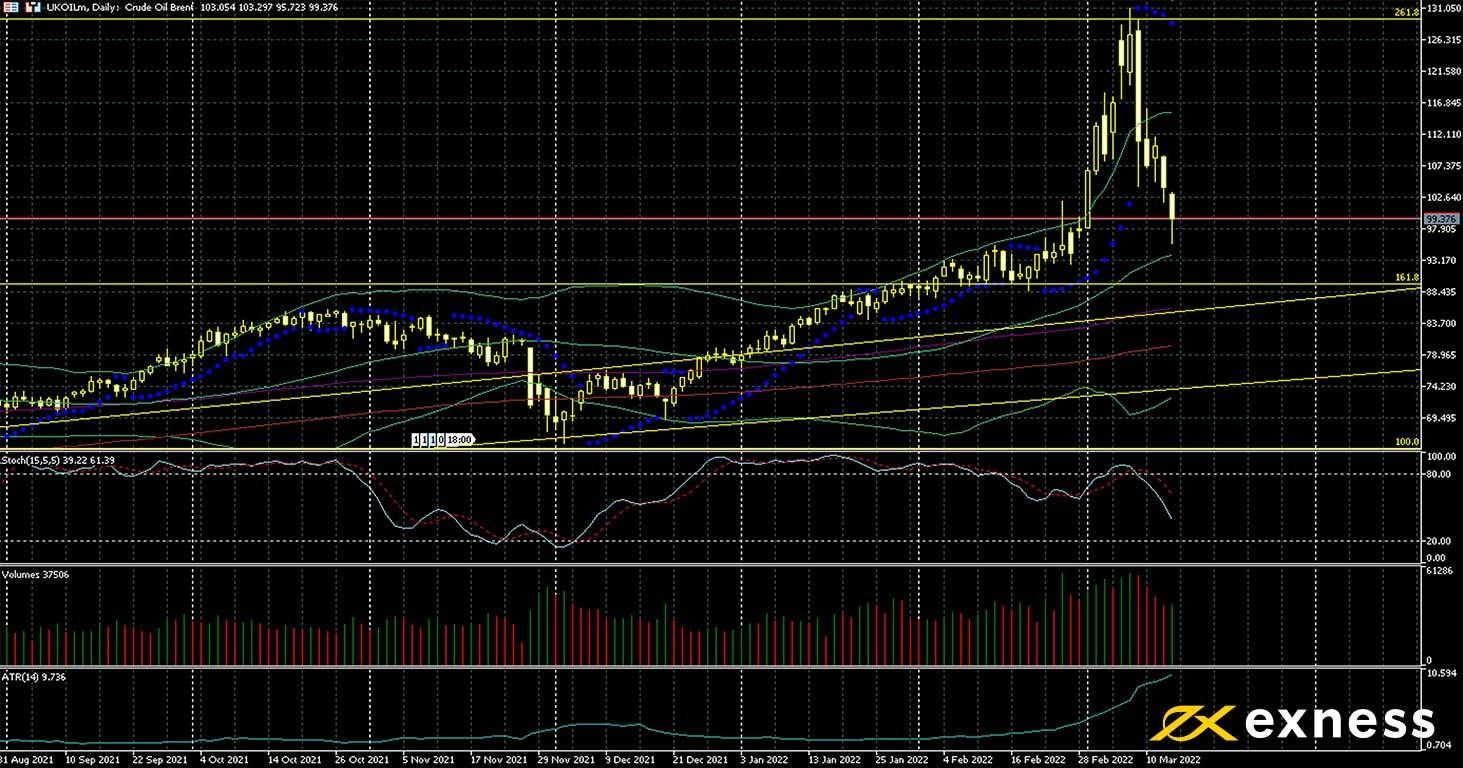

Brent, daily

Brent moved clearly below $100 a barrel yesterday as it became increasingly clear that Europe will not immediately and generally cut imports of Russia oil and as tens of millions of people in key industrial areas of China went into new anti-Covid lockdowns. While supply remains fairly tight for now as Saudi Arabia and the UAE have not started to pump more, due primarily to political disagreements with the current government of the USA, production in America has continued to increase this year, with 500 active oil rigs reached last month.

The technical picture for oil is quite similar to that for gold, but here we can observe no great surge in volume last week. Brent also doesn’t seem to have a key support between the psychological area of $100 and the 161.8% weekly Fibonacci extension area slightly below $90.

Behaviour around the 50 SMA from Bands this evening is likely to be important for direction into the end of the week. Usually, oil suffers as rates rise because this suggests less strong economic growth. However, in the current environment of extremely high inflation and high volatility, a change in sentiment on ceasefire talks could shift the picture from the chart dramatically.

Key data this week

Bold indicates the most important releases for this symbol.

Experienced writer and journalist, working in the global online trading sector, Steffy is the Editor of LeapRate. She has previous experience as a copywriter and has been with the company since January 2020. Steffy has a British and American Studies degree from St. Kliment Ochridski University in Sofia.