This following article was submitted by Michael Stark, market analyst at Exness.

Markets around the world seem to be set for another week of panic over the spreading coronavirus. Indices continued to lose value last week despite more emergency measures from a number of central banks; the dollar has made huge gains against most currencies.

Most major central banks cut their rates again last week. The Reserve Bank of Australia cut by another 0.25% and the Bank of England by 0.15%, taking their rates to their lowest levels ever. The Bank of Canada, the Norges Bank and Banxico each cut by 0.5%, and others like the Reserve Bank of New Zealand made even larger cuts.

The number of confirmed cases of covid-19 is now nearly 300,000 with over 12,000 deaths according to the WHO. While China seems to be on the road to recovery with factories reopening, many European countries are under strict lockdown. Data over the next few weeks will probably start to reflect significantly reduced economic activity in most countries.

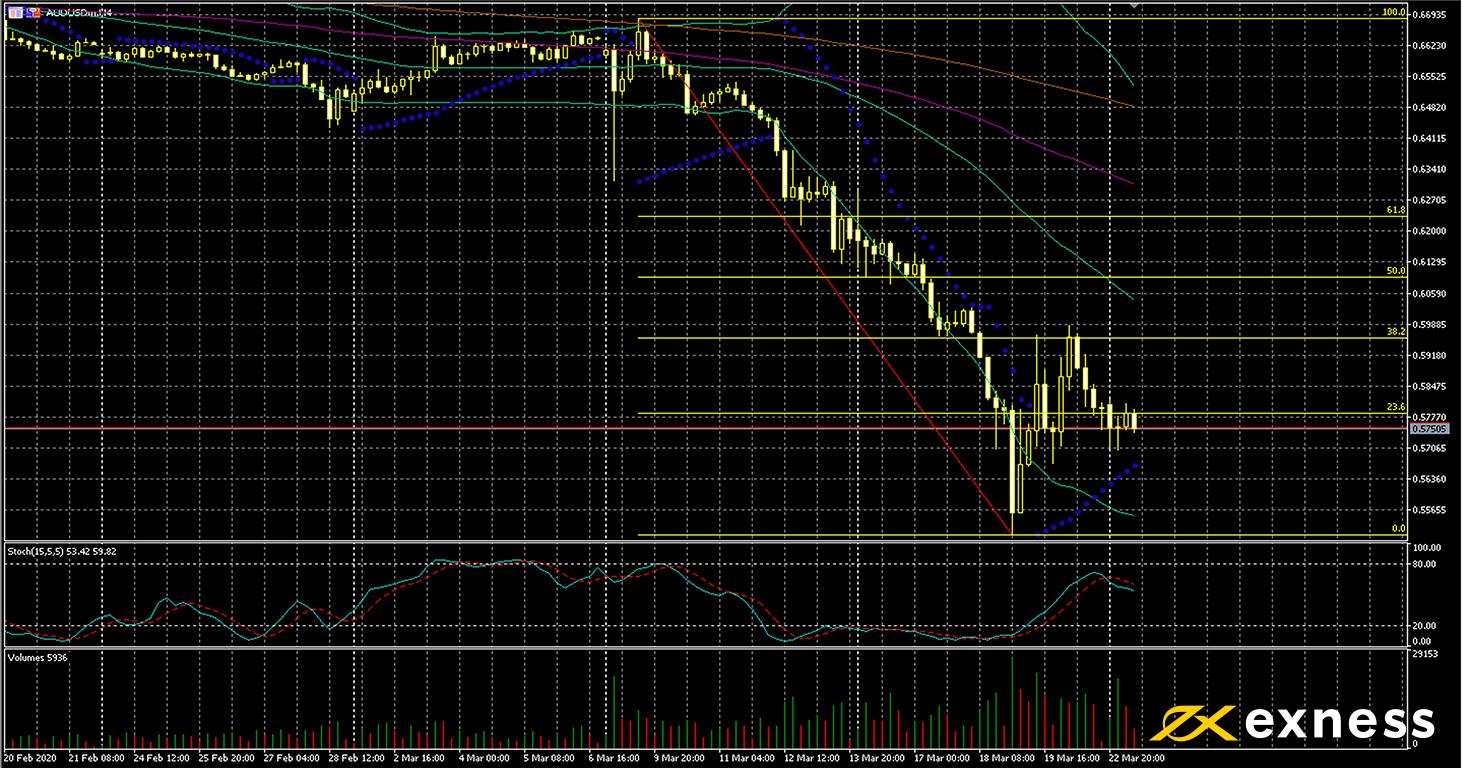

Australian dollar-US dollar, four-hour

The Aussie dollar retraced upward somewhat towards the end of last week. On Friday AUS200 suffered some of its biggest daily losses since the start of the current crisis, losing about 6%. AUD is usually seen as one of the more risk-on instruments among major currencies, so it has generally lost strength in March in most of its pairs.

Fibonacci retracement here is based on the ongoing downward movement which paused in the second half of last week. The 38.2% appears to be an important area, with price failing twice to break above it on Thursday and Friday. There is no longer any indication of oversold on this timeframe from either Bollinger Bands or the slow stochastic. A retest of the recent low around the psychological zone of 0.55 seems to be possible this week depending on markets’ reactions to the news. There’s no important data from Australia this week but American data, especially initial jobless claims on Thursday, could be key for this symbol.

Friday 27 March, 12.30 GMT: American personal income (February) – consensus 0.4%, previous 0.6%

Friday 27 March, 12.30 GMT: American personal spending (February) – consensus 0.2%, previous 0.2%

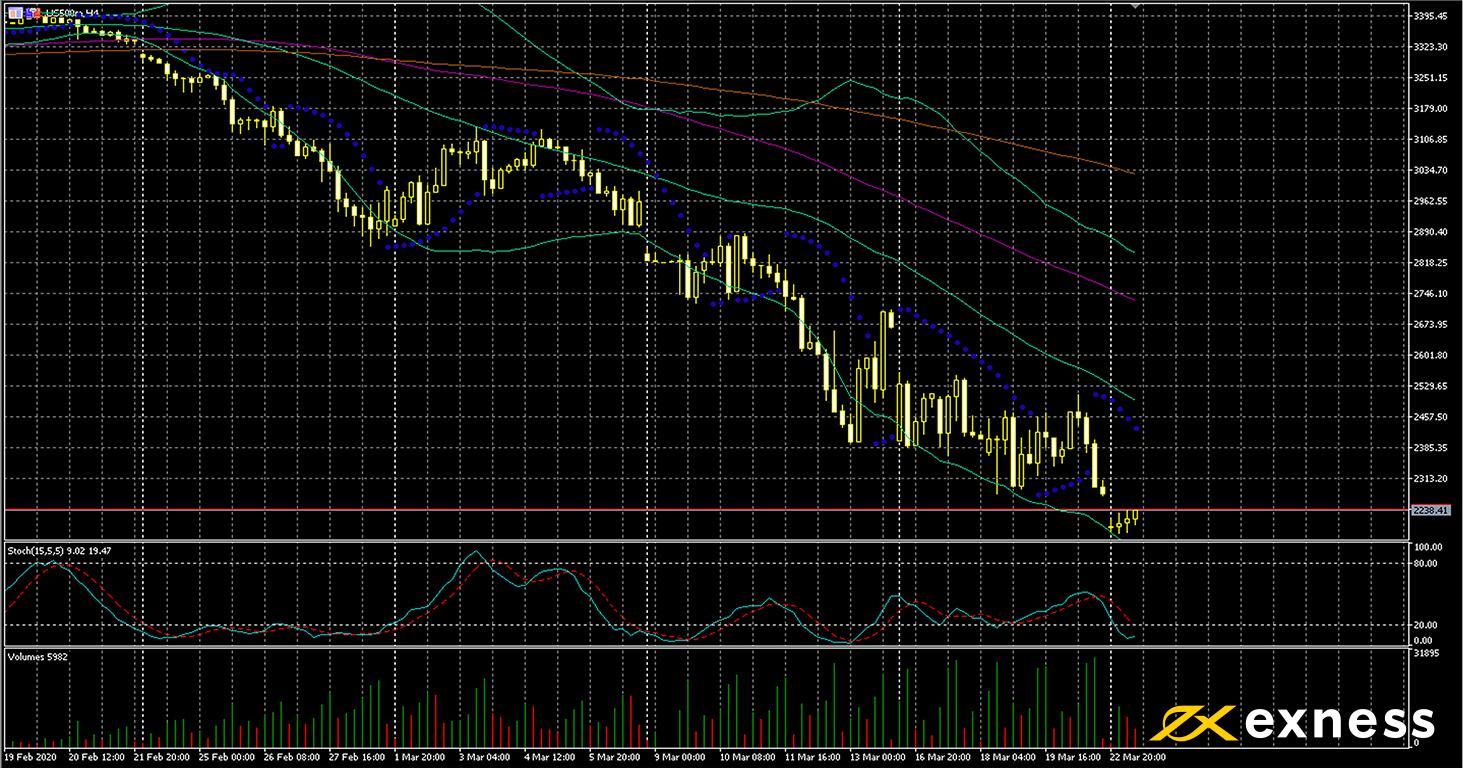

US500, four-hour

US500 like most indices has made ongoing losses since markets started to panic over the spread of the coronavirus. Aviation has been one of the hardest hit sectors but expected lower demand has led to losses for the large majority of shares in the index.

One can observe from volumes here that a number of traders have been trying to ‘catch the knife’, which is never recommended in these circumstances. After price emerges from oversold, there’s still considerable scope for more losses this week. The focus is likely to be on initial jobless claims on Thursday afternoon GMT for an indication as to how weak demand might be in the coming weeks. The deadlock in the Senate over the American government’s relief package is also an item to be monitored by traders.

Key data points

Bold indicates the most important releases for this symbol.

Friday 27 March, 12.30 GMT: American personal income (February) – consensus 0.4%, previous 0.6%

Friday 27 March, 12.30 GMT: American personal spending (February) – consensus 0.2%, previous 0.2%

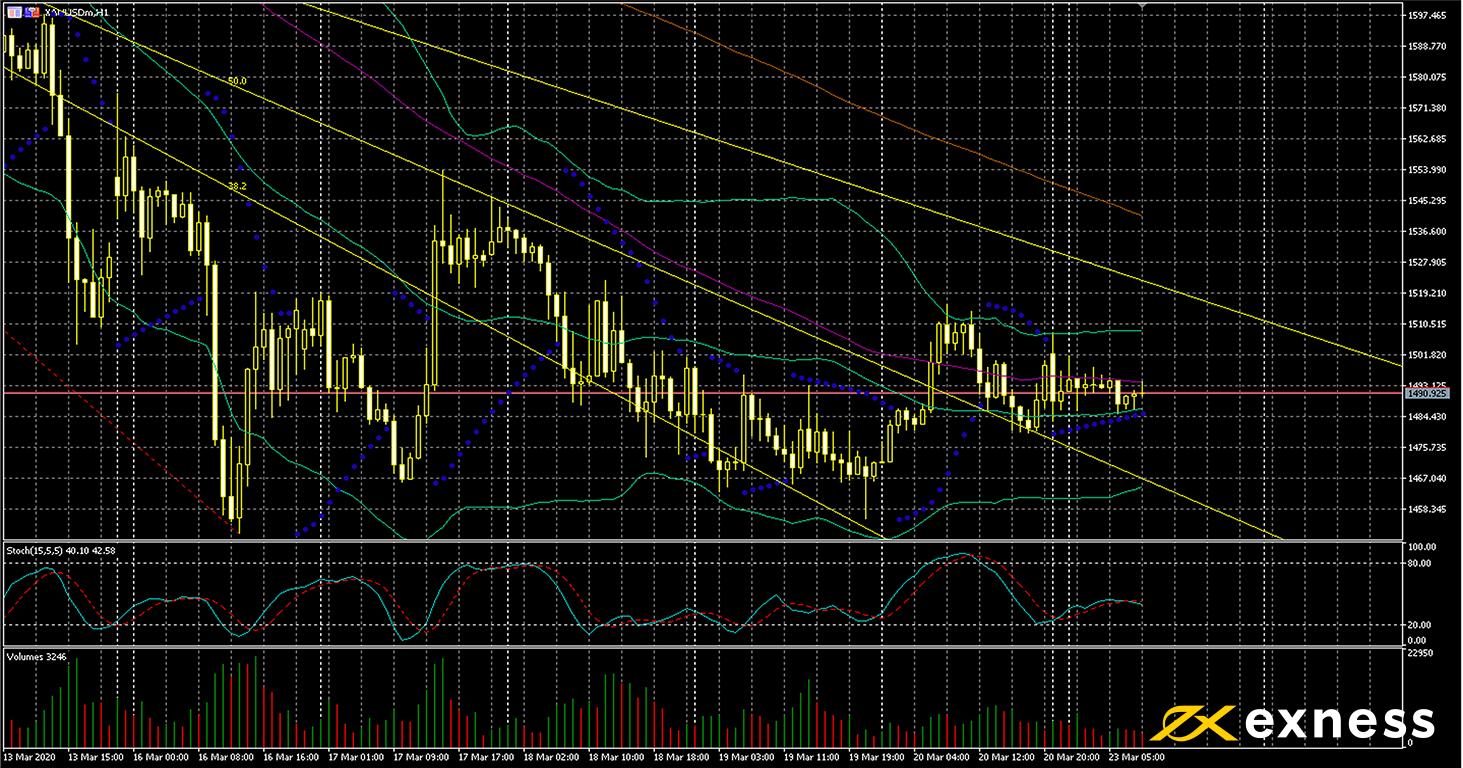

Gold-dollar, hourly

Gold’s losses against the dollar seem to have halted for now, with price lacking any clear direction since the start of last week. By comparison with 2008, it’s possible that gold could resume its gains as the crisis potentially deepens in various markets. On the other hand, the news from stock markets and governments could lead to significant ongoing volatility.

The Fibonacci fan here is based on the string of losses 6-13 March. Now that price has passed above the 38.2% and 50% zones, one might expect to see some more gains if the rate can hold above the 61.8% as well. As above, though, data and news could alter the technical picture completely; gold can be very unstable in such times of economic crisis.

Key data points

All week: British parliamentary debate of the coronavirus bill

Thursday 26 March, 12.30 GMT: American quarterly GDP growth (final, Q4) – consensus 2.1%, previous 2.1%

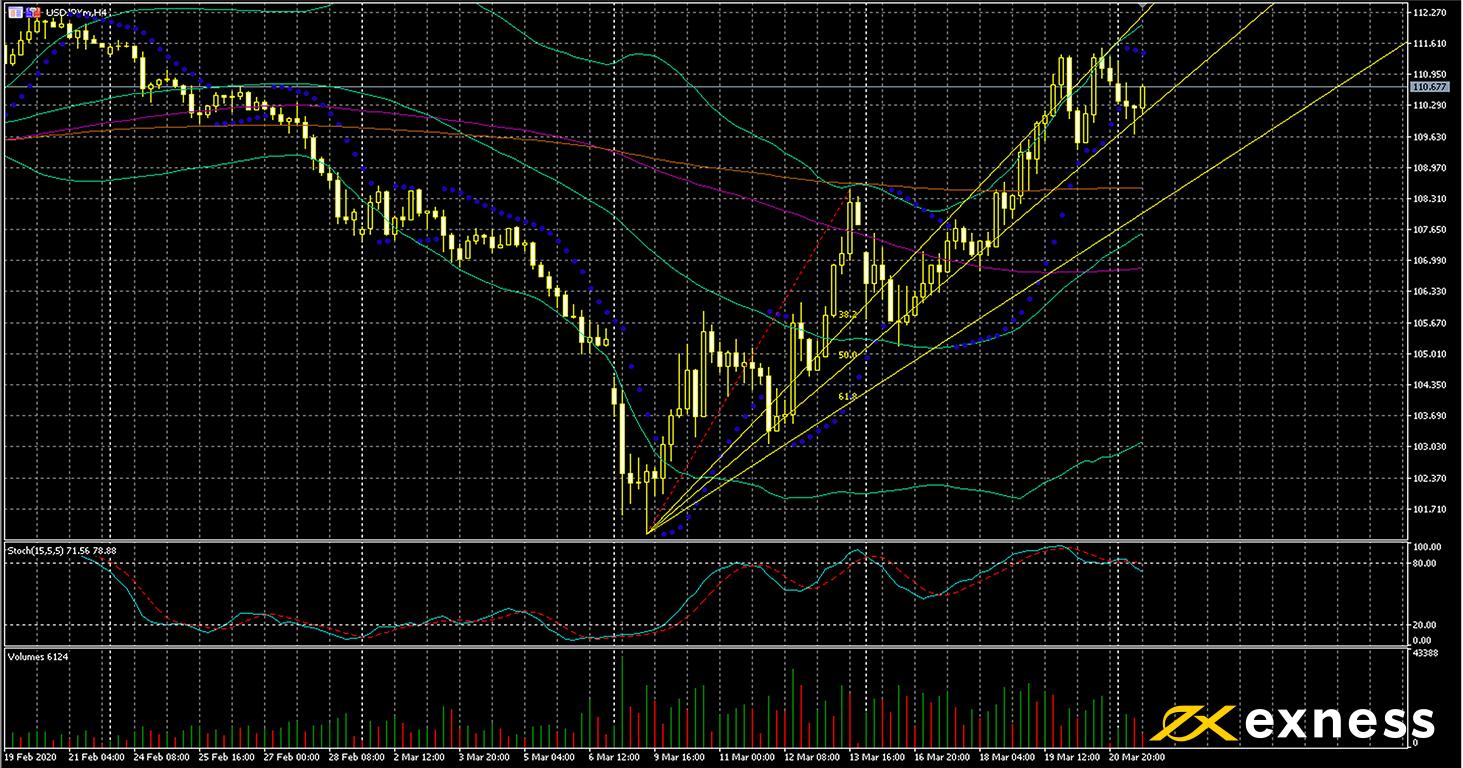

Dollar-yen, four-hour

USD-JPY is another haven, but unlike gold has continued to post gains over the last fortnight as the flight to cash remains more important to most investors than the flight to safety. JP225 bounced somewhat on Friday morning, and the yen’s inverse correlation with the index appears to be holding for now.

The key area to the downside is the 50% zone from the Fibonacci fan. A close below this on the four-hour chart might be an early signal of an extended period of consolidation. To the upside, the psychological area of 112 is expected to be important. This was also the approximate extent of the dollar’s gains in the fourth quarter of 2019.

Key data points

Tuesday 24 March, 23.50 GMT: minutes of the Bank of Japan’s meeting